The Wrong Margin

Why macroprudential policy keeps missing the real fault line

PIK is not an anomaly

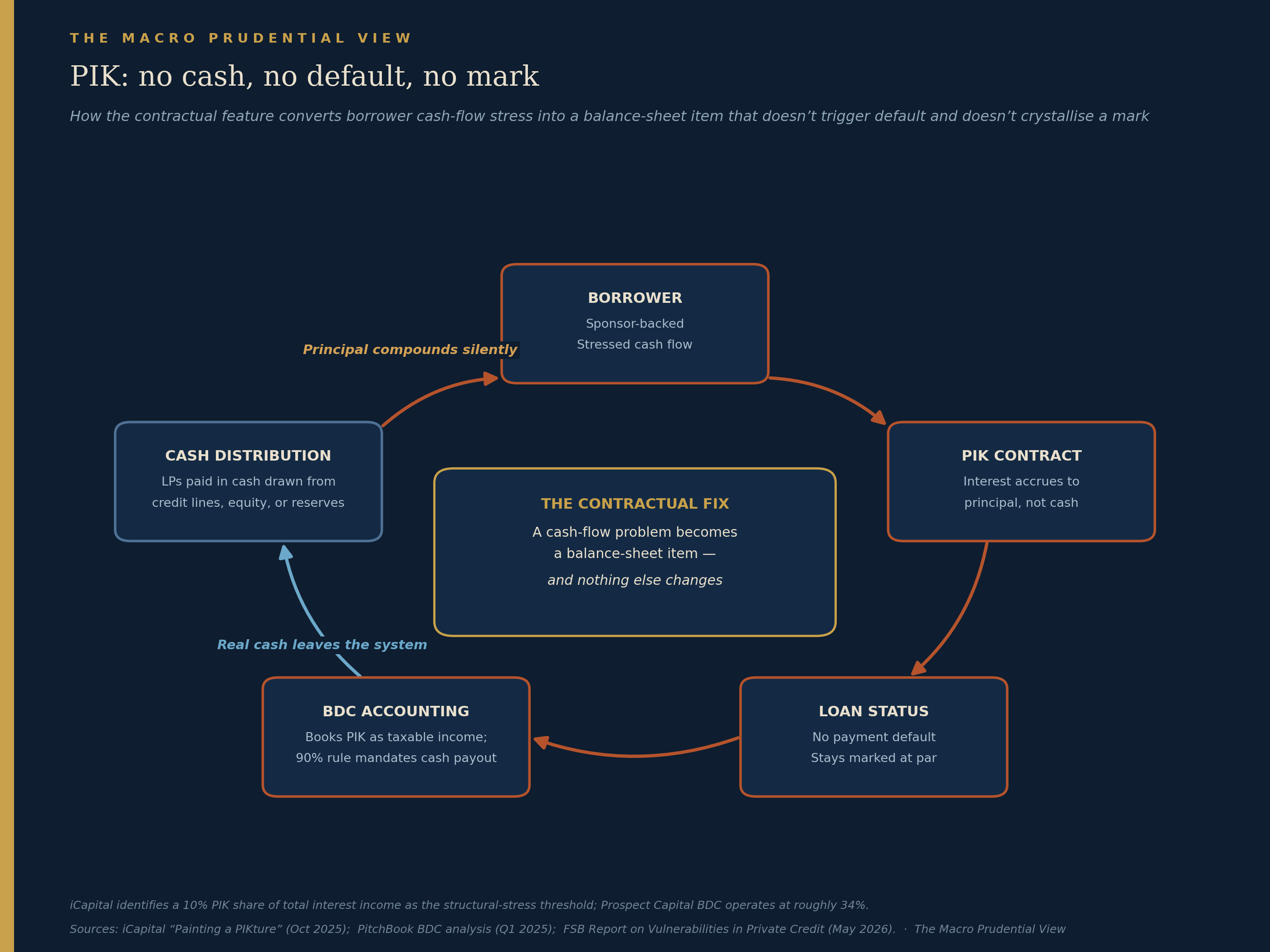

Imagine a sponsor-backed mid-market borrower. The original 2022 senior secured term loan was clean: cash interest paid quarterly, fixed and floating spreads, standard maintenance covenants. By late 2024 the borrower’s cash flow has deteriorated. Rather than mark the loan, restructure it, or trigger a covenant breach, the lender and the sponsor agree to convert a portion of the interest from cash-pay to PIK — payment-in-kind, where the interest doesn’t actually leave the borrower as cash but accrues to the principal balance instead. The headline default rate is unaffected. The loan continues to be marked at or near par. The BDC holding the loan reports interest income, including the PIK component, in its quarterly results. The cash distribution to LPs goes out on schedule, funded partly by other loans and partly, increasingly, by new equity raises or draws on the fund’s credit lines.

No one has crystallised a loss. The borrower’s principal is growing. The reported numbers look stable, for now. Because valuations in private credit are GP-determined and infrequently tested against arms-length markets, the “for now” can persist much longer than common sense expects.

