The Benchmark That Binds No One

The Commission found Europe's money market funds resilient and answered with a benchmark no fund is obliged to meet, set where the sector already sits.

On 11 May the European Commission delivered its report on the functioning of the Money Market Fund Regulation. The EU’s €1.95 trillion sector, it found, has grown by close to half since 2019 and came through both the March 2020 dash for cash and the 2022 gilt crisis without a single fund gating or suspending redemptions. Funds hold liquidity comfortably above the regulatory minima. The appropriate response, the Commission concluded, was not to reopen the Regulation but to set a non-binding supervisory benchmark: weekly liquid assets of around 40% for the stable-value funds, against a binding floor of 30%.

On 14 May, HM Treasury and the FCA confirmed the opposite instinct. Having consulted on this since 2023, the UK announced it will legislate to raise its binding liquidity requirements and, more consequentially, to sever the regulatory link between a fund’s liquidity level and the tools that let it slow or stop redemptions. The new regime is expected to be in place by the end of 2026.

The two documents describe the same instrument, draw on the same two crises, and read off much the same data; they reach opposite conclusions about what to do.

There is a third party to the disagreement, and it had already cast its vote. Fifteen months earlier, in February 2025, the European Systemic Risk Board graded the Commission materially non-compliant with the recommendations it had issued in 2021 on precisely this question. The assessment was neither gentle nor fringe: the team included Richard Portes and was chaired from within ESMA. On three of the four headline recommendations — the ones that would have changed the funds’ structure and their liquidity — the Commission had taken no action, and its justifications were judged insufficient.

That grade measured the Commission’s response against the ESRB’s recommendations: it records that the action fell short of what was asked, not that the sector failed a test. Even read that narrowly, it means the Commission reached its reassurance over the objection of the authority it sits beside on systemic risk, on a reform agenda that authority still judges unfinished. Working out who has the better of it means being precise about what a liquidity buffer measures, and what lies beyond its reach.

A short word on the LVNAV

European regulation offers three kinds of money market fund. Public-debt constant-NAV funds hold government paper and maintain a fixed share price. Variable-NAV funds let their price float with the value of their assets. Between them sits the low-volatility NAV fund, the LVNAV, which is the one that matters here and the largest single category in Europe at roughly 46% of the sector.

