Ireland's emerging macroprudential framework: two cases, one template

Two CBI deployments in three years — property funds and Sterling LDI — and what they say about the Eurosystem's reciprocation proposal. Part 2 of 2.

Part 1 used twelve years of Bundesbank data to argue that Germany’s KAGB redemption-restriction regime materially compressed retail open-ended property fund flow stress, including through the 2022–24 European rate shock. The German evidence is empirical: did the template work? The Irish material here is institutional: how is the template being deployed in Europe right now, by whom, with what coordination, and against which gaps in the architecture?

The Eurosystem’s May 2026 report Strengthening the macroprudential lens in the regulation of non-bank financial intermediation proposes, among other things, a reciprocation framework for cross-border NBFI macroprudential measures. The institution that has built such a framework in practice is the Central Bank of Ireland. Discussion Paper 11, published 18 July 2023, sets out CBI’s conceptual foundation. Two policy deployments since then give two worked examples: leverage and liquidity measures for Irish-resident property funds in November 2022 (under Regulations 26 and 18 of the Irish AIFM Regulations), and a codified yield-buffer framework for Sterling LDI funds in April 2024 (under Article 25 AIFMD, in coordination with CSSF and aligned with TPR/FCA guidance for the UK leg).

CBI’s own press release on the LDI codification states explicitly that this was “the second time the Central Bank of Ireland has introduced policy measures under the non-bank pillar of its macroprudential policy framework” — the first being the property fund measures. That self-framing is useful: CBI is presenting both deployments as components of the same emerging architecture rather than as unrelated regulatory actions. This article takes that framing at face value and works through what each deployment looks like, what early data show, and what the two cases together say about the Eurosystem report’s reciprocation proposal.

The CBI framework architecture

DP11 articulates the conceptual case for a macroprudential perspective in fund-sector regulation that complements rather than replaces the existing investor-protection mandate. The paper is explicit on a point that matters for what follows: macroprudential policy for investment funds “will be most effective if regulators coordinate. This underpins the importance of developing a globally-consistent approach. In certain circumstances, domestic action may also be required.”

The two deployments illustrate both halves of that statement. Property funds were a domestic action: Irish-authorised funds and managers, an Irish commercial real estate exposure that posed Irish systemic risk. Sterling LDI was the coordinated case: vehicles domiciled across Ireland and Luxembourg, sterling-denominated exposures to UK pension liabilities, a crisis whose epicentre was the UK gilt market. The two cases bookend the operating range of the macroprudential framework CBI is building. What unites them is not identical legal machinery but the use of fund regulation for explicit financial-stability rather than investor-protection purposes — Regulations 26 and 18 in one case, Article 25 AIFMD in the other.

Property funds: the slow-moving case, three years in

CBI announced the property fund measures on 24 November 2022 with two components. First, a 60% total-debt-to-total-assets leverage limit, imposed by way of condition of authorisation under Regulation 26 of the Irish AIFM Regulations. Existing funds have a five-year implementation period running to 24 November 2027, during which CBI expects gradual and orderly progress toward lower leverage. New funds must comply from inception. Funds investing at least 80% of AuM in social housing are out of scope, subject to specific lease and debt-structure conditions.

Second, guidance on the application of Regulation 18 of the Irish AIFM Regulations setting an expected minimum liquidity timeframe of 12 months for property funds, given the nature of the underlying assets. Existing funds had an 18-month implementation period (the guidance applied from 24 July 2023); new funds authorised on or after 24 November 2022 must comply from inception.

These are textbook ex-ante macroprudential tools — a numerical leverage cap and a liability-side liquidity timeframe — applied to a cohort holding illiquid commercial real estate. The conceptual architecture is similar to KAGB but the policy instruments are different: KAGB used redemption restrictions on the liability side; CBI used leverage restrictions on the asset side combined with redemption-frequency guidance.