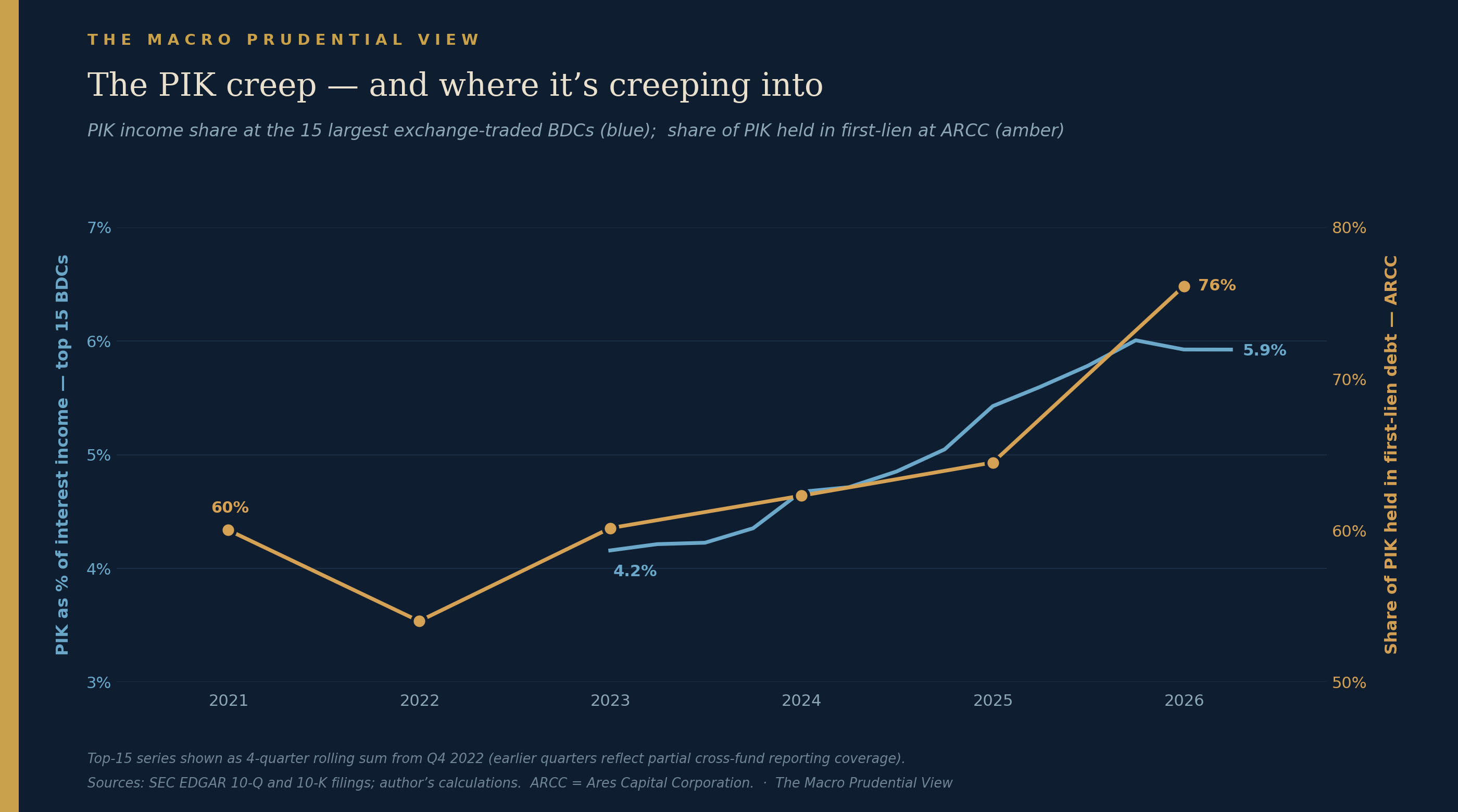

This is not a small phenomenon. Based on my own aggregation of the top fifteen exchange-traded BDCs’ EDGAR filings, PIK income has risen from roughly 4% of total interest income at end-2022 to about 6% by Q1 2026 on a four-quarter rolling basis. The more striking shift is where PIK now sits: at Ares Capital Corporation, the largest exchange-traded BDC and one of the most conservatively-run, the first-lien share of PIK-paying investments (measured by fair value) has risen from 60% in 2021 to 76% by year-end 2025. PIK was historically a feature of distressed mezzanine and second-lien paper. It now sits in senior secured paper at the most benchmark-quality BDC in the market.

The FSB’s Report on Vulnerabilities in Private Credit, published in May 2026 after a year-long investigation, made the data limitations explicit. The report states that private credit “remains untested in a prolonged economic downturn” and that authorities face “significant data challenges” in monitoring the bank-fund interconnection. It also flagged “the rising use of payment-in-kind arrangements” as one indicator of deteriorating credit conditions. After a year of work involving every major macroprudential authority in the developed world, the official sector is still working around structural data blind spots — unable to map, with anything approaching precision, how much PIK is outstanding, who holds it, or what these valuations would survive in a real downturn.