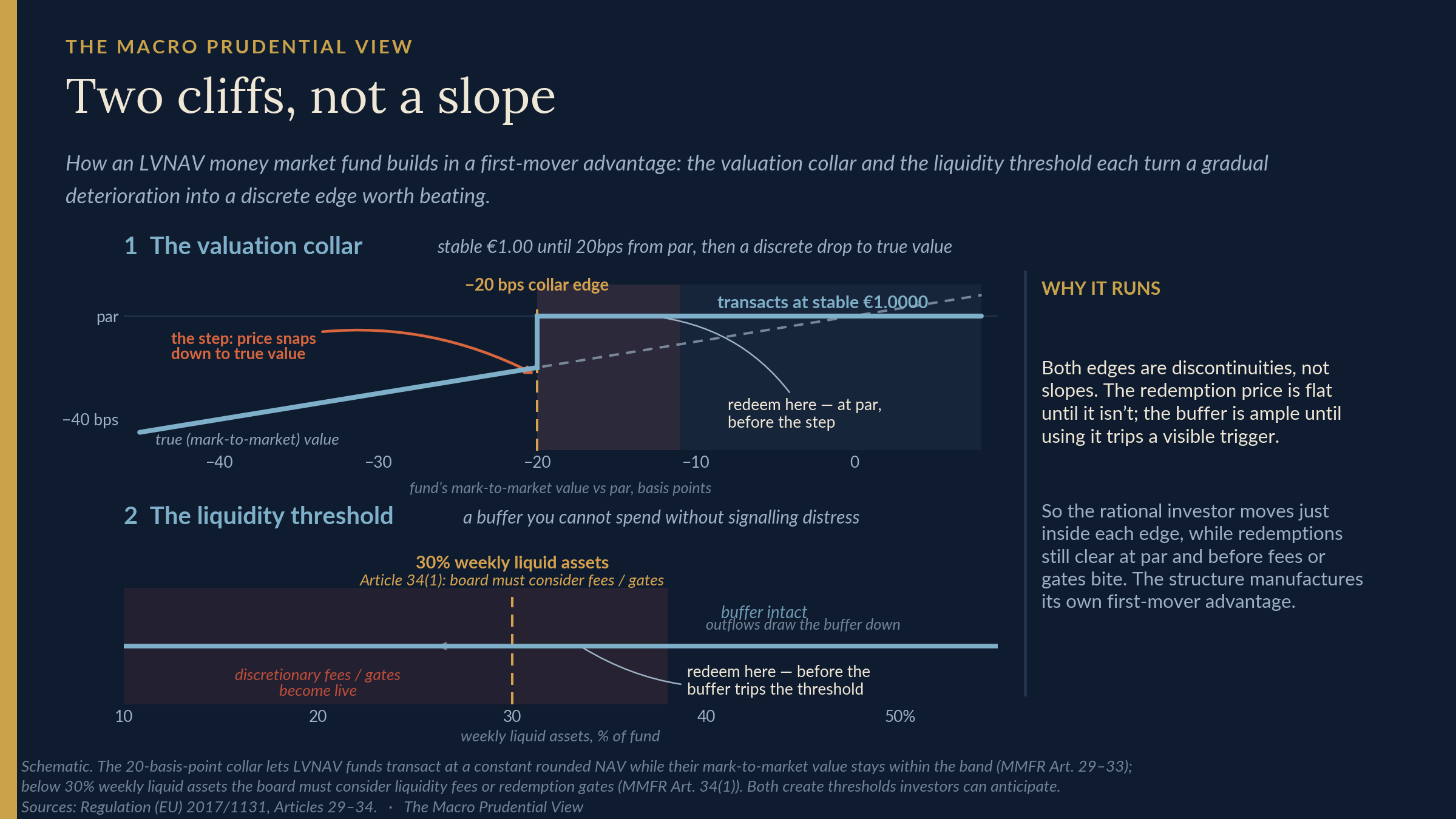

The LVNAV is a hybrid by construction. It values its assets at amortised cost and rounds its share price to a stable €1.00, but only while its true mark-to-market value stays within twenty basis points of par. Step outside that collar and the fund must price at its real value, like a VNAV. The stability is therefore conditional, and the condition is invisible to the investor until the moment it fails. That is the feature corporate treasurers pay for: cash that looks and settles like a deposit. It is also where the fragility sits. The Commission understood as much once — its own 2013 impact assessment warned that a constant share price “triggers false incentives and exacerbates runs.”

Why a money fund runs

The collar builds in a cliff. A fund whose assets are quietly losing value still transacts at €1.00, right up to the twenty-basis-point edge, at which point the price drops to meet reality. An investor who redeems while the fund is inside the collar gets out at par. An investor who waits until it breaks absorbs the loss the early movers left behind. The collar holds the price flat and then moves it in a single step, so the deterioration that a floating fund would show gradually arrives here all at once.

The Regulation adds a second cliff beside the first. When a fund’s weekly liquid assets fall below 30%, its board is obliged to consider imposing fees or redemption gates. The trigger is discretionary, not automatic. But investors do not need it to be automatic; they need only to anticipate it. Watching the buffer approach 30%, a holder knows a breach may bring restrictions, so the moment to leave is before the threshold is reached, while redemptions still clear freely and at par. The discontinuity that matters is in the behaviour, not in the text of the rule.

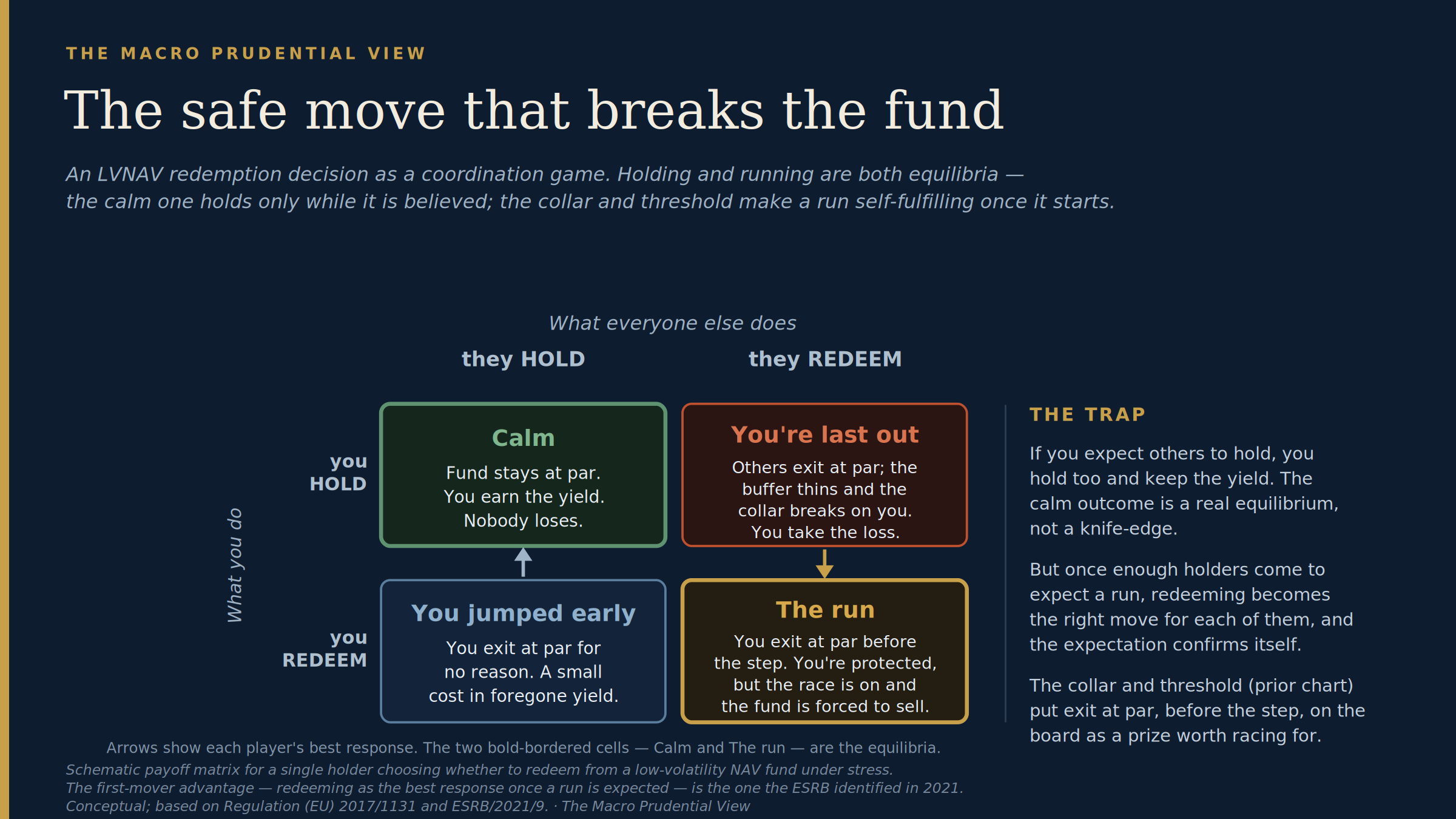

Put the two together and the redemption decision becomes a coordination game with two equilibria, one of them bad.

