Private credit's circles of risk — and the wider NBFI architecture behind them

The FSB's first dedicated private credit report is best read as a window onto a wider problem: supervising the banking system alone is no longer sufficient.

The Financial Stability Board’s first dedicated report on private credit, published 6 May, lands at a moment when European regulators are visibly turning their attention to the asset class. Frank Elderson, vice chair of the ECB’s supervisory board, said in an interview reported by Barron’s that European private credit “bears watching.” Earlier this month, the Eurosystem published its own roadmap for strengthening the macroprudential framework around non-bank financial intermediation — and private credit features prominently.

What stands out about the FSB report, though, is that the most interesting thing in it isn’t private credit. It is the structural picture of bank–nonbank interconnection that emerges, almost by accident, from the report’s data-availability annex. Read carefully, the report is best understood not as an asset-class warning but as a diagnostic of broader NBFI supervision. Banks and NBFIs increasingly operate as what the European NGO Finance Watch has called “communicating vessels,” and supervisors only partially see the connections between them. Private credit matters not because it is unique, but because it makes that wider problem legible. The same circles of risk — leverage layering, fund-bank financing loops, synthetic risk transfer, cross-border intermediation, opaque valuation — appear across the NBFI ecosystem. They are easier to see in private credit right now because it has grown fast enough to attract dedicated supervisory attention. The Eurosystem’s May paper makes the same point in regulatory language: data gaps in private credit are part of a wider NBFI data strategy still being built.

It is worth saying at the outset what the FSB also says: direct bank lending to private credit funds, where it can be separately identified, is below 0.5% of total bank assets in the FSB member data; private credit can support economic activity, diversify lending across the system, and provide tailored financing to underserved borrowers. The argument here is not that direct exposures are obviously systemic. It is that, even where direct exposures look manageable, the intermediation web and the data gaps are the supervisory issue the report points to.

The rest of this piece reads the FSB report through that lens, drawing also on the ECB Financial Stability Review, the EBA Risk Assessment Report, the OFR’s recent brief on counterparty exposures, and the Eurosystem’s May paper. Five charts walk through the architecture, the supervisory range of uncertainty, the cross-border asymmetry that defines European private credit, the SRT loop that closes some of the circles, and finally the data-availability heatmap that explains why all of this remains poorly observed.