This is not a small market. The FSB estimates the global private credit asset class at $1.5–2 trillion, with direct bank credit lines to private credit funds running in the hundreds of billions. The interconnection is large enough that the data gaps matter.

I want to be careful about what kind of claim I am making here. PIK is not a fraud. It is not even, on any individual loan, a problem. PIK toggles have a legitimate role in financing structures where cash flows are lumpy or where a sponsor needs flexibility through a specific investment phase. What is interesting is not any single PIK toggle. What is interesting is the equilibrium — the fact that every participant in the capital structure has private incentives pointing the same way.

That equilibrium is the subject of this essay. Private credit’s PIK creep is the contemporary illustration, but the underlying pattern is much older. It is, I will argue, the central problem in financial stability — and the one that macroprudential policy, for reasons that have to do with how the toolkit was designed rather than with anyone’s incompetence, is least well-equipped to address.

Why the equilibrium holds

Walk the stack of incentives, one participant at a time.

The borrower wants survival. Cash interest converted to PIK is, for a stressed borrower, the difference between a default and a non-default. Even if the principal is compounding at 12% — and that is roughly where current PIK rates sit — the alternative is worse. The borrower is not making this trade strategically; it is making it under duress.

The sponsor’s interest aligns. Injecting fresh equity into a stressed portfolio company crystallises a down-round, recalibrates the fund’s mark on the position, and hits the sponsor’s IRR. A PIK arrangement protects all three. It is the sponsor’s own version of smoothing, and the GP-LP interests align on this — neither party benefits from a marked-down NAV at this stage of the fund’s life.

The General Partner of the credit fund holds the loan at fair value, which is its own determination, audited but not market-priced. As long as the loan continues to pay interest (whether in cash or in kind) and as long as no covenant trips, the GP can defend a near-par mark. The GP earns management fees on assets under management and performance fees on returns above a hurdle. Both are smoother if losses don’t crystallise. Beyond the direct fee economics, the GP is in a competitive market for institutional capital where marked-down NAVs become a fundraising problem within months. The incentive to extend rather than mark is structural.

The Limited Partner — pension fund, insurance company, sovereign wealth fund — receives a cash distribution on the fund’s reporting schedule, and the distribution does not distinguish between cash interest received from healthy borrowers and PIK income accrued from stressed ones. The LP’s allocators are evaluated on relative performance against a benchmark, and the benchmark is constructed from the same fund universe with the same valuation conventions. There is no LP that has a strong unilateral incentive to demand a fair-value crystallisation.

For the BDC structure specifically, the regulatory framework adds an additional twist. US Regulated Investment Company (RIC) tax status requires the BDC to distribute at least 90% of its taxable income annually to maintain that status. That taxable income includes PIK. The BDC therefore must pay cash dividends on income it did not receive in cash. The cash for those dividends comes from other loans, from credit-line draws, from new equity raises, and — as the PIK share grows — from increasingly complex funding manoeuvres to sustain the dividend policy. iCapital argues that there is natural pressure on BDCs to keep PIK income below roughly 10% of total interest income, because above that level cash-distribution stress becomes structural. Prospect Capital, one of the more PIK-heavy listed BDCs, operates at roughly one-third of net investment income based on its filings — well past the threshold.

The mechanical consequence deserves to be stated plainly. When a BDC raises new equity, draws on a subscription line, or rolls a credit facility to fund a cash distribution against PIK income, real cash is leaving the system. The fund is burning actual liquidity — investor capital, bank lending capacity, dividend reserves — to sustain the appearance of a smooth, non-defaulting portfolio. The equilibrium is not a free lunch. It is a slow drawdown of liquid resources to defer the recognition of a credit problem, financed by the rotation of new capital in to pay out old.

The bank — and there is usually a bank somewhere in the structure — earns commitment fees on the subscription line or NAV-backed facility extended to the fund (typically collateralised by fund NAV and short-dated), and avoids any direct credit exposure to the underlying borrower. The bank’s balance sheet looks safer than it would have if the bank had made the loan directly. The economic exposure is largely the same, but it sits in a structure that doesn’t show up on the bank’s lending book or in its regulatory disclosures.

The point of walking through the stack is that nothing in it is wrong on its own terms. Every participant is responding rationally to its own incentive structure. The contractual fix — converting a cash-flow problem into a balance-sheet item — works at the level of each individual contract. What fails is the aggregation. The system as a whole is taking on credit risk that is not visible to any single participant, including the prudential supervisor.

This is often called “extend and pretend,” and it is recognised, in retrospect, as a feature of essentially every credit cycle for at least four decades.

The same machine, different fuel

In my reading of the post-1980 history of financial regulation, one of the most consistent patterns is not crisis followed by reform. It is innovation followed by smoothing, where smoothing means the introduction of some contractual or structural innovation that converts a cash-flow or credit problem into something that doesn’t trigger immediate recognition. Every cycle generates a new technology for doing this.