If you expect other investors to sit tight, you sit tight too: the fund holds at par, you keep the yield, and redeeming would only cost you a little of it. If you expect them to run, the calculation inverts, and redeeming becomes the one way to get out at par, ahead of the step and ahead of any gate. Holding and running are both equilibria, and which one obtains depends on what each investor believes the others will do.

The fragility is in the second equilibrium. The calm one holds only while everyone trusts that it will hold. Any event that shifts enough investors toward expecting a run makes running the correct response for each of them individually, and the expectation then confirms itself. The collar and the threshold are what give the run its edge, because they put a discrete prize on being early: exit at par, before the step. This is the first-mover advantage the ESRB identified in 2021. It does not require panic or misjudgement; it follows from the payoffs.

There is a corollary the Commission’s own evidence supports and its conclusion passes over. If drawing on a buffer is what signals distress and trips the threshold, managers will be reluctant to draw on it. The ESRB found exactly this when it examined March 2020: funds suffered heavy outflows but did not run their weekly liquid assets down to match, which the assessors read as “low levels of usability” for the buffers. A buffer that a manager will not spend, for fear that spending it invites the run, is worth less in an event than its headline size suggests.

The constraint outside the fund

The report measures resilience as a fund’s ability to meet redemptions out of its own liquid assets without forced selling. On that measure the sector looks sound, because funds do hold liquidity well above the minima. The measure is a single-fund one, though, and money funds are tested by system-wide events: in a stress, every fund holds similar paper and reaches for cash at the same moment.

