The Contagion Web

How shocks actually spread between banks and investment funds, and why single-sector models are no longer sufficient

In a highly interconnected world, one of the most persistent intellectual failings of the credentialed class, particularly within financial regulation, is the tendency to examine complex systems in isolation. We build elaborate, mathematically elegant models to stress-test banks, treating them as if they exist within a vacuum. But as the structural shifts of the past decade have shown us, the center of gravity in global finance has moved.

The conventional wisdom in macroprudential policy has long been to safeguard the banking sector. Yet, if we only look at banks, we suffer from our own form of institutional deafness. We fail to hear the signals emanating from the rapidly expanding non-bank financial intermediation (NBFI) sector, and specifically, investment funds.

What happens when an exogenous shock hits the system? Do banks and investment funds absorb the blow independently, or do their reactions feed off one another, creating a contagion web that amplifies the initial damage?

This was the core question my colleagues and I set out to answer in our recent paper, Shock amplification in an interconnected financial system of banks and investment funds, published in the Journal of Financial Stability.

The Conventional Wisdom: The Danger of the Silo

Historically, central banks and supervisory authorities have relied on single-sector stress testing models. We shock the banks. We see how the banks react. We declare the system safe or vulnerable.

But the reality of modern finance is deeply entangled. Banks and investment funds hold overlapping portfolios. Banks lend to funds; funds hold securities issued by banks. When a crisis strikes, such as the sudden economic halt caused by the COVID-19 outbreak, these entities do not merely absorb the shock in isolation. Their endogenous reactions, their desperate bids for liquidity and survival, collide.