US savings and loans in the 1980s used regulatory accounting principles — RAP, distinct from GAAP — to defer recognition of losses on residential mortgages whose market value had collapsed when interest rates spiked. The RAP allowed S&Ls to amortise losses over the remaining life of the loan rather than mark them at issuance. By the time the system was forced to recognise the underlying insolvency, the bill was several hundred billion dollars. In each case I describe in this section, the binding choice was not whether losses existed, but when — and in which set of accounts — they would be recognised.

Mortgage securitisation in the 1990s and 2000s separated the originator of a loan from the bearer of its credit risk. The originator earned a fee on issuance and passed the cash flows to investors via structured vehicles whose ratings depended on internal models that the rating agencies themselves did not fully understand. The CDO bid in 2005–2007 produced a market in which the demand for AAA-rated mortgage paper exceeded the underlying supply of AAA-quality mortgages, with the difference made up by financial engineering. The losses crystallised in 2008.

Leveraged loans and CLOs in the 2010s migrated the same originate-and-distribute model into the corporate credit space, with two refinements. First, covenant-lite documentation removed most of the maintenance triggers that historically forced workouts before losses became catastrophic. Second, the CLO buyer base — primarily insurance companies and bank trading desks searching for AAA-rated paper — provided structurally inelastic demand at the top of the capital structure. By the early 2020s, over 85–90% of new leveraged loans were covenant-lite, and the global CLO market had grown to around $1–1.4 trillion.

Private credit and PIK in the 2020s are, in my read, the next iteration — the same equilibrium I described earlier, refracted through different financial-engineering vocabulary. The contractual innovation is the PIK arrangement; the structural innovation is the move from public bond markets to private fund vehicles where valuations are GP-determined and disclosure is limited to LPs. Each generation looks technical and specific enough that the previous generation’s lessons “don’t apply.” Each generation is the same equilibrium — converting cash-flow stress into something that doesn’t have to be recognised today, because everyone in the stack is happier that way.

This is not the only path innovation can take. Plain-vanilla interest-rate swaps, simple pass-through securitisations, and CCP-cleared derivatives have all become standard infrastructure without obvious crisis episodes. The pattern I am identifying applies to the subset of innovation that combines leverage, opacity, and contractual smoothing of credit stress — which is, on the evidence of the last forty years, the consequential subset.

What is common across the consequential cases is not a failure of regulation in the narrow sense. Capital requirements existed in 1985, in 2005, in 2015, in 2025. They have generally gotten tighter over time, not looser. What is common is that the regulation operates on quantities — how much capital, how much liquidity, how concentrated the exposure — while the innovation operates on incentives — who recognises losses when, who captures the upside, who bears the downside if the bet doesn’t work. The architecture of post-2008 macroprudential policy was built to manage quantities. It works for that. It does not, by its own design, address the contractual and structural margins where the next equilibrium is being built.

This is the central argument of this essay. The rest is detail.

What macroprudential policy actually does

Before going further it is worth being precise about what the post-2008 macroprudential toolkit consists of, because the argument is not that macroprudential policy is bad — it is that the toolkit’s design defines its perimeter, and that perimeter is largely orthogonal to the incentive structures that drive the kind of equilibrium described above.