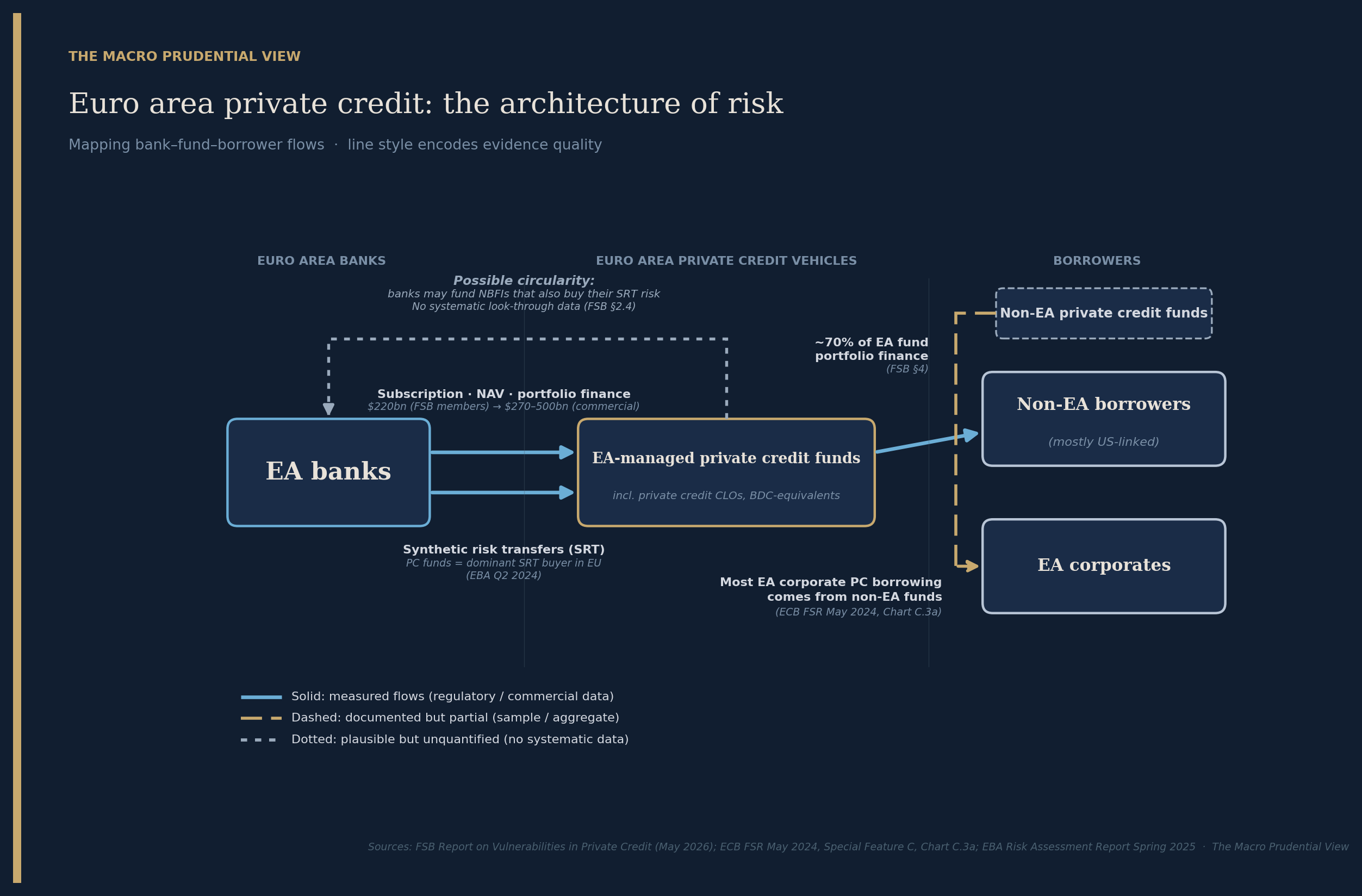

The architecture

Start with the structural picture. The FSB’s ecosystem diagram shows banks financing private credit funds through multiple facilities — subscription lines, NAV facilities, fund portfolio financing — while those same funds lend onward to corporate borrowers. The vertical axis of the schematic above replicates that: euro area banks lend to EA-managed private credit vehicles, which lend on to borrowers either inside or outside the area. The horizontal axis is the harder part. Three further flows complicate the picture, and the FSB names each of them.

First, the destination of euro-area fund portfolio finance is not euro-area corporates. About 70% of EA fund portfolio finance is directed to non-EU borrowers, the FSB reports — most of them US-linked. The euro area’s private credit fund infrastructure is, in significant part, intermediating credit to firms outside the bloc.

Second, euro-area corporates’ own private credit borrowing largely doesn’t come from euro-area lenders. The ECB’s May 2024 Financial Stability Review found that only around a fifth of private credit borrowed by EA companies is provided by EA-managed funds. The other four-fifths comes from outside the area — predominantly US managers operating cross-border.

Third — and this is where the FSB’s analysis gets most interesting — banks may remain indirectly exposed to credit risk they thought they had transferred. Through synthetic risk transfers (SRTs), banks transfer the credit risk of their loan books to investors while keeping the underlying loans on their balance sheets. The EBA reports that private credit funds are the largest single investor group in EU bank SRTs. And, as the FSB itself acknowledges, it remains unclear how far banks fund the very NBFIs that buy their SRT risk. When that loop closes, the economic risk may remain partly within the bank–NBFI perimeter even as the regulatory capital requirement against the underlying loans has been reduced.

The FSB calls these “circles of risks.” The phrase is appropriate. It is also a structural description that applies well beyond private credit.