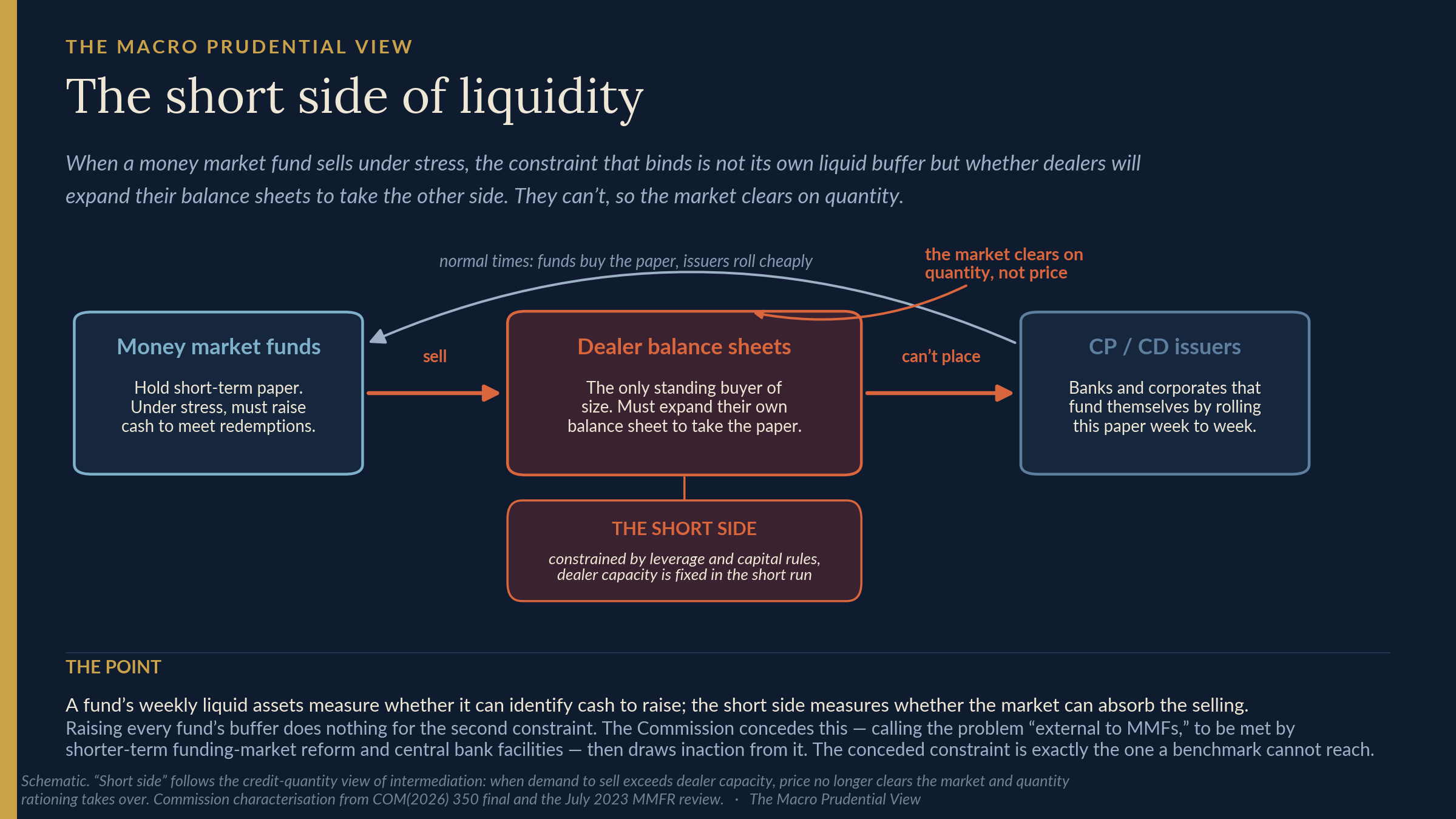

Start with how a fund actually raises that cash, because the intuitive version of the short-side argument goes wrong here. Weekly liquid assets are not mostly a stock of sellable securities; they are largely paper maturing within the week. A fund under redemption pressure meets it first by letting that paper mature and collecting the proceeds, and by declining to reinvest. It does not have to sell commercial paper into a thin market to find the cash. For the individual fund, the buffer works more or less as designed.

The strain does not disappear; it moves to the issuer. When a money fund collects its maturing paper and declines to roll, the issuer that sold that paper — a bank or a large corporate funding itself week to week — has to refinance somewhere else. The natural buyers of the new paper are money funds, and in a system-wide event they are all doing the same thing at once: husbanding cash rather than extending it. So the issuer cannot roll at the old size or the old price. The pressure the fund relieved on its own balance sheet reappears on the issuer’s, at the rollover margin. And it does not stay wholly on the issuer’s side. A fund meets this week’s redemptions from maturing paper, which pays at par, so the buffer does its job there. The credit strain lands instead on the same issuer’s longer-dated paper, still on the fund’s books: it reprices as the issuer’s spread widens, and in the extreme, if the issuer defaults, even maturing paper stops paying in full. That is what moves the shadow NAV toward the collar. Holding more weekly liquid assets reduces this exposure, since it leaves a smaller spread-sensitive long book, though it does nothing for the dealer-capacity limit that decides whether the issuer can refinance at all. None of this puts issuer-side strain in a separate regulatory silo: it returns to the funds through their own asset marks.

Dealers are meant to bridge exactly this kind of gap, standing in to buy paper that cannot immediately be placed. Their capacity to do so is fixed in the short run by leverage and capital rules, and when the whole sector turns at once it is quickly exhausted. Price impact becomes severe, and at the margin some issuance cannot be placed at a price the issuer can pay. The adjustment then runs through quantities — issuance abandoned, rollovers refused — and not through price alone. A fund’s weekly liquid assets tell you whether that fund can find cash. They tell you nothing about whether the market can absorb every fund finding cash together. Raising every fund’s buffer improves the first and relocates the second rather than resolving it: each fund is individually safer, while the aggregate strain shifts onto issuers and a dealer sector that cannot grow to meet it. A higher buffer changes the timing and size of that strain; it does not create the capacity to absorb it.

None of this is new, and the piece is better for not pretending otherwise. The role of dealer balance-sheet capacity as the binding constraint on absorbing forced sales, with quantity rationing taking over from price once that capacity is reached, is the standard reading of the 2020 dash for cash. The Financial Stability Board’s Holistic Review of the March Market Turmoil set it out at the official level in November 2020, and it runs through the central banks’ own accounts of why they intervened and the wider market-based-finance literature. The Federal Reserve stood up two facilities in March 2020, not one: a money market fund liquidity facility to take funds’ assets, and a commercial paper facility to backstop issuance. Both channels had seized — the fund-level and issuer-level constraints are one constraint seen from two ends.

The Commission sees this. Its report accepts that dealer liquidity provision is more constrained and less responsive than before 2008, characterises much of the problem as external to the funds, and points to the right remedies: deeper short-term funding markets and access to central-bank facilities. Having located the binding constraint outside the Money Market Fund Regulation, it concludes that the Regulation itself needs no substantive change. That is where the diagnosis and the conclusion stop fitting together. An external constraint is a reason a fund-level buffer cannot fix the system; it is not a reason to leave every other lever untouched, including the levers, such as the run-inducing threshold and the stable share price, that sit squarely inside the Regulation. This is not a call for a bigger buffer to do a buffer’s impossible job. A higher, usable floor buys fund-level resilience while the systemic gap still needs the external tools the Commission names; the complaint is that the Commission declined the structural levers it did control and answered with a benchmark no fund is obliged to meet.