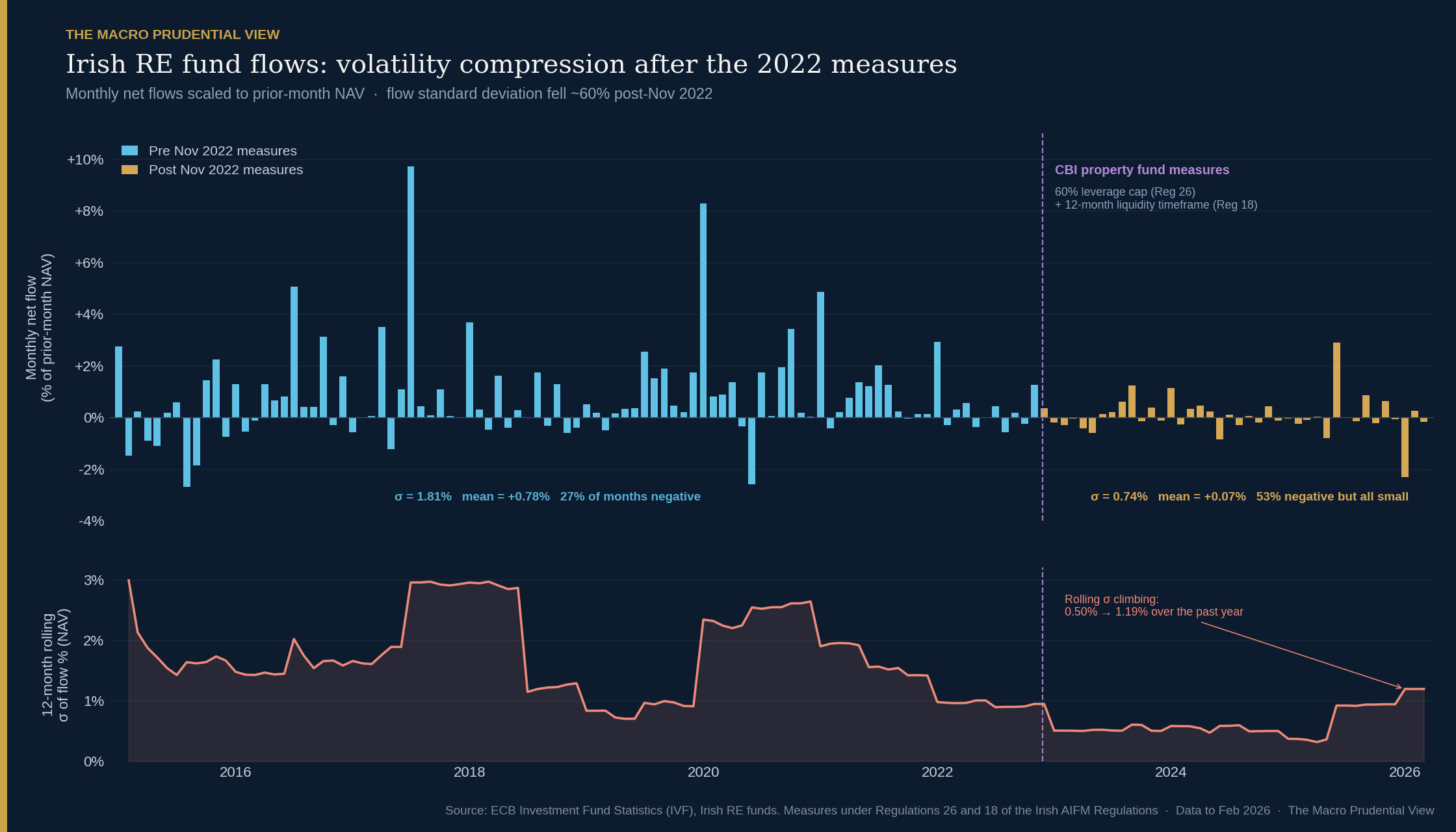

The chart above shows monthly net flows as % of lagged NAV for the Irish RE fund cohort from December 2014 to February 2026. Pre-Nov 2022 (95 monthly observations): mean +0.78%, σ 1.81%, 27% of months in net outflow. Post-Nov 2022 (40 monthly observations): mean +0.07%, σ 0.74%, 53% of months in net outflow. Flow volatility roughly halved; the upper tail of inflow surges has been eliminated.