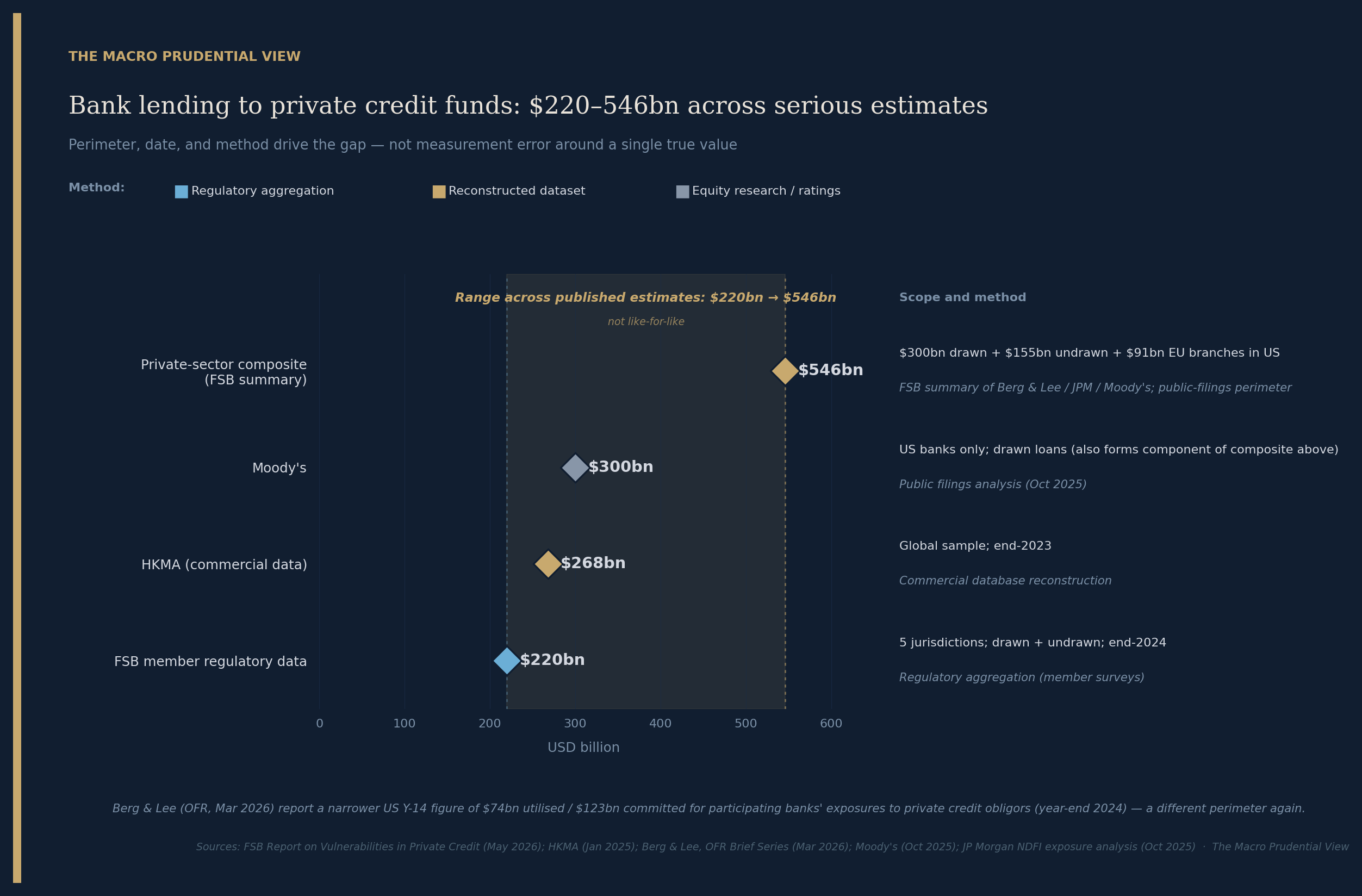

What we don’t know about size

Here is the most uncomfortable finding in the FSB report, and the one most easily missed. The report’s headline estimate of bank lending to private credit funds — about $220bn drawn and undrawn — is based on regulatory data from FSB member jurisdictions. But the report also references commercial and academic estimates that range up to $546bn for what is broadly a related perimeter.

The chart above shows where the four most-cited serious estimates land. The FSB member figure ($220bn, end-2024, five jurisdictions) is the lowest. The HKMA’s reconstruction from commercial data ($268bn, global, end-2023) sits modestly higher. Moody’s analysis of US bank filings ($300bn, drawn only, late 2025) is higher still. The FSB’s own summary of private-sector composite estimates puts the upper bound at $546bn — combining $300bn drawn loans, $155bn undrawn commitments, and $91bn from EU branches operating in the US, drawn from a body of research including Berg and Lee’s recent OFR brief (which itself, more narrowly, finds $74bn utilised and $123bn committed in US Y-14 data for participating banks).

