Stablecoins, Sanctions and the Strait of Hormuz

From regulatory arbitrage to maritime chokepoints — why the macroprudential case against stablecoins just got harder to ignore

Last week I used the IMF’s Global Financial Stability Report to make the case that ETF hoarding and passive flows were quietly reshaping emerging market debt dynamics. This week I am back at the same well. The GFSR, it turns out, has more to give — and the news cycle has helpfully provided a real-world stress test of one of its central anxieties.

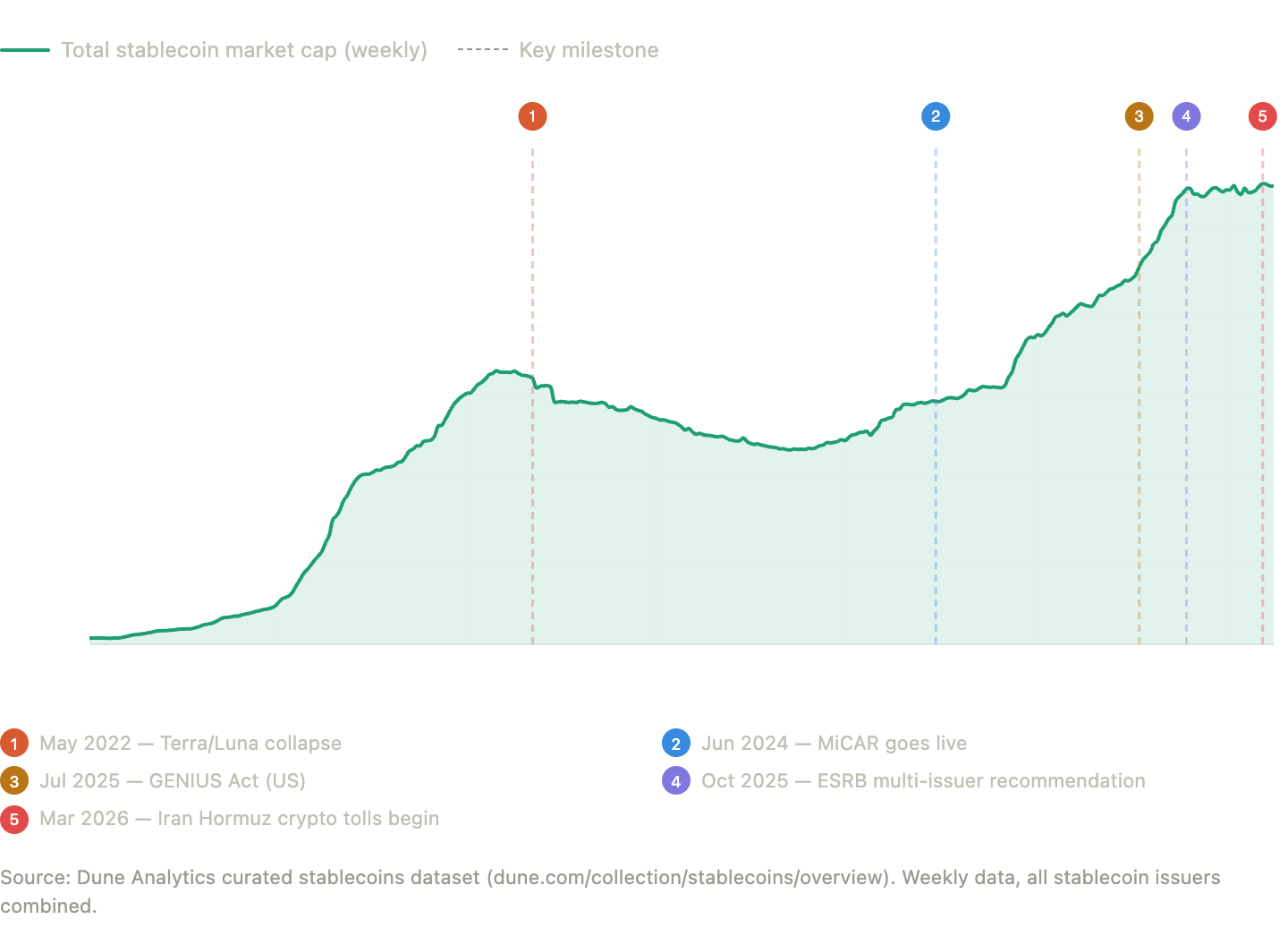

The anxiety in question is stablecoins. Not the crypto-bro version of the argument — moon, lambos, number go up — but the macroprudential one. The IMF, the European Systemic Risk Board, and a handful of serious monetary economists have spent the past eighteen months constructing a framework for thinking about stablecoins as a financial stability problem. That framework now has a live case study: the Strait of Hormuz, where Iran’s Islamic Revolutionary Guard Corps has been collecting transit tolls from oil tankers in Bitcoin and USDT since mid-March 2026. Theory, meet practice.