The headline pattern is similar to the KAGB-era German case: post-implementation flow volatility compresses materially, and the tail risk on the inflow side is eliminated. The Irish post-2022 sample is shorter, the macro environment was specifically a CRE valuation correction rather than a broader retail-fund stress, and the dataset captures all Irish RE funds in the ECB Investment Fund Statistics rather than only the macroprudential cohort (≥50% Irish CRE), which CBI’s FSR 2025:II flags in footnote 64. With those caveats: the direction of travel is consistent with what the policy was designed to achieve.

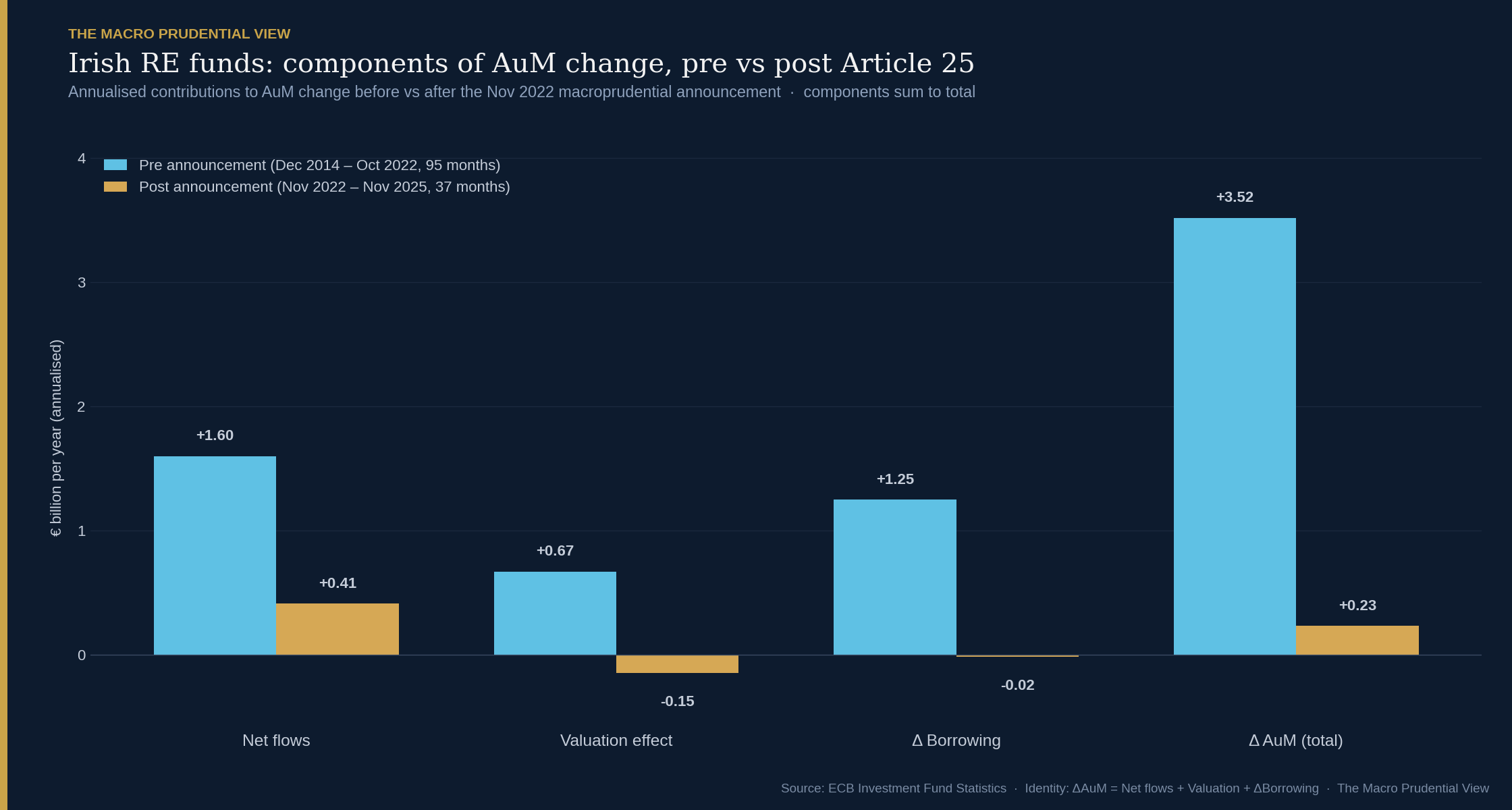

The chart above decomposes the change in fund AuM into three components — net flows, valuation effects, and changes in borrowing — annualised across the pre and post periods. Pre-Nov 2022 the Irish RE fund sector grew by roughly €3.5bn per year, with flows (+€1.6bn), valuation (+€0.7bn), and borrowing (+€1.3bn) all contributing positively. Post-Nov 2022 the sector grew by €0.23bn per year, with modest inflows (+€0.41bn) offsetting CRE valuation drag (-€0.15bn) and effectively zero change in borrowing (-€0.02bn).

The post-implementation trajectory is neither the run-and-fire-sale dynamic the policy was designed to prevent, nor a continuation of pre-implementation growth. The sector neither grew nor contracted materially in the post-implementation period — a quieter trajectory than pre-2022. This is itself the policy story: in previous CRE cycles, falling valuations would trigger run-like dynamics on retail-facing vehicles, forcing asset sales that depressed valuations further. The fact that the sector has gone quiet against a meaningful CRE correction is the circuit-breaker working as intended. The bank-to-non-bank debt substitution within the cohort is worth flagging: CBI’s FSR 2025:II reports that Irish property fund debt fell over 2024 from €15.91bn to €15.07bn, with bank and other debt down €1.75bn partially offset by an increase of €0.91bn in non-bank debt (Chart 39). That is itself a within-cohort substitution worth monitoring as the leverage transition proceeds toward its November 2027 deadline.

The watch-this-space caveat: the most recent observation in the flow data is a -2.31% Pub-style outflow in December 2025, and the 12-month rolling volatility has crept from 0.50% to 1.19% over the past year. The leverage transition has two more years to run, and the funds adjusting toward the cap may be doing so against a still-soft CRE valuation environment. None of this is a problem with the policy — it is the policy doing its work, gradually, against a difficult macro backdrop. But it is a reminder that the post-implementation period is not yet a steady state.