The honest reading is not that supervisors see less than half of true exposure. It is that the available estimates measure different things — different geographies, different dates, drawn versus undrawn commitments, different scopes of what counts as “private credit” — and there is no harmonised perimeter to compare against. The spread is therefore not estimation error around a single number. It is a measurement of how much methodological choice drives the headline figure.

This is the data deficit story in one chart. It is also a leading indicator of the wider NBFI surveillance problem that the Eurosystem’s May paper is explicitly trying to fix.

A cross-border story Europe is not at the centre of

Of the three FSB findings sketched above, the one that should preoccupy European policymakers most is the cross-border asymmetry. The chart above puts it in a single panel.

Euro area-managed private credit funds direct roughly 70% of their portfolio finance outside the EU, predominantly to US-linked borrowers — the top bar. Euro area corporates, meanwhile, get roughly 80% of their private credit from non-EA lenders — the bottom bar. The two figures come from different but complementary datasets, and they tell the same story from opposite ends.

Read together, they suggest that the euro area sits in the middle of a cross-border intermediation chain rather than being the destination of either flow. EA fund infrastructure is helping place credit risk on mostly US-located corporate balance sheets. EA corporates are mostly funded by non-EA private credit funds. The euro area, in private credit, is a transit node — not a self-contained system.

What does this mean for supervision? At a minimum, it complicates the EA’s regulatory perimeter. The corporate credit risks that matter most for the euro area economy are largely originated outside it. The fund-level vulnerabilities most easily observed by EU supervisors — concentration, liquidity mismatch, leverage layering — increasingly relate to non-EA exposures. Effective monitoring requires looking at things the EA framework was not originally built to see.

This is not a uniquely private-credit problem. The same cross-border intermediation pattern appears in repo, derivatives, and prime brokerage. But private credit is the segment where the asymmetry is most clearly documented in recent regulatory work.