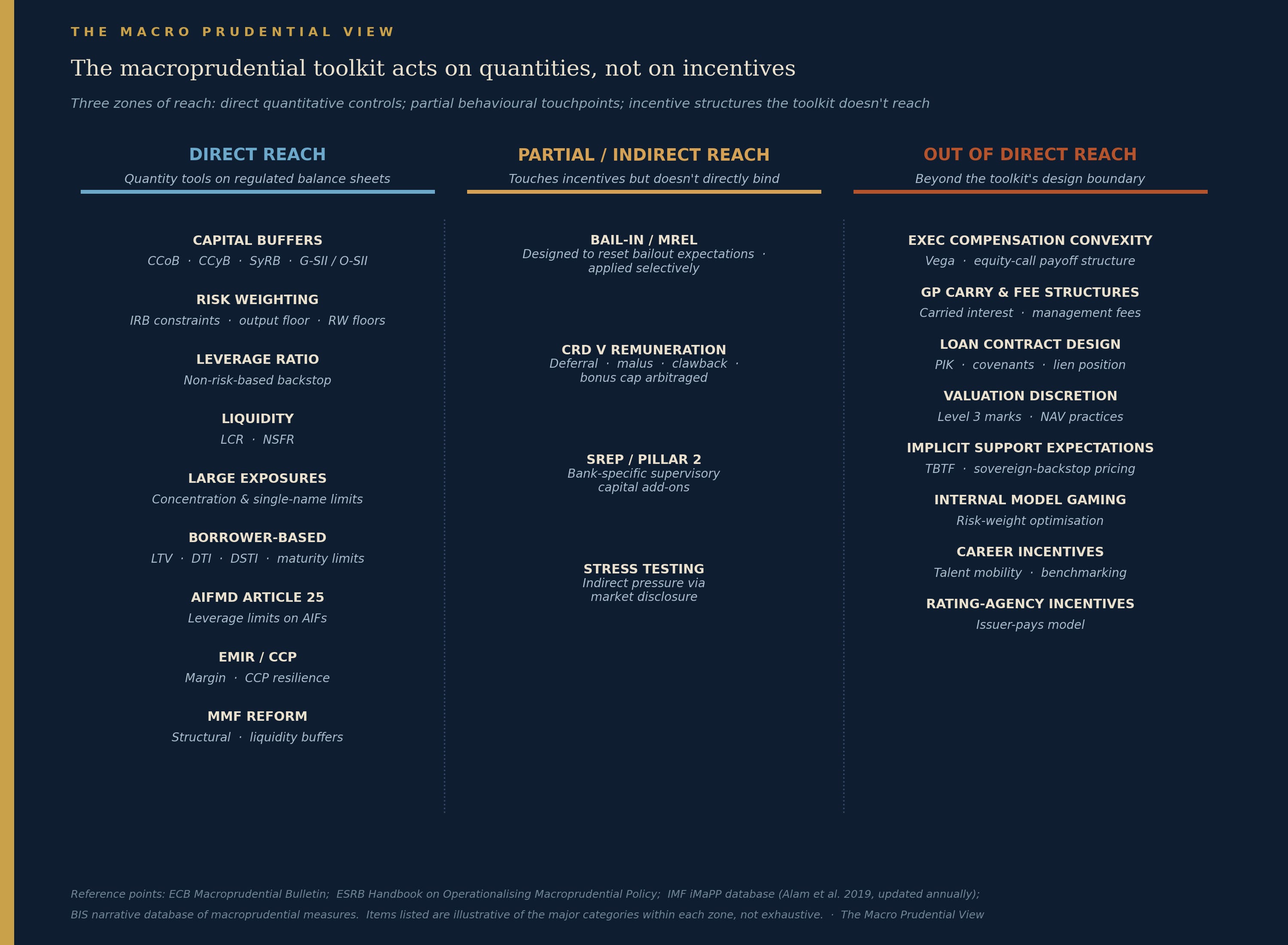

The bank-side toolkit, organised by category, has six main families. Capital tools — the Capital Conservation Buffer, the Countercyclical Capital Buffer, the Systemic Risk Buffer, the G-SII and O-SII buffers — together raise the equity-to-assets ratio of regulated banks above the Basel III minimum, in some jurisdictions substantially. Risk-weight constraints — output floors, IRB restrictions, sectoral risk-weight floors — limit the extent to which banks can use internal models to reduce the denominator of their capital ratio. The leverage ratio provides a non-risk-based backstop against the gaming of risk weights, and in Europe has been binding for a subset of large institutions since CRR2 took effect in 2018. Liquidity tools — the Liquidity Coverage Ratio and the Net Stable Funding Ratio — require banks to hold sufficient high-quality liquid assets to survive a 30-day stress scenario and to maintain a stable funding profile over a one-year horizon. Large exposure limits and concentration rules cap the credit risk a bank can take to a single counterparty or sector. Borrower-based measures — LTV, DTI, DSTI, maturity limits on mortgages — operate on the demand side of the lending market.

Beyond banks, the macroprudential perimeter has expanded into non-bank financial intermediation, with three main vectors. AIFMD Article 25 gives national authorities the power to impose leverage limits on alternative investment funds. EMIR margin and CCP resilience requirements address counterparty risk in derivatives markets. The MMF reform agenda restructured the prudential treatment of money market funds after the 2008 and 2020 runs.

Every item in this toolkit operates on a quantity: amount of capital, ratio of capital to assets, share of liquid assets in the balance sheet, size of exposure to a single counterparty, leverage of a fund vehicle. None of them operates directly on a contract — on how interest is structured, how covenants are written, how valuations are determined, how compensation is linked to outcomes. (Supervisors do issue expectations on underwriting standards through guidelines and SREP letters, but these are not primary macroprudential tools, and they operate at the institution level rather than at the market level.) Bail-in and MREL come closest to touching incentives, in that they were explicitly designed to reset bondholder expectations about loss-absorption capacity, and CRD V’s remuneration rules — deferral, malus, clawback — reach into compensation structure. But as we will see, the latter has been substantially arbitraged and the former applied unevenly. SREP capital add-ons under Pillar 2 give supervisors institution-specific discretion, but the discretion is exercised through the same quantity-based instruments as the rest of the toolkit.

There is a defensible objection at this point: that capital and MREL do reach incentives indirectly, through the cost-of-capital channel. Higher required capital makes risk-taking more expensive at the margin; higher MREL makes bail-in-eligible debt price the risk of loss; rising buffers compound through retained earnings into discount rates. This is true. But what the price channel adjusts is the price of risk-taking. It does not adjust the contractual terms through which risk is masked. A bank facing higher capital costs may demand a higher spread on a leveraged loan; it does not, through the price channel, get an instrument to constrain whether that loan can convert from cash-pay to PIK once made. The price channel changes the marginal economics of activities the framework can see. It does not bring activities the framework cannot see into the framework.