Sterling LDI: the fast-moving cross-border case

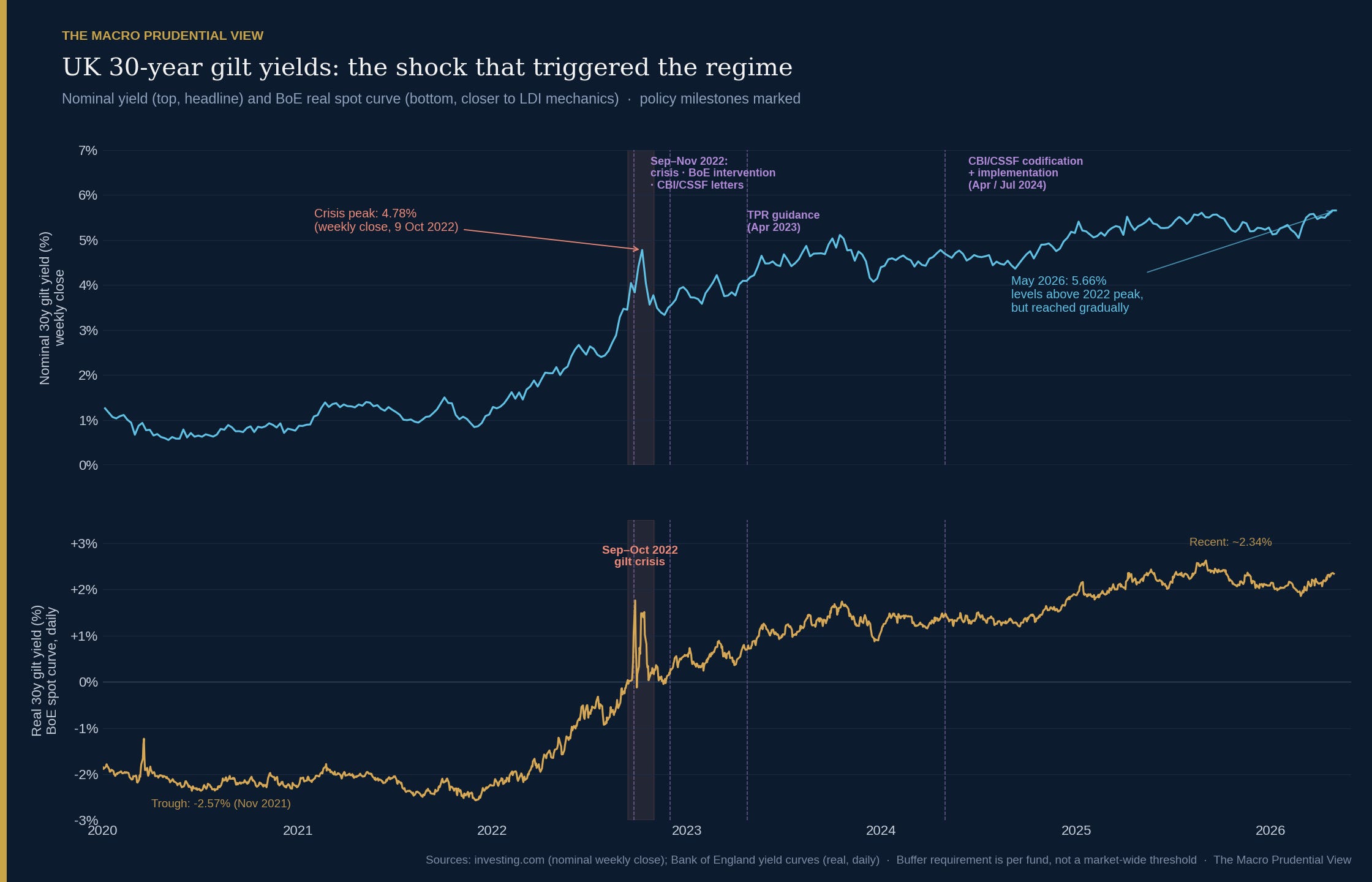

The chart above shows UK 30-year gilt yields from 2020 to 2026, with policy milestones marked. The crisis itself was concentrated: the Bank of England’s December 2022 Financial Stability Report describes what happened in late September 2022 as “a vicious spiral of collateral calls and forced gilt sales that risked leading to further market dysfunction, creating a material risk to UK financial stability”. Nominal 30y gilts moved from 3.45% on 11 September to a 4.78% weekly close on 9 October — about 130 basis points in four weeks. The BoE’s emergency bond-purchase programme stabilised the market within roughly two weeks. The structural question — what to do with the LDI cohort thereafter — was the regulatory community’s to answer.

The response unfolded in two stages. On 30 November 2022, CBI and CSSF issued substantively identical industry letters to managers of GBP LDI funds, framed explicitly as a coordinated CBI/CSSF/ESMA response. The letters noted that resilience buffers in the 300–400 basis-point yield-shock range had been built up across the cohort post-crisis, expected those levels to be maintained, and required advance notification and stress-tested justification before any reduction. This was supervisory expectation backed by a notification regime — not a codified rule with an explicit numerical floor.

Eighteen months later, on 29 April 2024, CBI and CSSF announced aligned codified frameworks. The CBI version requires Irish-authorised GBP LDI funds to maintain resilience to a minimum 300 bps increase in UK yields, with a three-month transition for existing funds and at-inception compliance for new ones. The CSSF version is parallel: 300 bps minimum, monthly average yield buffer reported each month-end, with limited flexibility (one of the last four monthly observations may be below 300 bps in exceptional circumstances). The November 2022 letters formally ceased to apply once the implementation period ended on 29 July 2024.