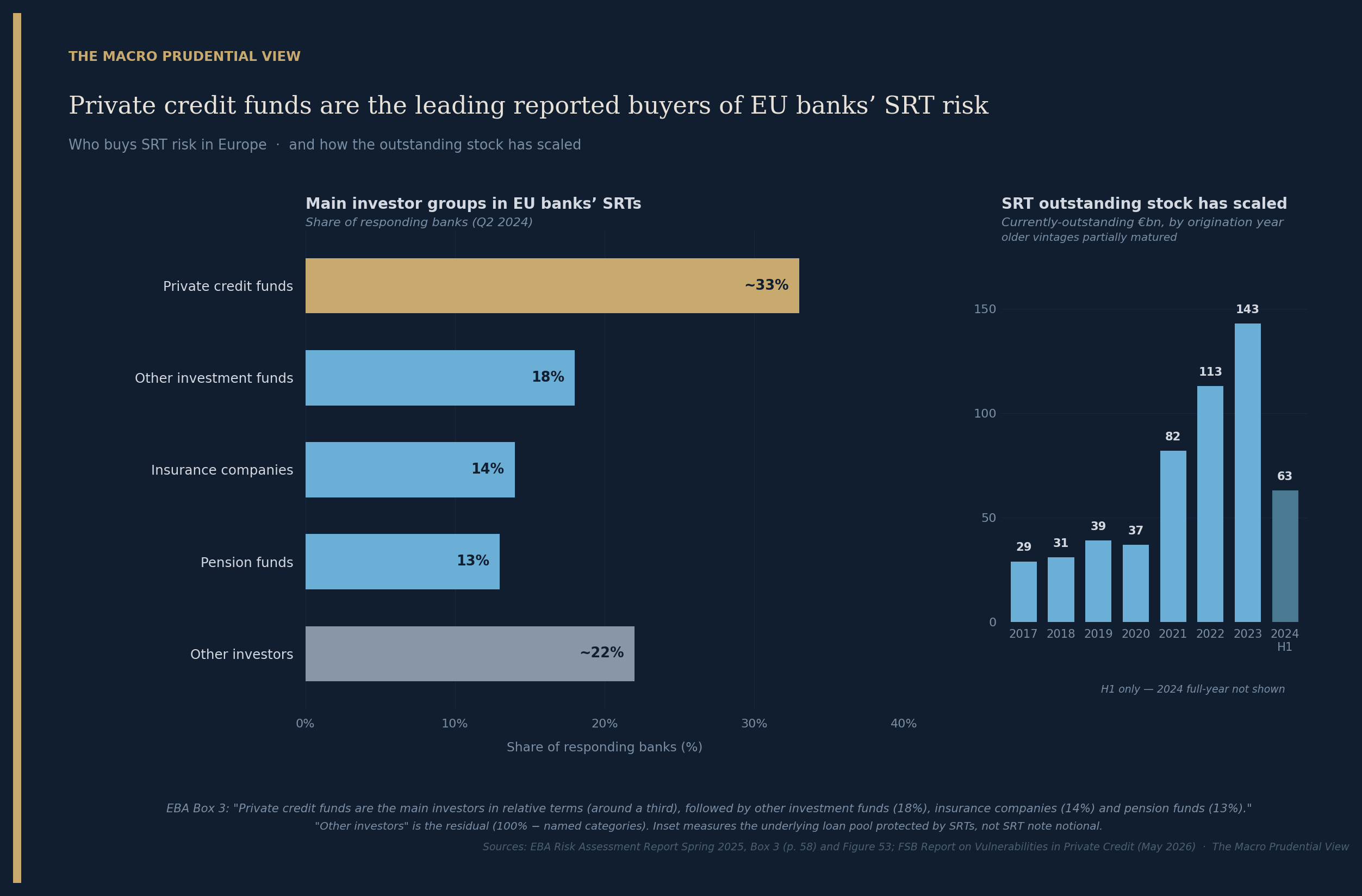

The SRT loop is closing

Now to the loop that gives private credit its specifically circular structure.

Synthetic risk transfers — instruments that move the credit risk of a bank loan book to outside investors while leaving the loans on the bank’s balance sheet — have grown rapidly. The right-hand panel above shows currently-outstanding protected loan pools by origination vintage, rising from around €30bn per year in 2017–2020 to €82bn in 2021, €113bn in 2022, and €143bn in 2023. The 2024 H1 partial-year figure of €63bn suggests another year close to or above the 2023 level. Older vintages have partially matured, so these are stock figures rather than annual issuance.

The left-hand panel, drawn from EBA reporting, shows who is on the other side of those transactions. Private credit funds are reported as the leading investor group, named by roughly a third of responding banks. Other investment funds, insurance companies, and pension funds account for another 45% between them, with a residual ~22% spread across asset managers, sovereign wealth funds, and other investor types.

This is where the FSB’s “circles of risks” language earns its plural. Some banks are simultaneously: financing private credit funds through credit lines; transferring loan credit risk to those same funds through SRTs; and holding revolving credit facilities with the corporates the PC funds are lending to. The motive for the SRT itself is regulatory capital relief — by transferring the credit risk of a loan book to outside investors, the bank reduces the risk-weighted capital it must hold against those loans. But when the same fund holds a bank’s SRT and receives that bank’s subscription financing — and the FSB acknowledges this is plausible but unquantified — the capital has been freed up while the economic exposure has not entirely left the bank–NBFI perimeter. The risk has been re-routed, not eliminated.

The supervisory response to this is hard. It requires look-through data that doesn’t currently exist at the regulatory level. The Eurosystem’s May 2026 paper identifies legal entity identifiers (LEIs) and a dedicated AIFMD subcategory for private credit funds as priority data infrastructure precisely to begin closing this gap. Until those are in place, the question of how much SRT risk is sitting inside fund vehicles that the same banks also finance is — to use the FSB’s own framing — a question.