Three regimes, three answers

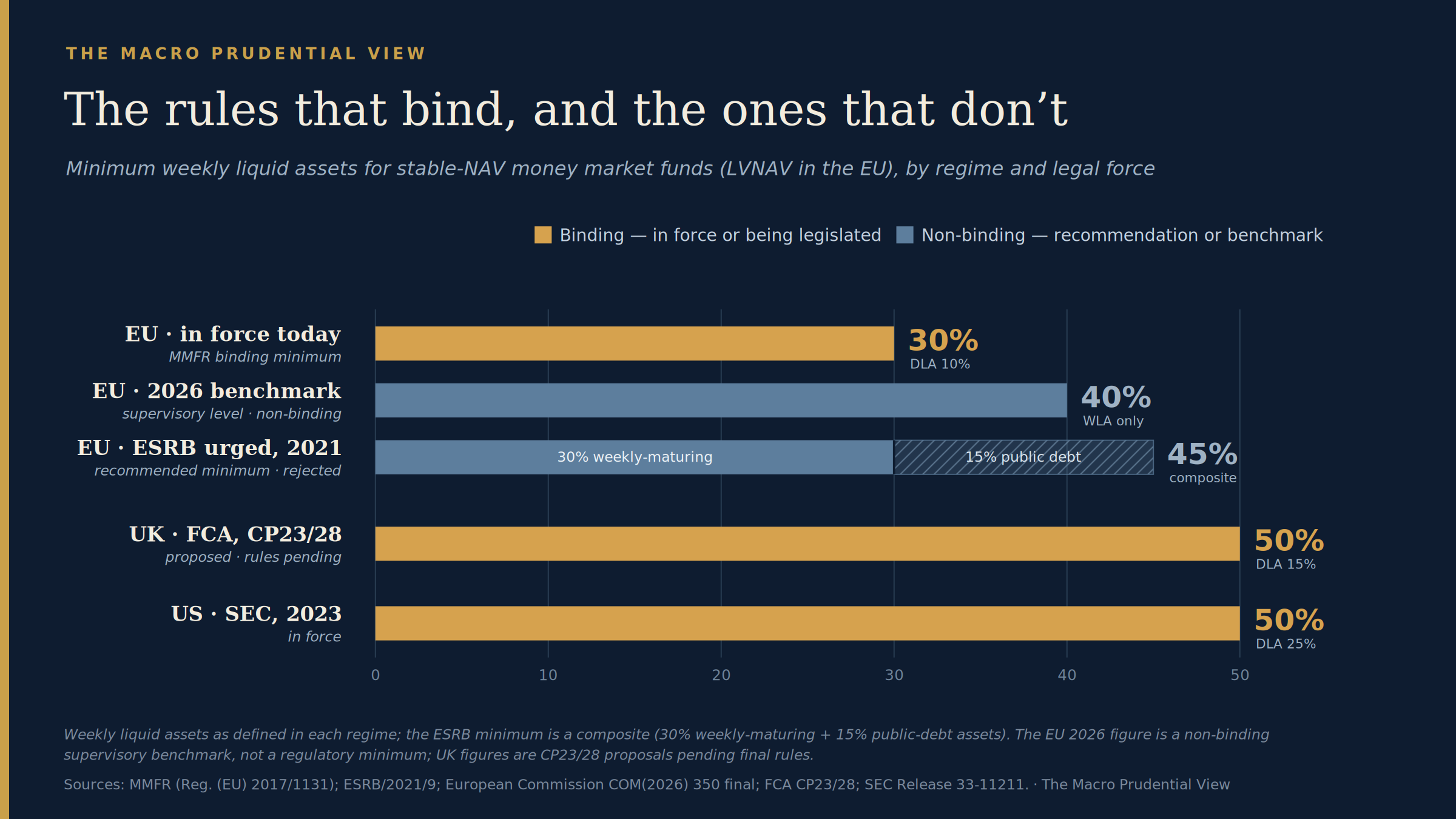

Set the three big regimes beside each other and the EU’s choice looks lonelier than its report admits.

The United States went first and went furthest. In 2014 the SEC required institutional prime and institutional municipal funds — the ones most prone to run — to abandon the stable share price and float their NAV, a change that took effect in 2016. It removed the deposit illusion from the funds where it was most dangerous. Then in 2023, in response to March 2020, it raised weekly liquid assets to 50% and daily to 25% across the board, and cut the automatic link between breaching a liquidity threshold and imposing fees. The American settlement is a floating price for the riskiest funds and high, usable buffers for the rest.

The United Kingdom proposes to keep the stable-value structure and the collar but to raise weekly liquid assets toward 50% and to sever the link between the liquidity threshold and the redemption tools. The FCA’s reasoning is explicit: a 40% requirement would not cover the largest plausible sterling outflows, 50% would, and a dash-for-cash event of the 2020 kind would call for 60 to 70%. The effect is to make the buffer both higher and usable, so that a fund can spend it without that act alone triggering the restrictions that begin the run.

The EU’s answer is a binding floor it left untouched at 30%, a non-binding benchmark of 40%, and one genuine reform: the requirement, delivered through the 2024 overhaul of the AIFMD and UCITS directives rather than the MMFR itself, that funds make at least one liquidity-management tool available. That reform is real, and it is the single ESRB recommendation the Commission was graded as having substantially met. It is also the cheapest of the four. The two costly ones, floating the LVNAV and raising binding liquidity, it declined.

The bars are not strictly like-for-like, and the chart’s footnote says so: the regimes define liquid assets differently, and the ESRB’s 45% is a composite that counts public-debt holdings the others treat separately. The ranking survives the caveat. The EU’s binding floor is the lowest of the group, and the one number it added is the only one in the field that no fund is obliged to meet.

The benchmark that binds no one

Return to the 40% benchmark, because it is the centre of the Commission’s actual policy. Two things about it matter.

The first is that it is not binding. It is a supervisory expectation, not a regulatory minimum, so a fund that sits below it has breached nothing and owes no remediation. In the legal sense the benchmark binds no one, which is the sense the title of this piece intends.