This is not a critique of the toolkit. The macroprudential framework was designed to address the failures most clearly diagnosed in the aftermath of 2008 — banks were undercapitalised, illiquid, and concentrated. The post-2008 reforms made banks better capitalised, more liquid, and less concentrated. The empirical literature on the effectiveness of macroprudential tools — Galati and Moessner’s BIS survey, the IMF’s iMaPP studies, the ECB’s Macroprudential Bulletin series — generally finds that the tools work for what they were designed to do.

The toolkit has also expanded. AIFMD Article 25 leverage limits, MMF structural reform, CRD V remuneration rules, and SSM Pillar 2 discretion all reach further than the framework did in 2010. Yet these expansions remain largely quantity-based, or — in the case of remuneration — have been substantially arbitraged, as the bonus-cap evidence later in this piece will show.

The argument is structural, not evaluative. The toolkit’s design constrains its reach. The kind of equilibrium described above — where PIK creep happens because every participant has private incentives pointing the same way — operates at margins the toolkit does not directly touch. The regulatory architecture has the tools to constrain how much bank capital sits behind a leveraged loan, but no comparable tools to constrain how that loan is contractually structured once made.

The deeper question, and the subject of the rest of this essay, is whether macroprudential authorities can — or should — develop tools that reach the contractual and incentive margins directly. The right place to start is where the post-2008 reform agenda itself started: the capital framework.

Capital alone hasn’t worked, but not for the reason most people think

After 2008, the regulatory response was dominated by capital. Basel III roughly tripled the minimum CET1 requirement; CRD IV and CRR layered the Capital Conservation Buffer, Countercyclical Capital Buffer, Systemic Risk Buffer, and G-SII/O-SII surcharges on top. The trajectory has been almost monotonically upward: average CET1 ratios for large international banks have risen from approximately 7% pre-crisis to comfortably above 14% by 2024. By any reasonable measure, large internationally-active banks are better capitalised today than at any point since the 1980s.

This was the right starting point. The 2008 crisis revealed that major banks were running with equity ratios of 2–3% of unweighted assets, supporting maturity transformation and credit creation that depended on continuous wholesale funding access. When that funding froze, the banks did not have the equity buffer to absorb mark-to-market losses while remaining solvent. The capital response is, in retrospect, the clearest success of the post-2008 reform agenda.

But it has limits. Two of them deserve attention.

The first limit is the one Haldane diagnosed in his 2012 “Dog and the Frisbee” speech. Regulatory complexity, beyond a certain point, becomes a tool of gaming rather than a constraint on it. The more granular the risk-weighting framework, the more parameters available for a sophisticated bank to optimise against. The internal ratings-based (IRB) approach was, in its design, supposed to align capital requirements more tightly with actual risk. In implementation, it produced significant divergence between banks holding similar portfolios — divergence that the EBA’s IRB benchmarking exercises have documented year after year. The output floor introduced under Basel IV is the multilateral response, but a partial one: it limits how far banks can use internal models to reduce risk weights, without addressing the underlying complexity that makes the gaming possible. Tarullo, in his April 2017 “Departing Thoughts,” made adjacent points from the regulatory side: the framework had become too complex for supervisors themselves to verify in real time.

The second limit is more fundamental and gets less attention. Capital regulation operates on the denominator of the loss-absorbing layer. Increase capital requirements, and equity holders bear more of any given loss. Useful — but it does not change who decides whether to take the loss-generating risk in the first place. That decision is made by management, on the basis of an incentive structure that allocates the upside of risk-taking to equity (via options, restricted shares, performance metrics that scale with ROE) and the downside to depositors, bondholders, and ultimately the sovereign. Capital regulation does not touch that asymmetry directly. It just changes the size of the buffer between management’s incentive and the taxpayer.

Admati and Hellwig pushed hard on the level of capital in The Bankers’ New Clothes (2024 edition) — arguing that bank capital should be substantially higher than current Basel standards, and that the conventional industry case against higher capital is built on flawed arguments about funding costs. Their analysis is rigorous, and the response from the official sector and from academic critics has, in my read, mostly conceded the basic point while disagreeing on the operational margin. Their argument is about level. The argument I make next — the Bebchuk-Spamann argument — is about structure.

The same logic, refracted, applies to private credit. The capital that sits behind a bank’s subscription line to a private credit fund is regulatory-light because the line is structurally senior, collateralised by fund NAV, and short-duration. That is a quantity argument that holds up under standard regulatory analysis. But the bank’s decision to extend the line, and the fund’s decision to use it for cash dividends to LPs rather than for borrower workout, is driven by incentive structures that no quantity tool reaches.