Part I: What the IMF actually said

The April 2025 GFSR dedicated prominent analysis to crypto assets and stablecoins, and its tone was notably less hedged than the Fund’s usual register. The central concern is what the IMF calls “cryptoization” — the process by which residents of countries with weak or compromised monetary frameworks substitute dollar-pegged stablecoins for their domestic currency. This is dollarization by another name, but faster, cheaper, and harder to monitor. You do not need a US bank account to hold USDT. You need a smartphone.

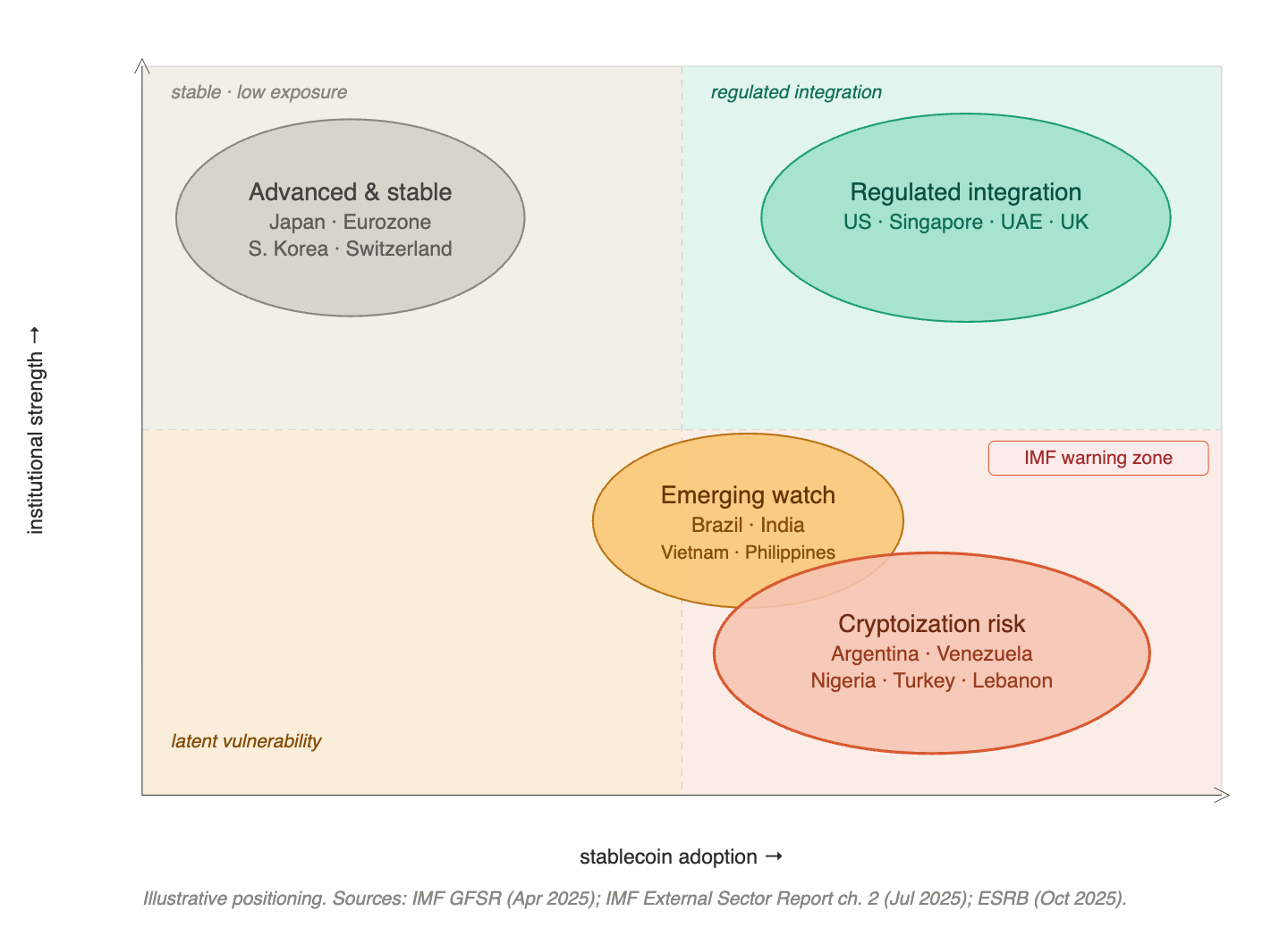

The IMF’s concern is not symmetrical across countries. In advanced economies with deep financial markets and credible central banks, stablecoin adoption is largely a regulated integration story — a new payment rail sitting alongside existing infrastructure. The risk is different in economies with high inflation, volatile exchange rates, and weak institutional anchors. There, stablecoin adoption can quietly hollow out domestic monetary transmission, erode the central bank’s balance sheet, and accelerate capital flight in ways that are nearly invisible to conventional surveillance tools.

The countries named or implied in the GFSR — Argentina, Turkey, Nigeria, Lebanon, Venezuela — are not accidental. These are places where the dollar has long served as an informal unit of account and where stablecoin adoption is driven not by convenience but by survival. What is new is the scale and speed. The IMF’s July 2025 External Sector Report noted that stablecoin flows relative to GDP are most significant in Latin America and the Caribbean, and in Africa and the Middle East — precisely the regions with the greatest institutional vulnerability.

There is a second concern that sits at the opposite end of the risk spectrum but is equally striking. Stablecoins are not just a monetary sovereignty problem for fragile economies. They are becoming a structural feature of the US Treasury market.

Hélène Rey of the London Business School has argued that this dynamic amounts to the privatisation of global seigniorage — concentrating in a handful of private companies a function that central banks have exercised for centuries. The beneficiaries, she notes, are likely to be few given the strength of network externalities, with significant implications for the political economy of regulation.