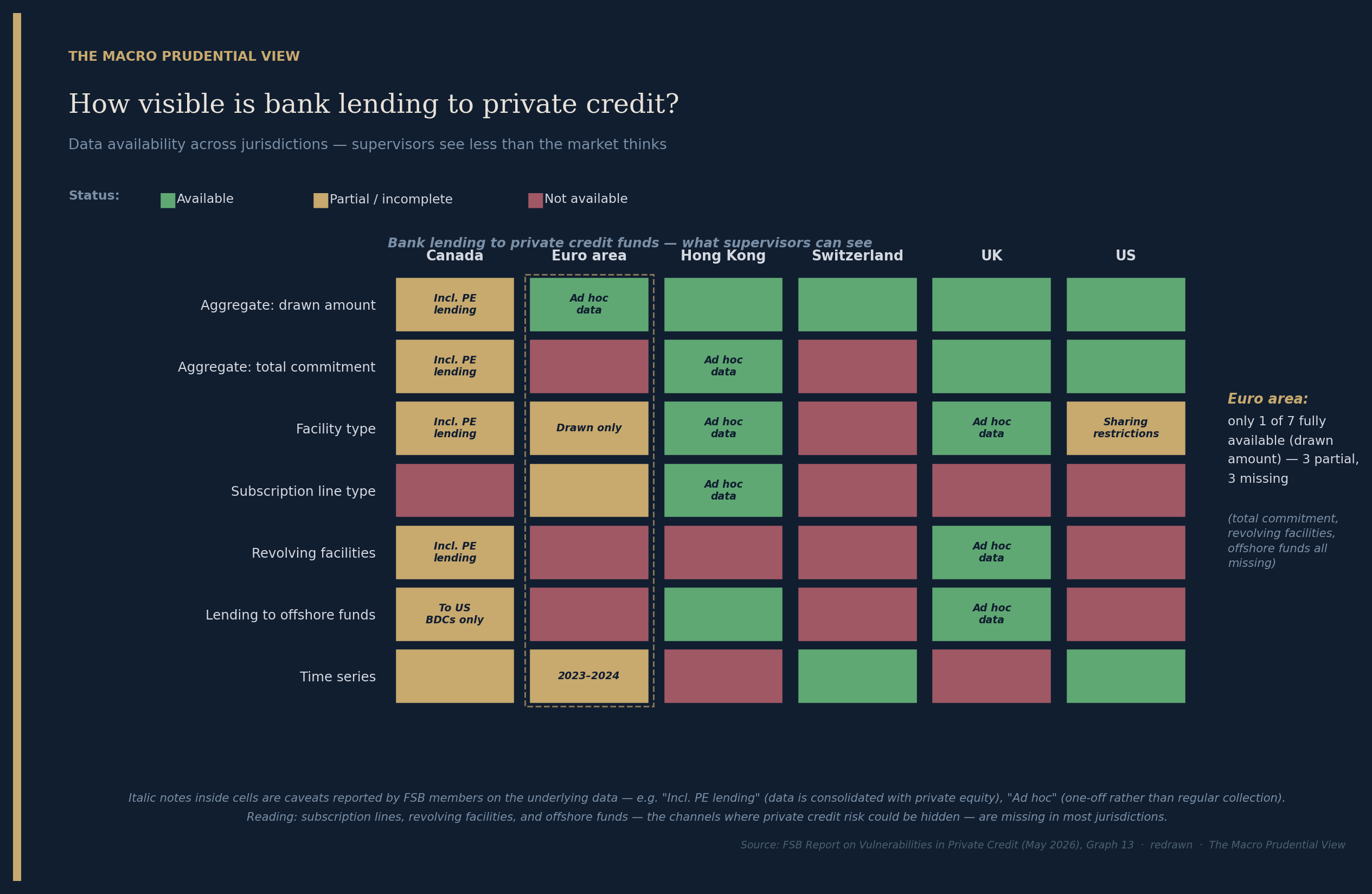

Why supervisors still can’t see most of this

The FSB report’s data annex contains what I think is the most important chart in the entire document, even though it sits near the back. Redrawn above, it shows what data is available to authorities in each major jurisdiction, by data category.

The story is not, as I initially expected, “US sees everything, EA sees nothing.” Look at the columns. The euro area can fully see aggregate drawn exposures (top row, green) but only via ad hoc collection. Total commitments — including undrawn lines — are missing. Facility-type breakdowns are partial. Subscription lines, the most common form of bank-to-fund financing, are only partially reported. Revolving credit facilities, lending to offshore funds, and granular time series are largely missing.

Look at the rows. The categories where private credit risk could be most plausibly hidden — subscription lines, revolving facilities, offshore fund exposure, granular time series — are red or yellow in most jurisdictions, including in the US. Switzerland is blind to most of the granular facility metrics, with five of seven categories missing. The UK and the US are the strongest reporters among the jurisdictions shown, but neither is comprehensive.