CBI Governor Gabriel Makhlouf framed the rationale in terms that the Eurosystem report would later use almost verbatim: “The gilt market disruption of 2022 demonstrated how financial vulnerabilities in non-bank financial intermediation can amplify adverse shocks to the rest of the financial system and the broader economy. The macroprudential measures announced today aim to safeguard resilience of sterling LDI funds, and — in doing so — support financial stability at a global level. Given the cross-border nature of capital markets, achieving that outcome requires effective international co-ordination.” The cross-border coordination was explicit in the announcement: CBI worked with CSSF, UK authorities, ESMA “and relevant stakeholders since the beginning of the UK gilt market crisis”; the CSSF announced its aligned framework on the same day. The UK leg ran in parallel: the BoE FPC recommended interim TPR action; TPR’s April 2023 trustee guidance set a 250 bps minimum stress buffer plus scheme-specific operational buffer (principles-based rather than a single numerical floor); the FCA published associated guidance for fund managers.

The two architectures — CBI/CSSF’s 300 bps numerical floor with monthly observation, and TPR’s 250 bps minimum stress buffer plus principles-based operational buffer — are functionally similar approaches to a shared resilience objective. CBI/CSSF chose a single numerical floor that is straightforward to monitor and enforce. TPR chose a principles-based architecture that requires trustee judgement about scheme-specific exposures. Each architecture offers different operational trade-offs; the next stress event will provide the empirical comparison that published evidence does not yet allow.