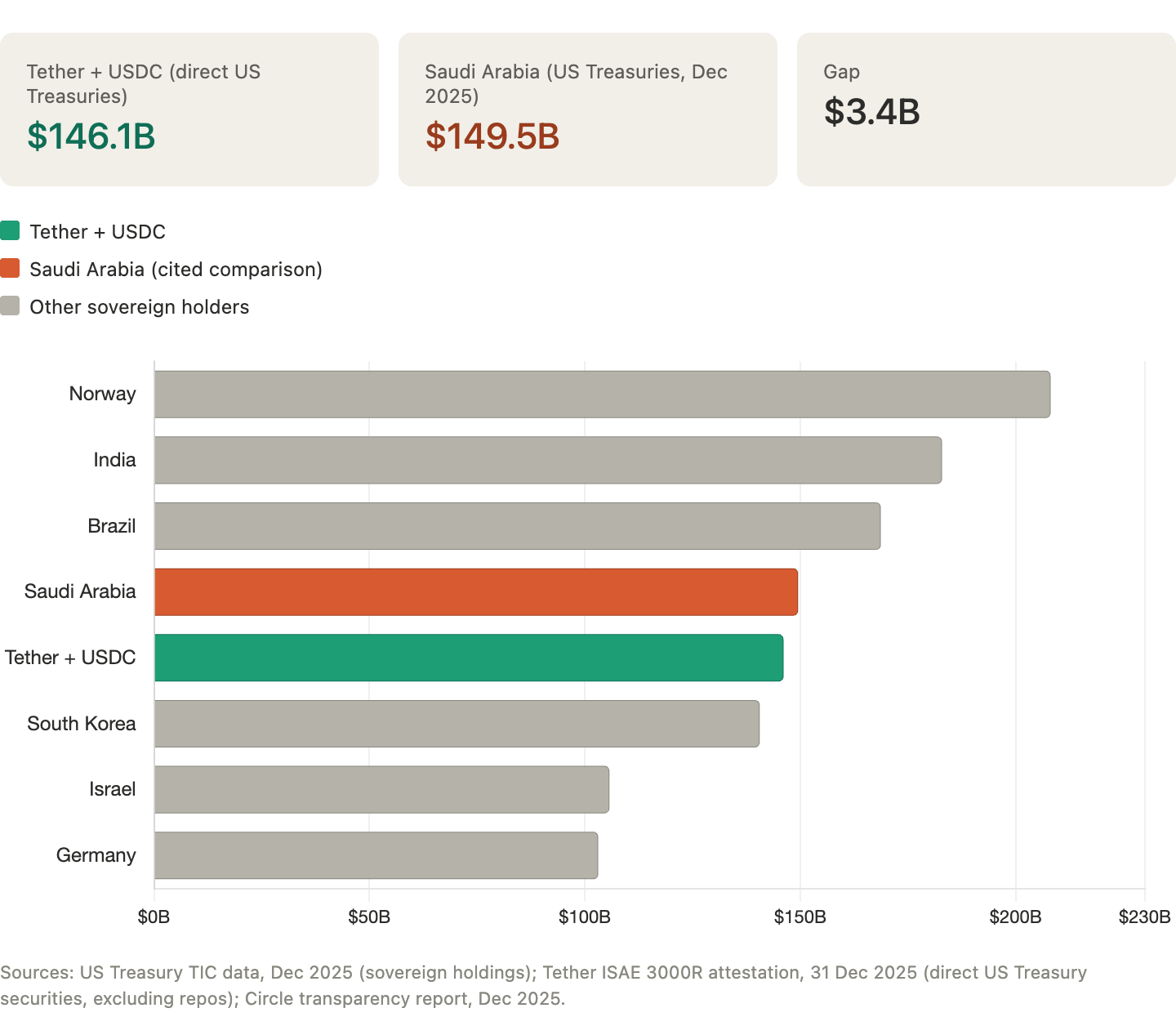

Tether and USDC combined held approximately $146 billion in direct US Treasury securities at end-2025 (Tether's independently attested direct holdings were $122bn per its ISAE 3000R attestation, with Circle USDC comprising the remainder) — within $3.4 billion of Saudi Arabia’s holdings, and comfortably in the same league as Norway, India and Brazil. The IMF’s July 2025 External Sector Report flagged this directly, noting that at an earlier point in the year the two issuers collectively held more Treasuries than Saudi Arabia. The figure has since converged as Saudi Arabia’s holdings grew, but the point stands: two private companies, accountable to no central bank and subject to no formal reserve requirements under US law until the GENIUS Act passed in July 2025, had quietly become systemically relevant holders of the world’s benchmark safe asset. A confidence shock — a stablecoin run — would not stay in crypto markets. It would land in short-term Treasuries.