The incentive mechanism: a call option on bank assets

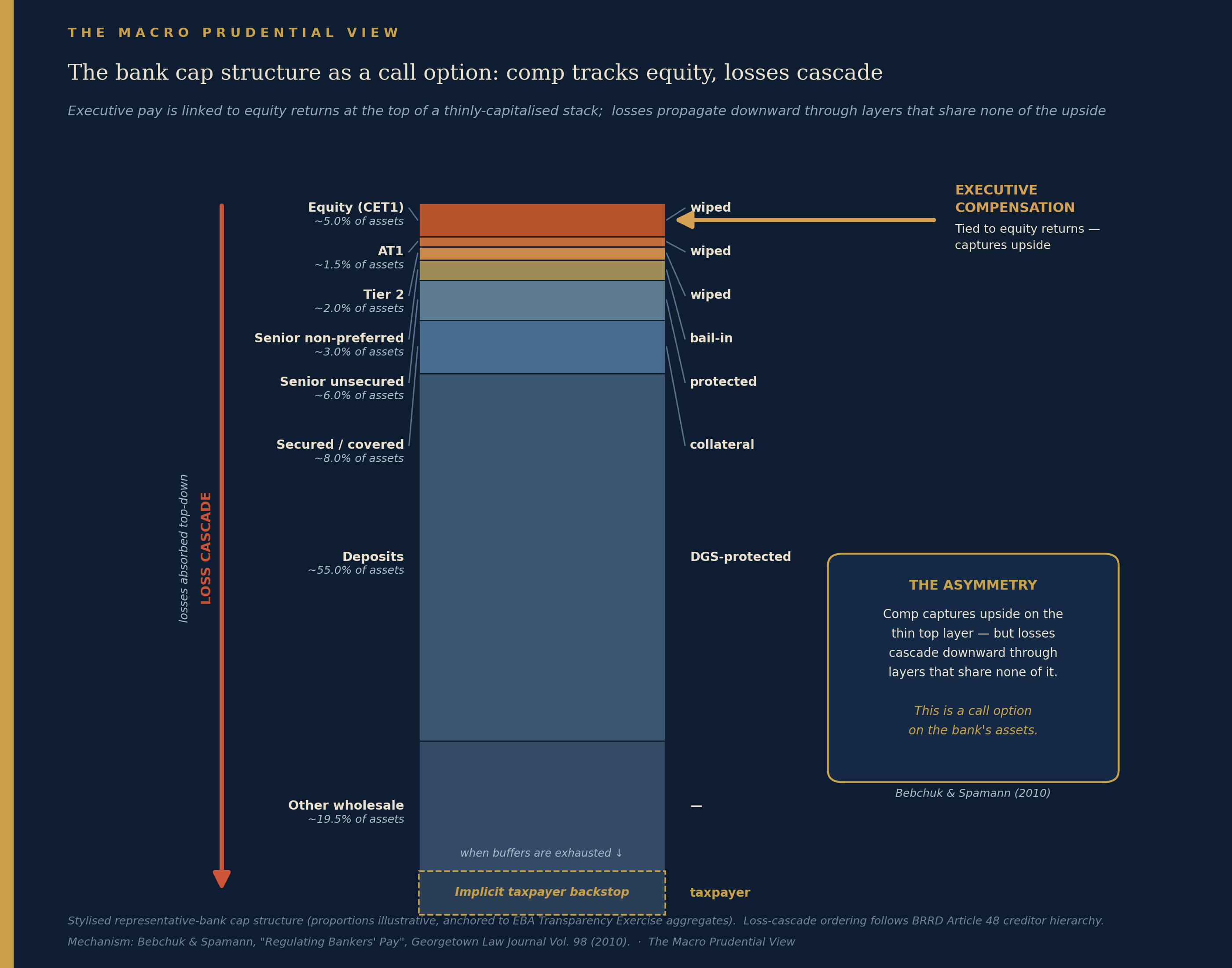

The cleanest formal statement of the bank-comp problem is Bebchuk and Spamann’s 2010 Georgetown Law Journal article, “Regulating Bankers’ Pay.” Their argument has a single moving part. A bank’s capital structure is overwhelmingly debt-financed: equity is typically 5–7% of assets, with deposits (50–60% of liabilities) and various forms of senior and subordinated debt filling the rest. Executive compensation is heavily linked to equity returns — through restricted stock, performance share units, ROE-based bonuses. The structure of the executive’s claim, then, looks like a long call option on the bank’s assets: substantial upside if asset values rise (equity is the residual claimant), capped downside at zero (because the executive does not personally fund losses below their own equity holdings, which are typically a fraction of one year’s compensation).

The mechanics are straightforward. With a thin equity layer at the top of a heavily-levered capital stack, small changes in asset values translate into large changes in equity value. A 1% increase in asset values, on a balance sheet where equity is 5% of assets, is a 20% increase in equity. Conversely, a 1% decline in asset values wipes out 20% of equity — but the executive’s exposure is asymmetric, because their pay is linked to equity returns when those returns are positive (vesting of options, performance bonuses paid in good years), while the executive does not personally absorb negative returns beyond their own holdings. The result is an executive payoff profile that is convex in asset volatility: the executive is, in option theory terms, long vega.