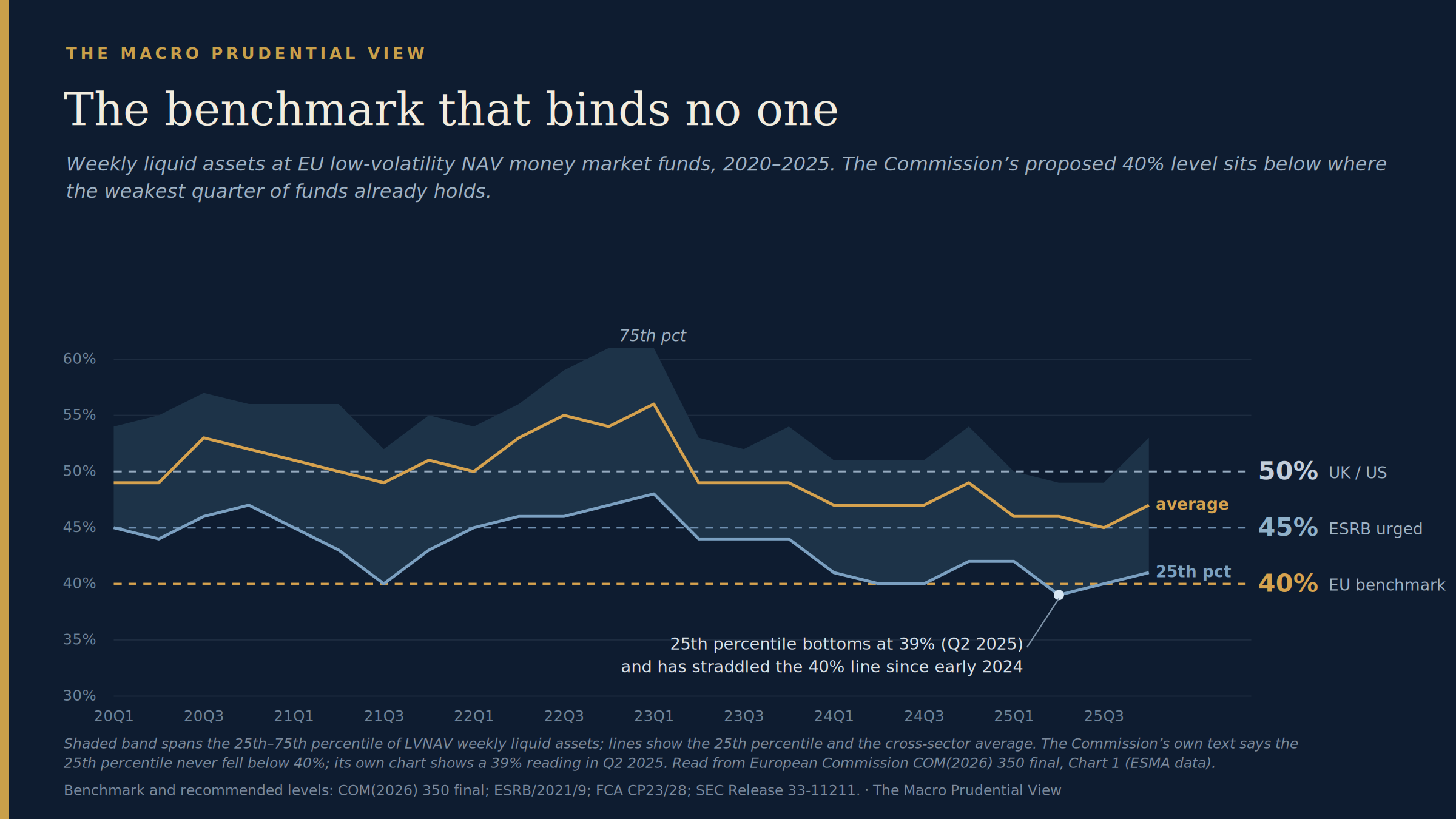

The second is where the level sits. Forty per cent is the level the FCA examined and rejected as too low for the largest sterling outflows; both are pure weekly-liquid-asset figures, so that comparison is like-for-like. It is also at or below where the weakest quarter of EU low-volatility funds has held its liquidity through much of the past five years. The 25th percentile ran through the mid-40s for most of 2020 to 2023, touched 40% as early as the third quarter of 2021, and has sat in a narrow band straddling the 40% line since the start of 2024.

On the Commission’s own chart the 25th percentile reaches 39% in the second quarter of 2025, the only quarter in the five years plotted in which it falls below 40% outright. The report’s text says the figure never fell below 40%; the chart a couple of pages on shows 39%. The discrepancy itself is minor. The 25th percentile sits exactly on the 40% line in four other quarters and has stayed within a point or two of it since the start of 2024, so a binding 40% floor would have bound on part of the weakest quartile across much of the recent period rather than in one isolated quarter. A non-binding version of it, pitched at that level, describes where the sector already operates rather more than it disciplines it.

That is the substance of the objection. The ESRB asked for four things in 2021: make the LVNAV’s price fluctuate, repeal the threshold that manufactures the first-mover advantage, raise binding liquidity, and improve the data on who holds what. Against that list, a non-binding number pitched where the weakest quartile already sits falls well short of a reform, which is the reading the ESRB itself recorded when it graded the response.

What the Commission gets right

The honest objection to all of this is that the Commission is not simply wrong, and the argument is stronger for saying so.

The stress in money funds is not spread evenly across the sector. It concentrates in a tail. And the tail is exactly where the coordination game described earlier actually fires. A run needs a correlated investor base — holders who will reach for the exit on the same signal at the same time. Funds with diversified, operational cash investors do not supply one; funds whose investors are a single strategy, or a single type all exposed to the same shock, do.