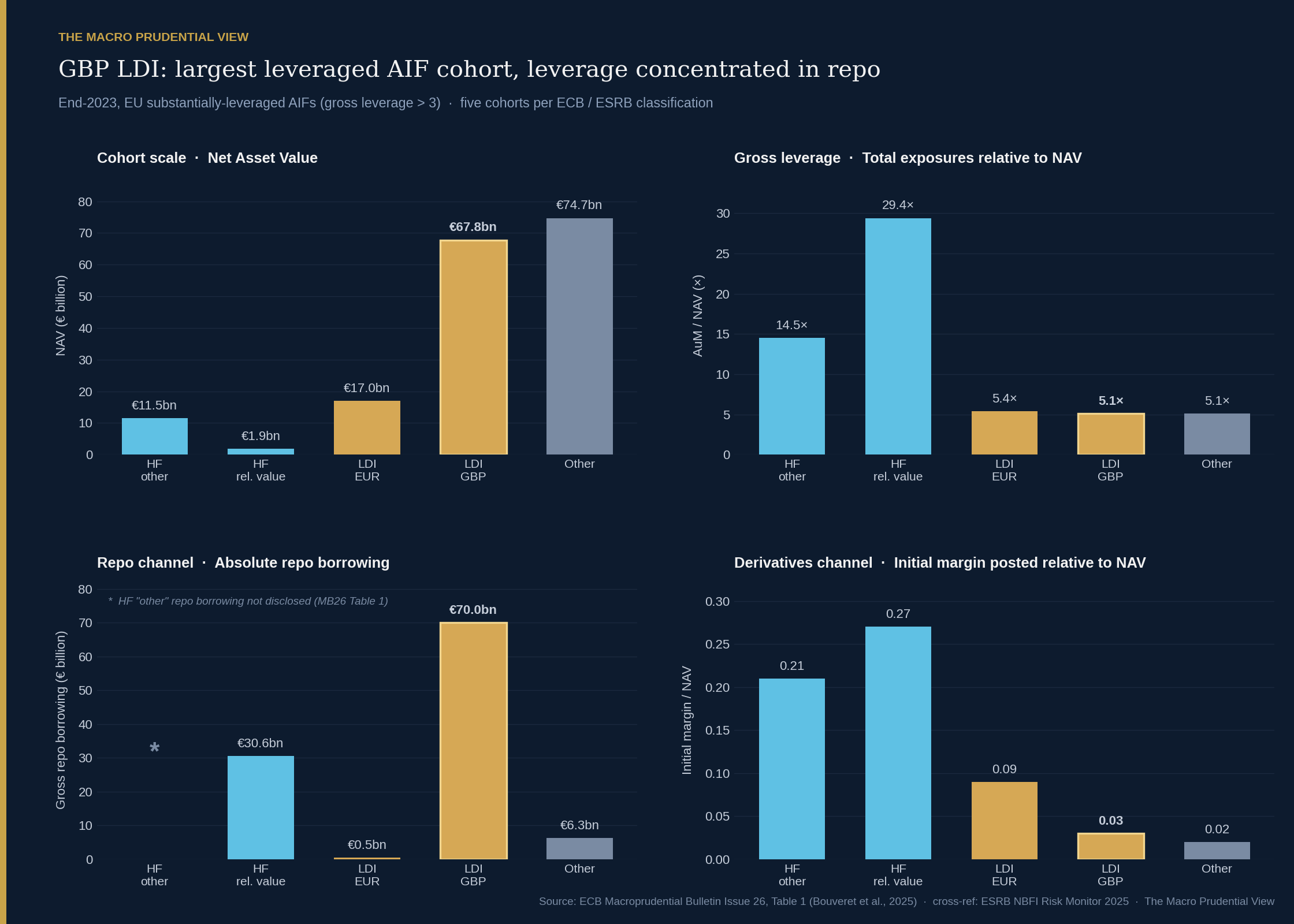

The chart above shows the structural reason GBP LDI funds got macroprudential attention first. From ECB Macroprudential Bulletin Issue 26, Table 1 (Bouveret, Ferrari, Grill, Molestina Vivar, Schmidt and Weistroffer, 2025; cross-referenced with ESRB NBFI Risk Monitor 2025, Table 3): GBP LDI is the largest cohort by NAV (€67.8bn) within the EU’s substantially-leveraged AIF universe, the largest by absolute repo borrowing (€70.0bn), and concentrates its leverage in repo rather than derivatives. Among substantially-leveraged AIFs at end-2023, GBP LDI alone accounts for €349bn of AuM — by far the dominant single cohort.

Bouveret et al. (2025) test this cohort against the exact 300 bps shock the codified buffer is designed to absorb. They find an average NAV loss of 31% for GBP LDI funds and 26% for EUR LDI funds — described as having “negligible” effect on hedge funds and other leveraged AIFs at this risk factor. Crucially, the article reports that “only very few LDI funds would have a NAV below zero” in this scenario: the calibrated buffer absorbs the calibrated stress. A milder 100 bps shock generates a €6.6bn aggregate liquidity shortfall across the LDI cohort, which Bouveret et al. note “would be covered by the redemption of money market fund shares and sales of unpledged bonds”. That is the cross-border doom loop in compressed form: a UK gilt shock forces Irish and Luxembourg LDI funds to redeem MMF shares (which are themselves a major source of short-term funding for euro-area banks via commercial paper and certificates of deposit, as documented in ESRB monitoring of euro-area MMFs) and to sell unpledged bonds into thin markets. The calibration is intended to absorb the specified shock scenario; the secondary transmission channels remain relevant and are precisely the cross-border vector the Eurosystem report is trying to address.

What the two cases together say about the Eurosystem proposal

Two deployments, three years apart, one template. Both explicitly framed by CBI as components of the same emerging macroprudential architecture. Property funds: slower-moving, single-jurisdiction, multi-year transition. LDI: fast-moving, cross-border, 18-month codification with monthly compliance reporting. Both build on the existing AIFMD machinery — Article 25 in the LDI case, Regulations 26 and 18 of the Irish AIFM Regulations in the property fund case — but apply that machinery for explicit financial-stability rather than investor-protection purposes. That is the analytical point DP11 makes: macroprudential mandate complements the investor-protection mandate; both can be advanced through the same regulatory infrastructure.

For the Eurosystem report’s reciprocation proposal, this matters in two specific ways.