This is the supervisory deficit made concrete. The implication for the wider NBFI argument is direct: if this is what data availability looks like for the segment that has just received a dedicated FSB report, the surveillance situation for the broader NBFI sector — hedge funds, MMFs, securitisation vehicles, derivatives exposures — is no better, and in many places worse.

The Eurosystem’s May paper makes the same diagnosis. It proposes three priority interventions: targeted amendments to AIFMD, the UCITS Directive and related legislation to enable data sharing between the ECB, ESRB, ESMA, and national supervisors; a centralised data access mechanism, with ESMA exploring a data hub as part of an integrated reporting framework; and mandatory use of LEIs across NBFI reporting, including for private credit funds. The paper also proposes amending ESMA’s AIFMD guidelines to introduce a specific AIF subtype for private credit funds — directly addressing the residual-category problem that today makes EU private credit hard to identify in regulatory data.

These are not glamorous proposals. They are plumbing. But they are the right plumbing to fix, and the FSB heatmap above is the diagnostic that makes the case for them.

What the FSB report is really about

The FSB report can be read in two ways. The narrower reading treats it as a specific assessment of a fast-growing asset class — useful, careful, not particularly novel. The wider reading, which I find more interesting, treats it as a diagnostic of NBFI supervision: a worked example of what we know and don’t know about a single segment of market-based credit intermediation, written by people who clearly understand the limits of their own evidence.

Finance Watch’s recent report on systemic risk from shadow banking makes the wider case explicitly. Banks and NBFIs, they argue, function as communicating vessels — connected via leverage, funding, securitisation, derivatives, and liquidity channels that supervisors only partially see. The FSB’s circles-of-risks language is the same point in narrower form. So is the Eurosystem’s proposal to build a centralised NBFI data infrastructure. So is the ESRB Advisory Scientific Committee’s reported consideration of a formal private credit inquiry.

What’s notable is that these efforts are converging. The diagnosis is broadly shared: NBFI is now a large enough share of global financial assets that supervising the banking system alone is no longer sufficient. The prescriptions are still being assembled — data infrastructure first, then macroprudential tools, eventually possibly entity-level designations of systemically important NBFIs.

Private credit is where the architecture is currently easiest to see in Europe. That is partly because it has grown fast, attracted political attention, and become the subject of a dedicated FSB report. It is also because — paradoxically — private credit’s interlinkages with banks are more visible than those of other NBFI segments, precisely because banks are involved at every step. The FSB report is therefore both an asset-class document and, more interestingly, a structural map.

Read it as the structural map. The risk of circular exposures is real. The data to confirm or refute the more concerning interpretations is not yet available. The Eurosystem is building the surveillance infrastructure that would make better answers possible. The recent publications suggest these theoretical risks are increasingly being viewed as supervisory priorities rather than abstract concerns.

What we are watching, in short, is the start of a wider NBFI supervisory framework being assembled — with private credit as the most legible test case.

Paweł Fiedor - The Macro Prudential View

The views expressed are the author’s own and do not necessarily reflect those of any institution with which the author is or has been affiliated.

Sources: FSB, Report on Vulnerabilities in Private Credit, 6 May 2026 — https://www.fsb.org/uploads/P060526.pdf; Eurosystem, Strengthening the macroprudential lens in the regulation of non-bank financial intermediation, May 2026 — https://www.ecb.europa.eu/press/intro/publications/pdf/ecb.ebaecb202605.en.pdf; ECB, Financial Stability Review May 2024, Special Feature C — https://www.ecb.europa.eu/press/financial-stability-publications/fsr/special/html/ecb.fsrart202405_03~bc23a48dbc.en.html; EBA, Risk Assessment Report Spring 2025; Berg and Lee, Measuring Counterparty Exposures to Private Credit, OFR Brief Series, March 2026 — https://www.financialresearch.gov/briefs/files/OFRBrief-26-02-measuring-counterparty-exposures-private-credit.pdf; Finance Watch, Systemic risk from shadow banking — https://www.finance-watch.org/policy-portal/stability-supervision/report-systemic-risk-from-shadow-banking/; Barron’s, “Europe’s Regulators May Launch Private Credit Inquiry,” — https://www.barrons.com/articles/europe-private-credit-probe-c22ea2dc.