The Contagion Web: Liquidity and Solvency

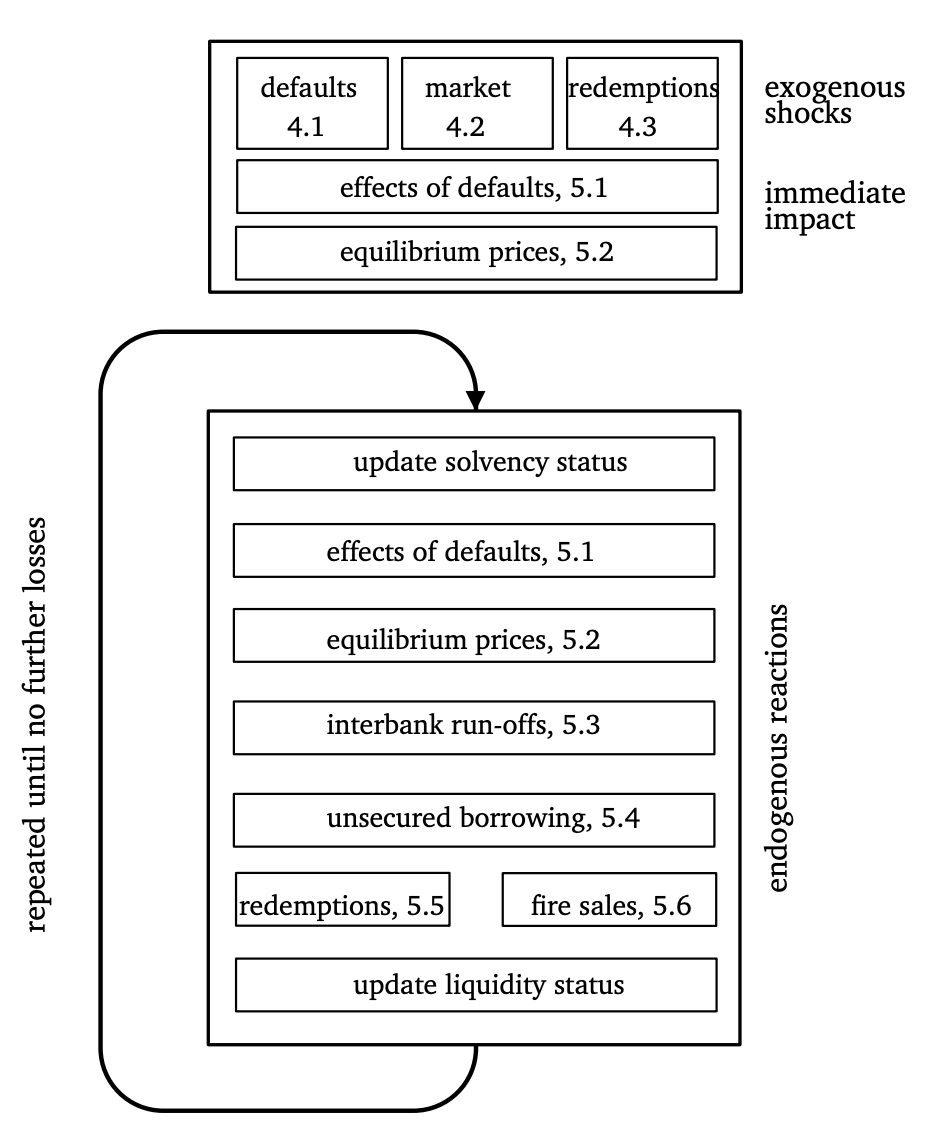

To understand this hidden plumbing, we built a novel model of contagion propagation using a remarkably granular dataset for the euro area. We subjected both sectors to a severe, multi-layered exogenous shock: a default shock, a market shock, and a redemption shock (where investors suddenly pull their capital from funds).

Our model revealed that the contagion mechanism operates through a dual channel of liquidity and solvency risk.

When investment funds face sudden, massive redemptions, they are forced to liquidate assets rapidly to generate cash. This phenomenon, the classic “fire sale,” depresses asset prices across the board. Because banks hold many of those exact same assets, their balance sheets instantly take a hit.

The findings are stark:

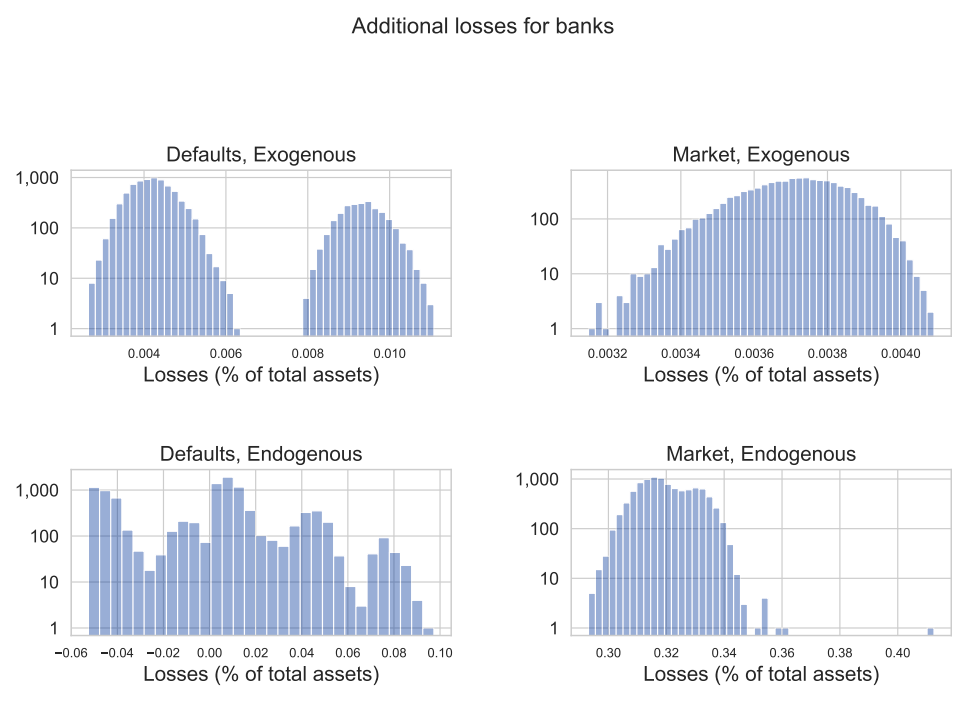

Amplification, not containment: The combined, endogenous reaction of banks and investment funds significantly amplifies losses to the broader financial system compared to single-sector stress testing models.

The Fire Sale Penalty: Adding the investment fund sector to our traditional banking model leads to substantial additional losses driven entirely by these endogenous market losses generated by investment funds’ asset liquidation.

Capital Depletion: This interconnectedness causes a further depletion of banks’ capital ratios by around one full percentage point — a highly material impact during a severe systemic crisis.

The Policy Imperative

For those of us tasked with safeguarding the European financial system, the implications are clear. The days of siloed, single-sector stress testing must end.

If we continue to view the financial system as a collection of independent fortresses rather than a deeply integrated ecosystem, our models will remain elegant but dangerously incomplete. We must expand the scope of financial stability analysis to capture this institution-level contagion across different sectors.

Understanding the world requires us to map the connections others ignore. As the shadow banking sector continues to grow, our regulatory frameworks must evolve from monitoring isolated entities to managing the contagion web itself.