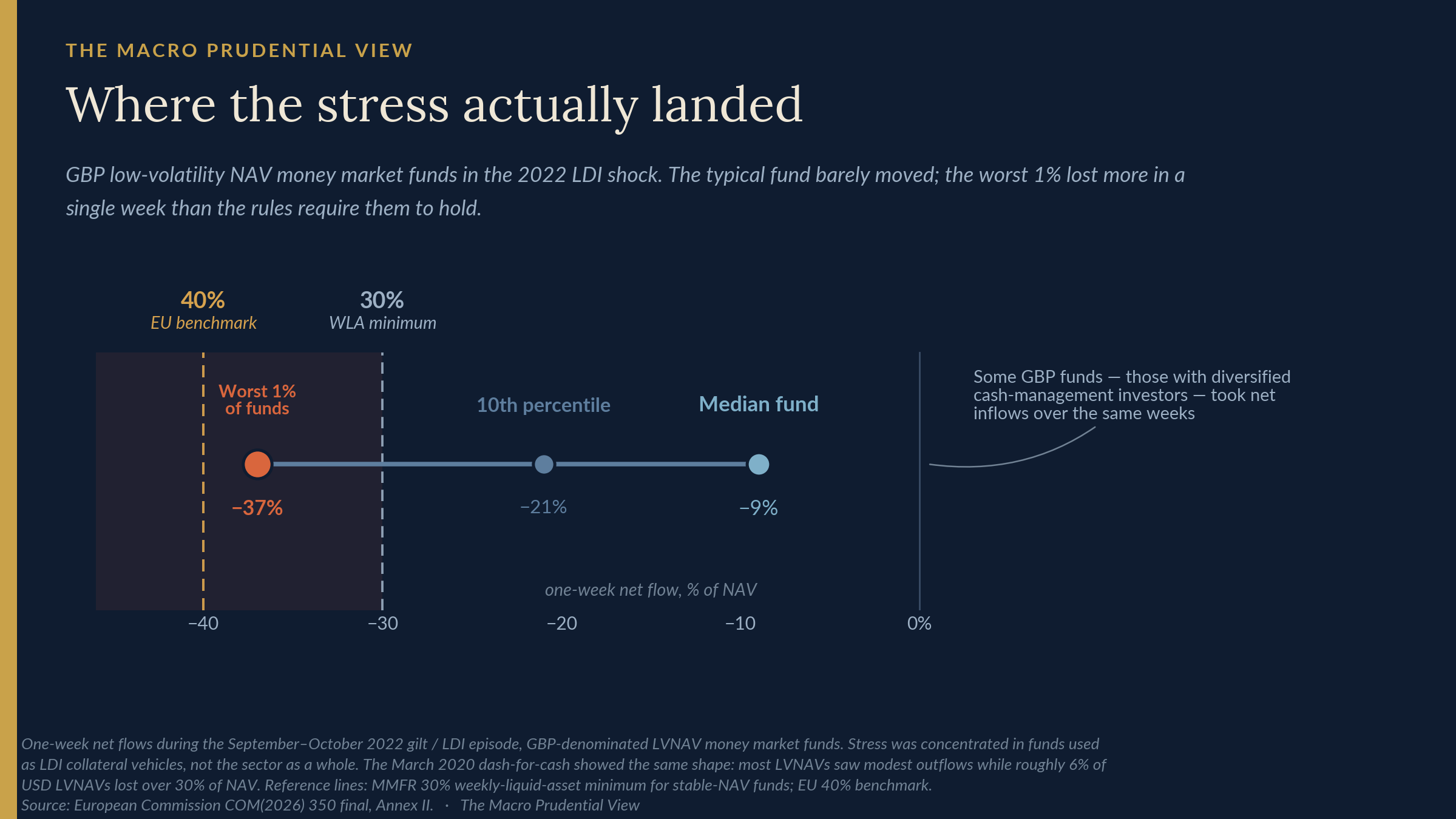

The 2022 gilt crisis showed the pattern. The median sterling LVNAV saw a one-week net outflow of around 9% — heavy for a cash vehicle, but well inside the liquidity the rules require it to hold, and several funds with diversified cash-management investors took money in over the same weeks. The damage was concentrated in a small set of funds used as collateral vehicles by liability-driven investment strategies, whose investor base was about as correlated as an investor base can be. The worst one per cent lost more than a third of their assets in a single week. The weekly liquidity rules are sized to a week of stress, so the comparison is a fair one: a one-week outflow above a third of assets exceeds the 30% the rules require a fund to hold in total, which means that for those funds the buffer would have been fully spent and the fund still short. March 2020 had the same shape — most LVNAVs saw modest outflows while a small fraction of US dollar funds lost over 30% of their assets in a week. The European sector is not a bystander to this. Its own correlated tail is the US-dollar-denominated prime and LVNAV funds concentrated in Ireland and Luxembourg, held by investors who cluster by currency and mandate; that segment carried the 2020 strain on the European side, and it sits inside the EU rules.

A tail problem is a poor match for a sector-wide instrument. Raising the floor on every fund to reach a concentrated minority charges the prudent majority for resilience they already carry, and leaves the concentration that creates the tail untouched. The Commission’s wariness about a blanket increase has a real argument behind it, and the LVNAV does serve a cash-management function for which, in its words, there is “no obvious economic alternative.”

The trouble is that this argument points to a different policy, not to none. If the danger lives in particular funds with particular investor structures, the response is to find and constrain them: concentration and investor-type limits, granular data on who holds what, and buffers a manager can actually draw down under stress without that act alone starting the run. The first two are close to the monitoring and reporting recommendation the ESRB made and the Commission declined; the third is the core of the UK reform. The case against a blunt floor is a case for sharper tools; the Commission adopted neither.