Part II: The ESRB and the multi-issuer loophole

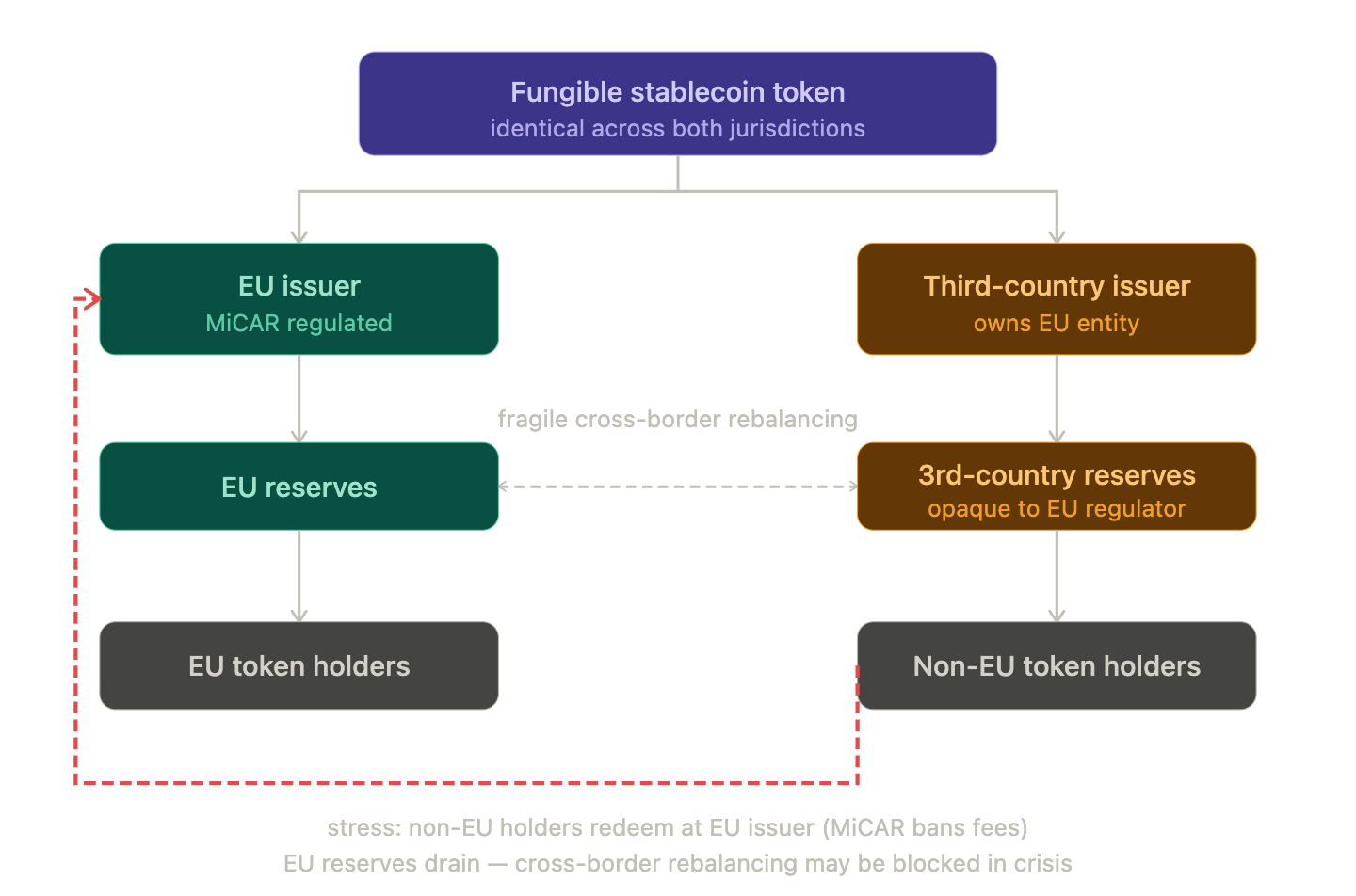

European regulators have been watching a more specific structural vulnerability develop on their doorstep. The ESRB’s October 2025 report on crypto assets identified what it called the multi-issuer stablecoin problem, and issued a formal recommendation — ESRB/2025/9 — urging the European Commission to clarify that these schemes are not permissible under MiCAR.

The mechanics are worth understanding because they are the kind of thing that looks innocuous until it isn’t. A multi-issuer stablecoin involves an EU-regulated entity and a third-country entity — typically the parent company — co-issuing what is legally and technically a single, fungible token. The reserves backing the token are split across jurisdictions. Under MiCAR, the EU issuer is prohibited from charging redemption fees and must redeem at par, at any time. The third-country issuer faces no such constraint. In a stress scenario, non-EU token holders have a strong incentive to seek redemption through the EU entity — better terms, legally enforceable rights, a regulated counterparty. The EU issuer then faces redemption pressure it cannot fully hedge, from a reserve pool it cannot fully see, under a cross-border rebalancing mechanism that the ESRB explicitly describes as fragile.

Richard Portes of the London Business School, who co-chaired the ESRB’s Crypto Asset Task Force, has written up the academic case for urgency in a VoxEU column published in late 2025. His argument is direct: the multi-issuer loophole, if left unaddressed, exposes the EU financial system to contagion from crises originating in third-country jurisdictions, with EU supervisors holding responsibility for liabilities created entirely outside their remit.

The European Commission, as of writing, has not formally ruled the schemes impermissible. Several members of the European Parliament have written to Commissioner Albuquerque expressing concern. ECB President (and ESRB Chair) Lagarde has been more forthright in her public opposition. The institutional standoff is unresolved, which is part of what makes the ESRB recommendation significant — it is not an academic intervention but a formal macroprudential alarm from the body charged with systemic risk oversight in the EU.

Part III: The Strait of Hormuz — theory meets geopolitics

Which brings us to the news hook that makes all of the above feel less theoretical than it did a month ago.

