The Liquidity Illusion

From the AI ETF boom to the hidden mechanics of market plumbing — why all exchange-traded funds are not created equal.

The AI ETF Boom and the Plumbing Beneath It

We are witnessing a historic reallocation of capital, and it is being executed through Exchange-Traded Funds (ETFs).

To understand the sheer scale of what is happening, you only need to look at the Nasdaq-100. Investors flock to the Invesco QQQ Trust under the assumption of diversified tech exposure. In reality, the fund has become incredibly top-heavy. As of early 2026, nearly 50% of the entire ETF’s weight is concentrated in just nine companies, almost all of them directly tethered to the artificial intelligence boom.

This concentration isn’t an accident; it is a reflection of a market that has violently bifurcated. The companies building the physical infrastructure for this new era have completely decoupled from the rest of the economy.

When we index the performance of these assets back to the end of 2020, the divergence is staggering. The VanEck Semiconductor ETF (SMH) has left both broad tech (QQQ) and small-cap equities (IWM) in the dust.

But perhaps the most telling metric isn’t past performance, it is current investor sentiment. Looking at year-to-date fund flows for 2026, we can see exactly how the market is placing its bets. Institutional and retail money alike are abandoning broad market exposure. QQQ has bled $10.7 billion in outflows, and small-caps have lost $4 billion. Meanwhile, capital continues to pour into the semiconductor space.

Investors are using ETFs as precision scalpels to slice into highly specific macro trends. They treat these vehicles as perfectly liquid, perfectly efficient conduits for their capital.

But this brings us to a critical, heavily overlooked problem: an ETF is not a magic wand that uniformly blesses its underlying assets with liquidity. It is a conduit. And like any conduit, what it transmits depends entirely on what it is connected to.

The Liquidity Illusion

There is a comforting, yet deeply flawed, tendency within the credentialed class to treat financial innovations as monoliths. When a new vehicle proves successful, we assign it a static set of characteristics and assume it will behave identically across all environments.

Nowhere is this intellectual complacency more evident than in our understanding of Exchange-Traded Funds (ETFs).

Over the past decade, ETFs have been heralded as the great democratizers of finance, granting investors immediate, continuous access to everything from highly liquid equities to notoriously opaque corporate bonds. The conventional wisdom dictates that ETFs inject liquidity into the system, acting as a stabilizing buffer. But this view suffers from a critical blind spot: it ignores the microstructure of the underlying markets.

An ETF is not a magic wand that uniformly blesses its underlying assets with liquidity. It is a conduit. And like any conduit, what it transmits depends entirely on what it is connected to.

This was the premise of the research I conducted with Petros Katsoulis at the Central Bank of Ireland, detailed in our paper, Information and liquidity linkages in ETFs and underlying markets. We sought to answer a specific question: Does the systemic footprint of an ETF change depending on the asset class it tracks?

The answer is a resounding yes.

The Arbitrage Engine and Market Accessibility

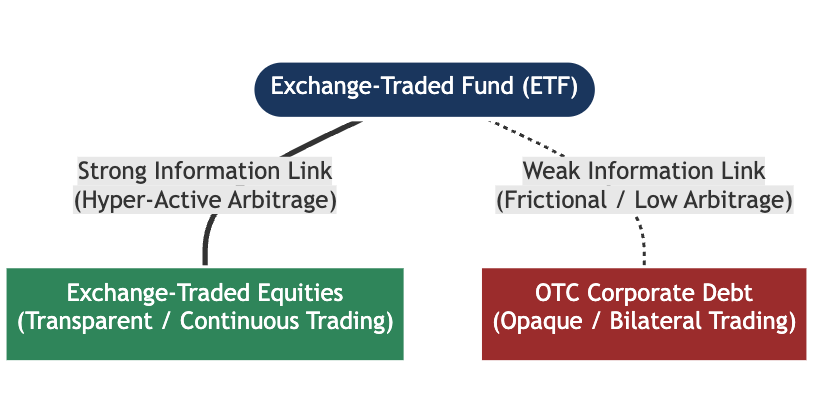

To understand the differential impact of ETFs, we must look at the mechanics of arbitrage. The price of an ETF share and the value of its underlying securities are kept in equilibrium by arbitrageurs who exploit price differences the moment they arise. This activity creates an “information link.”

However, this link requires accessibility.

When an ETF tracks equities, it tracks assets that are traded continuously on transparent, highly accessible exchanges. Arbitrageurs can move swiftly between the ETF and the underlying stocks. This hyper-accessibility forges a strong information link.

Corporate debt, by contrast, is a different beast. It is primarily traded over-the-counter (OTC) in private, bilateral transactions characterized by high search and transaction costs. It is fundamentally hard to access. Consequently, arbitrageurs are far less active, resulting in a weak information link between the ETF and the underlying bonds.

The Volatility Paradox

This divergence in market accessibility leads to starkly different systemic outcomes—some of which directly contradict the prevailing regulatory assumptions. Our analysis revealed three distinct phenomena:

1. The Contagion of Illiquidity: When an ETF experiences a liquidity shock (a sudden spike in trading costs), it propagates that shock directly to underlying equities. Because the information link is so strong, a disruption in the ETF instantly impairs the underlying stock. However, this illiquidity contagion does not spread to corporate debt securities. The weak information link acts as a firewall.

2. Asymmetric Returns: Demand shocks in the ETF market—represented by sudden inflows or outflows—affect the daily returns of underlying equities to a massive degree. Yet, these same ETF flows barely register on the daily returns of corporate bonds.

3. The Volatility Divergence: This is perhaps the most counterintuitive finding. What happens as ETF ownership of an asset class grows?

In the equity market, higher ETF ownership actually increases the volatility of the underlying stocks. The ease of access supercharges arbitrage activity, making equity prices hyper-sensitive to ETF demand.

In the corporate debt market, higher ETF ownership decreases the volatility of the underlying bonds. Because the underlying bonds are hard to trade, investors simply migrate to the ETF to satisfy their liquidity needs, leaving the underlying OTC market quiet.

The Policy Imperative

The illusion of uniform liquidity is a dangerous premise for both investors and financial regulation.

When we watch billions of dollars flee broad market tech (QQQ) and violently pivot into concentrated semiconductor bets (SMH), we aren’t just looking at a shift in market sentiment. We are watching a real-time stress test of the underlying market plumbing.

When regulators attempt to gauge the systemic risk posed by the multi-trillion-dollar ETF industry, they cannot rely on broad generalizations. The hyper-accessible equity markets underlying SMH and QQQ mean that these massive, sudden fund flows will inevitably breed arbitrage-driven volatility and potential illiquidity contagion in the underlying stocks.

However, if those same billions were flowing into high-yield corporate debt ETFs, the systemic footprint would be fundamentally different. In the corporate bond space, the risk is not contagion, but rather the hollowing out of the underlying market as liquidity migrates entirely to the ETF layer.

If we wish to build resilient macroprudential frameworks—and if investors want to truly understand the structural risks sitting inside their portfolios—we must stop looking at financial products in a vacuum. We must be willing to do the hard work of examining the plumbing.