What the resilience rests on

There is a reason the Commission can read the same record as reassuring where the ESRB reads a deferred problem.

In March 2020, and again in the 2022 gilt episode, the constraint that would otherwise have bound was relieved from outside, though by different routes. In 2020 the ECB’s pandemic asset purchases — and, for the EU’s dollar funds, the Federal Reserve’s facilities — stood behind short-term funding directly, at the moment dealer capacity ran out. In 2022 the Bank of England’s gilt intervention worked a step upstream: buying long-dated gilts broke the margin spiral that was forcing liability-driven investors to sell, which stopped the redemptions draining the sterling money funds. Either way a public balance sheet stood in where private capacity had run out, and no EU fund had to gate. That is the fact the Commission leans on. What the record cannot show is how the funds would have fared without those interventions, because the interventions are the reason the counterfactual never ran.

This is the part the Commission half-states when it lists central-bank facilities among the answers. The resilience it observes is real, but it is conditional, and the condition is not priced. An LVNAV offers its investors something close to a bank deposit — a stable value, settlement like cash — at a yield above a deposit. A bank that offers a deposit pays for the public backstop behind it through deposit-insurance premiums, capital requirements, and supervised access to the central bank’s standing facilities. The LVNAV has been able to rely on public support in stress — less formal than deposit insurance, and discretionary rather than guaranteed — while carrying none of those costs. That specific gap, rather than the general truth that all liquidity transformation ends somewhere at the central bank, is what the report leaves unaddressed.

Providing the LVNAV with that implicit backstop may well be the right policy. It is defensible if it is acknowledged, and if the implied support is either priced or contained by the kind of structural limits the ESRB asked for. It is harder to defend when the support is read as evidence of the funds’ own soundness, because it is discretionary: the willingness to deploy it again, at the same scale, may not be there when it is next needed. That is the gap the ESRB chair pointed to in urging the European Parliament’s economic committee, last December, not to wait for the next crisis to settle the framework. The Commission’s report establishes that the funds met their redemptions. It is quieter on what allowed them to.

Paweł Fiedor — The Macro Prudential View

The views expressed are the author’s own and do not necessarily reflect those of any institution with which the author is or has been affiliated.

Sources: European Commission, Report on the functioning of Regulation (EU) 2017/1131 on money market funds, COM(2026) 350 final, 11 May 2026 — https://ec.europa.eu/finance/docs/law/260511-money-market-funds-report_en.pdf; HM Treasury and Financial Conduct Authority, money market fund reform announcement, 14 May 2026 — https://assets.publishing.service.gov.uk/media/6a059b2622977ebc82cb3f5d/The_Government_and_FCA_announce_plans_to_reform_UK_Money_Market_Fund_Regulations..pdf; European Systemic Risk Board, Recommendation ESRB/2021/9 on the reform of money market funds — https://www.esrb.europa.eu/pub/pdf/recommendations/esrb.recommendation220125_on_reform_of_money_market_funds~30936c5629.en.pdf; European Systemic Risk Board, assessment of compliance with Recommendation ESRB/2021/9, February 2025 — https://www.esrb.europa.eu/pub/pdf/recommendations/esrb.compliancereport202502_1~cfa5aff4bd.en.pdf; Regulation (EU) 2017/1131 on money market funds (MMFR) — https://eur-lex.europa.eu/eli/reg/2017/1131/oj/eng; European Commission, impact assessment accompanying the 2013 money market funds proposal — https://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:52013SC0315; Directive (EU) 2024/927 (AIFMD II), amending the AIFMD (2011/61/EU) and the UCITS Directive (2009/65/EC) to require liquidity-management tools — https://eur-lex.europa.eu/eli/dir/2024/927/oj; Financial Conduct Authority, CP23/28, Updating the regime for Money Market Funds — https://www.fca.org.uk/publications/consultation-papers/cp23-28-updating-regime-money-market-funds; U.S. Securities and Exchange Commission, Money Market Fund Reforms, Release No. 33-11211 (2023) — https://www.sec.gov/files/rules/final/2023/33-11211.pdf, and the 2014 institutional prime and municipal floating-NAV reforms — https://www.sec.gov/newsroom/press-releases/2014-143; Financial Stability Board, Holistic Review of the March Market Turmoil, 17 November 2020 — https://www.fsb.org/2020/11/holistic-review-of-the-march-market-turmoil/; Federal Reserve, Money Market Mutual Fund Liquidity Facility and Commercial Paper Funding Facility, March 2020 — https://www.federalreserve.gov/monetarypolicy/mmlf.htm; European Central Bank, Pandemic Emergency Purchase Programme, March 2020 — https://www.ecb.europa.eu/mopo/implement/pepp/html/index.en.html; Bank of England, gilt market operation announcement, 28 September 2022 — https://www.bankofengland.co.uk/news/2022/september/bank-of-england-announces-gilt-market-operation; Bank of England, Financial Stability Report, July 2023 — https://www.bankofengland.co.uk/financial-stability-report/2023/july-2023; European Systemic Risk Board, chair’s remarks to the European Parliament Committee on Economic and Monetary Affairs, December 2025 — https://www.europarl.europa.eu/doceo/document/P-10-2025-004833_EN.html. Data: regime liquidity requirements per the regulatory sources above; the 25th-percentile and cross-sector-average weekly-liquid-asset series read from COM(2026) 350 final, sterling LVNAV redemption data for the 2022 gilt episode — https://ec.europa.eu/finance/docs/law/260511-money-market-funds-report_en.pdf.