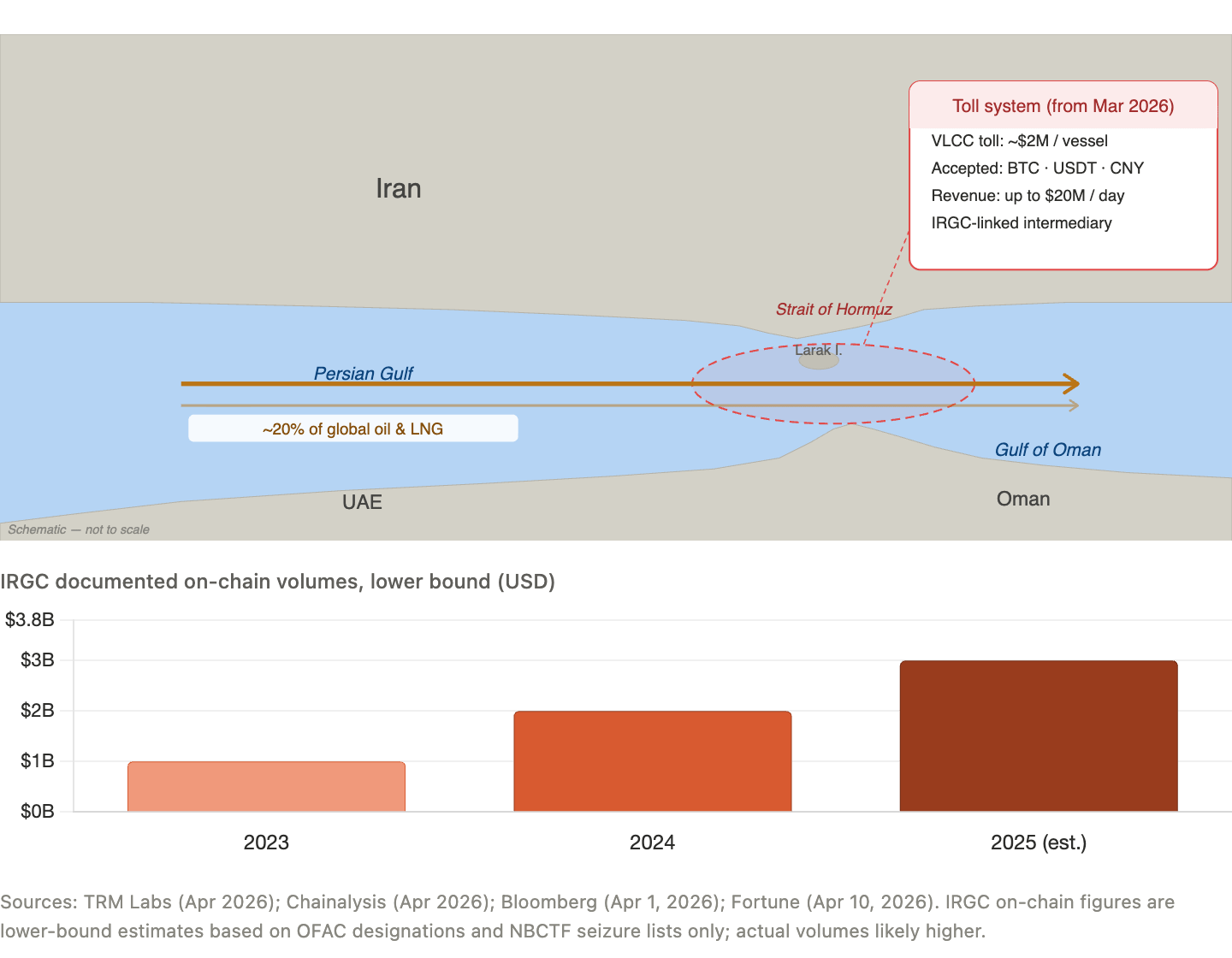

Since mid-March 2026, Iran’s IRGC has been charging oil tankers up to $2 million per vessel to transit the Strait of Hormuz, accepting payment in Bitcoin, USDT, and Chinese yuan routed through Kunlun Bank outside SWIFT. Iran’s parliament formally codified the system in the “Strait of Hormuz Management Plan,” approved on 30–31 March 2026. At current traffic levels, public estimates from TRM Labs suggest the toll system could generate up to $20 million per day from oil tankers alone, with $600–800 million per month possible if LNG vessels are included.