First, the LDI case shows what cross-border coordination looks like when it works. CBI did not act unilaterally — it acted in deliberate coordination with CSSF and ESMA, and the codified frameworks are aligned across the two domiciles. That coordination was effective but bilateral and ad hoc. Under the Eurosystem report’s proposed reciprocation framework, similar action would have a defined process at EU level rather than depending on bilateral goodwill and the personal coordination of senior NCA staff. The LDI case is the existence proof; the reciprocation framework is the institutional infrastructure that would let it scale.

Second, the property fund case illustrates the gap that reciprocation is specifically designed to address. Article 25 AIFMD is a mandate exercised by the AIFM’s home regulator over the funds it authorises. But Irish commercial real estate could be held by funds domiciled in multiple EU jurisdictions; if a substantial share of the addressable Irish CRE market is held by funds authorised outside Ireland, CBI cannot apply its leverage limit to those vehicles. Domestic action is constrained by where funds happen to be domiciled, even when the underlying systemic exposure is unambiguously domestic. Reciprocation — under which other NCAs would apply equivalent measures to the funds they authorise that hold material Irish exposures — is the institutional missing piece. It is also the piece that is hardest to achieve voluntarily, because the reciprocating NCA must balance domestic priorities alongside measures designed primarily to address a foreign systemic risk (a classic collective-action problem in EU macroprudential policy).

The Eurosystem proposal puts this missing piece on the institutional table. Whether the Commission’s eventual legislative response carries it through is a separate question. But the analytical case for reciprocation is now anchored in two concrete deployments that have run for three and one years respectively, both of which expose the same gap in the existing architecture. Twelve years of German evidence support the empirical case for ex-ante liquidity tools. Three years of Irish institutional building support the case for the cross-border framework needed to deploy them at EU scale.

These cases make the implementation problem concrete.

Paweł Fiedor - The Macro Prudential View

Sources and methodology

Eurosystem and ECB

ECB (May 2026), Strengthening the macroprudential lens in the regulation of non-bank financial intermediation. Eurosystem report.

Bouveret, A.; Ferrari, M.; Grill, M.; Molestina Vivar, L.; Schmidt, D. J.; Weistroffer, C. (2025), Leveraged investment funds: A framework for assessing risks and designing policies. ECB Macroprudential Bulletin, Issue 26.

ESRB (2025), EU Non-bank Financial Intermediation Risk Monitor 2025, Table 3.

CBI

Discussion Paper 11 – An approach to macroprudential policy for investment funds, 18 July 2023.

The Central Bank’s macroprudential policy framework for Irish property funds, November 2022.

Industry letter: Liability Driven Investment Funds, 30 November 2022.

Central Bank introduces macroprudential measures for Irish-authorised GBP-denominated LDI funds, 29 April 2024.

Financial Stability Review 2025:II, Chart 39 and footnote 64.

Other regulators

Bank of England (December 2022), Financial Stability Report.

CSSF (29 April 2024), Macroprudential measures for GBP Liability Driven Investment funds.

ESRB (2021), Issues note on systemic vulnerabilities of and preliminary policy considerations to reform money market funds — referenced for the MMF-to-bank short-term funding channel.

The Pensions Regulator (April 2023), guidance on the use of leveraged liability-driven investments by trustees of defined benefit pension schemes.

Data

ECB Investment Fund Statistics (IVF) — Irish RE funds, monthly series.

Investing.com UK 30-year bond yield (nominal, weekly close).

Bank of England yield curves — real 30-year spot curve, daily.

Calculations. All flow statistics, decompositions and rolling volatility measures for the Irish property fund section are computed by The Macro Prudential View from the ECB IVF monthly series. Pre period: December 2014 to October 2022 (95 monthly observations). Post period: November 2022 to February 2026 (40 monthly observations) for flow statistics; November 2022 to November 2025 (37 monthly observations) for the AuM decomposition, because IVF Total Assets is missing for December 2025 to February 2026 and including those months would break the additive identity (Δ AuM = Net flows + Valuation + Δ Borrowing). Working spreadsheet available on request.

Views are my own. This article is a personal analytical piece based on public sources. It does not represent the views of the European Systemic Risk Board, the Central Bank of Ireland, the Eurosystem, or any other institution.