This is the first time a state has deployed stablecoin infrastructure as a sovereign revenue mechanism at a major maritime chokepoint. It is not, however, a departure from Iran’s existing financial playbook. It is an extension of it. Chainalysis has documented IRGC-attributed on-chain activity growing from approximately $1 billion in 2023 to over $3 billion in 2025, based on OFAC designations and NBCTF seizure lists — figures that represent a lower bound, since they cover only identified wallets. The IRGC’s documented flows have overwhelmingly relied on stablecoins rather than Bitcoin, for reasons that are straightforward: stablecoins offer dollar-denominated value, high throughput, deep liquidity, and no issuer that can easily freeze an account.

That last point is important. In March 2026, Tether froze $6.7 million tied to IRGC and Houthi-linked networks. Bitcoin cannot be frozen by anyone. The choice of payment rail reflects operational learning about where the vulnerabilities in each system lie.

As this piece goes to press the situation is live and escalating. Iran declared the strait open on 17 April in line with a Lebanon ceasefire, then reversed course within 24 hours, reasserting “strict control” until the US lifts its naval blockade of Iranian ports. IRGC gunboats attacked a tanker on 18 April — no injuries, but a significant escalation. The ceasefire expires mid-week, with Pakistani-led mediation scrambling to extend it. What is not in flux is the underlying infrastructure: the toll system, the crypto payment rails, and the IRGC’s on-chain apparatus predate this crisis and will outlast any particular ceasefire. The Hormuz situation is the stress test — not the source of the vulnerability.

A brief note on epistemic caution: TRM Labs’ own Ari Redbord told Fortune that he was sceptical crypto was being used at scale for toll payments as opposed to being signalled as an available option. The situation was, in his words, “incredibly fast moving.” Subsequent on-chain reviews by Chainalysis (10 April) have reached the same conclusion. The Chainalysis framing is more bullish on the significance. Both are worth reading. What is not in dispute is that Iran has built the infrastructure for stablecoin-denominated state revenue collection and has been using it for sanctions evasion at scale for several years. The Hormuz toll system is the most visible deployment of that infrastructure, not its origin.

There is one political economy footnote that deserves a sentence. One commentator observed that if Iran were to demand payment specifically in USD1 — the stablecoin affiliated with the Trump family’s World Liberty Financial — the President of the United States would face a financial incentive to lift sanctions. The observation is not presented here as a prediction. It is presented as an illustration of how private stablecoin infrastructure can become entangled with geopolitical incentives in ways that conventional financial plumbing simply does not permit.

Part IV: Putting it together

The IMF, the ESRB, and Richard Portes have all been making versions of the same argument in measured institutional language: stablecoins are no longer a crypto-native curiosity. They are monetary infrastructure with systemic implications, and the regulatory frameworks governing them are running several years behind their actual footprint.

The framework they offer can be summarised across five interlocking risks. First, reserve concentration: if a major stablecoin issuer faces a confidence shock, the forced liquidation of its Treasury holdings could disrupt short-term funding markets well beyond crypto. Second, cryptoization: in fragile economies, dollar-pegged stablecoin adoption is quietly hollowing out domestic monetary sovereignty in ways that are hard to reverse. Third, regulatory arbitrage: the multi-issuer loophole is the EU-specific version of a global pattern in which jurisdictional gaps between stablecoin issuers create run risk and supervisory blind spots. Fourth, sanctions evasion: Iran has demonstrated that stablecoin infrastructure can function as a parallel financial system for a comprehensively sanctioned state, and the architecture is available to others. Fifth, dollar exorbitant privilege 2.0: the proliferation of dollar-backed stablecoins may reinforce rather than undermine dollar dominance, but it does so by privatising seigniorage — concentrating it in a handful of companies whose governance and accountability bear no resemblance to a central bank.

None of these risks is yet systemic in the sense that regulators use that word carefully. The IMF is explicit about this. Stablecoin market capitalisation remains small relative to global currency flows, and the transmission channels to traditional financial markets are still developing. But the pace of development — market cap roughly doubling in two years, IRGC volumes tripling, multi-issuer schemes securing MiCAR authorisation before the regulatory framework could catch up — is precisely the dynamic that macroprudential frameworks are designed to flag before the fact rather than respond to after.

The GENIUS Act in the US, MiCAR in Europe, and the ESRB’s recommendation are all attempts to close the gap. Whether the European Commission acts on the ESRB’s advice before the next stress test arrives is an open question. The Strait of Hormuz did not wait for an answer.

The Macro Prudential View is published weekly. If you found this useful, please share it.