This is what the chart above shows. Compensation tracks equity at the top of the stack; losses cascade downward through layers that share none of the upside. The depositor at the bottom of the cap structure is the residual loss-absorber, with explicit protection via deposit insurance schemes funded by the rest of the banking system and, in extremis, the sovereign. The implicit taxpayer backstop at the very bottom is not a flourish. It is what makes the option valuable. Without an implicit floor, the executive’s claim would not be a call — it would be a position in a residual claim with genuinely unbounded downside, and the optionality that drives the compensation argument would disappear.

The empirical evidence is consistent with what theory predicts. Cheng, Hong, and Scheinkman, in their 2015 Journal of Finance paper, showed that US banks with higher residual pay (the unexplained portion of total executive compensation) were more likely to fail in 2008, controlling for size, leverage, and asset composition. Bebchuk, Cohen, and Spamann had earlier documented, in The Wages of Failure (Yale Journal on Regulation, 2010), that the senior executives of Bear Stearns and Lehman Brothers extracted some $2.4 billion in cash bonuses and equity sales between 2000 and 2008 — money that did not flow back to creditors or to the FDIC when the firms failed. The compensation system, in their phrasing, was structured so that executives “made money during the build-up of risk that crashed their firms.” Cerasi, Deininger, Gambacorta, and Oliviero (BIS Working Paper 630, 2017) found that across a large international panel, banks with more equity-linked CEO compensation had higher CDS spreads and higher Z-score volatility — consistent with the option-like payoff inducing more risk.

The structural question this poses for regulation is whether the asymmetry can be addressed by any policy tool other than direct intervention in compensation structure. The Bebchuk-Spamann answer is essentially no. Capital requirements reduce the option’s intrinsic value but do not eliminate the convexity. Bail-in shifts more loss-absorption onto debt holders but does not change executive incentives. Deferred compensation rules push the payoff out in time but do not address its option-like nature. The only structural fix is to change what executives are paid with — to give them claims that share in the downside, not just the upside.

The parallel to today’s PIK structures is not hard to draw. The GP of a private credit fund has a similar option-like payoff: 20% carried interest above a hurdle (the upside), management fees on AUM (a base layer that does not decline with NAV losses below a certain band), and limited personal capital at risk in the fund. The compensation asymmetry is structurally identical to the bank-executive case Bebchuk and Spamann formalised. Only the capital-structure terminology differs.

What the EU has actually tried

The European post-crisis architecture has gone further than the US on incentives. This is not a partisan claim — it is the empirical record of legislation and implementation.

The BRRD (Bank Recovery and Resolution Directive, 2014) and SRMR (Single Resolution Mechanism Regulation, 2014) established a framework that placed loss-absorption onto a hierarchy of bondholders before any taxpayer support could be deployed. Article 18 of the SRMR specifies the three tests that must be met for SRB-led resolution: (a) the bank is failing or likely to fail; (b) no private or supervisory alternative exists; and (c) resolution is in the public interest. The framework was designed to make TBTF support politically and operationally costly enough that managers and creditors would price the bail-in risk into their decisions.

MREL (Minimum Requirement for Own Funds and Eligible Liabilities) operationalised the framework: each significant bank must hold a portfolio of bail-in-eligible debt sufficient to cover potential losses and a recapitalisation amount. The SRB’s MREL Dashboard reports that the banks under its mandate had built up MREL stocks averaging close to 28% of risk-weighted assets by end-2024 (SRB MREL Dashboard, end-2024) — well above pre-crisis subordinated debt levels.

CRD IV’s remuneration framework went further. From 2014, variable pay for identified staff was capped at 100% of fixed pay, extendable to 200% with shareholder vote. Deferral periods of 4–5 years became mandatory, with malus and clawback provisions for risk-management failures discovered after vesting. EBA Guidelines (EBA/GL/2021/04) provide the implementation detail. The CRD V update (2019) tightened the regime further on smaller and mid-sized institutions, addressing earlier proportionality exemptions.

ECB-led supervision via the SSM, established in 2014, provided centralised micro-prudential oversight of significant institutions, with SREP capital add-ons (Pillar 2 Requirement and Pillar 2 Guidance) giving the supervisor institution-specific discretion to layer capital requirements on top of Pillar 1.

This is, on paper, a more ambitious regulatory architecture than the US framework. Dodd-Frank’s bail-in framework (Orderly Liquidation Authority) has never been invoked since enactment in 2010, and is subject to 2018 Treasury guidance that narrowed the practical path to OLA, emphasising bankruptcy as the preferred route. The US compensation rules under Dodd-Frank Section 956, which would have imposed deferral and clawback requirements on incentive compensation at large banks, were proposed in 2011 and again in 2016 and have still not been finalised and implemented, despite being re-proposed in 2024. The Volcker Rule, while implemented, was substantially weakened in the 2020 amendments that loosened its application to proprietary trading and merchant banking.

What Europe attempted, the US did not try — or tried and abandoned. This is worth saying directly, because it sets up the question the next section takes on: where the European architecture has been tested in real cases, what did the results actually show?

Two natural experiments: bail-in and the bonus cap

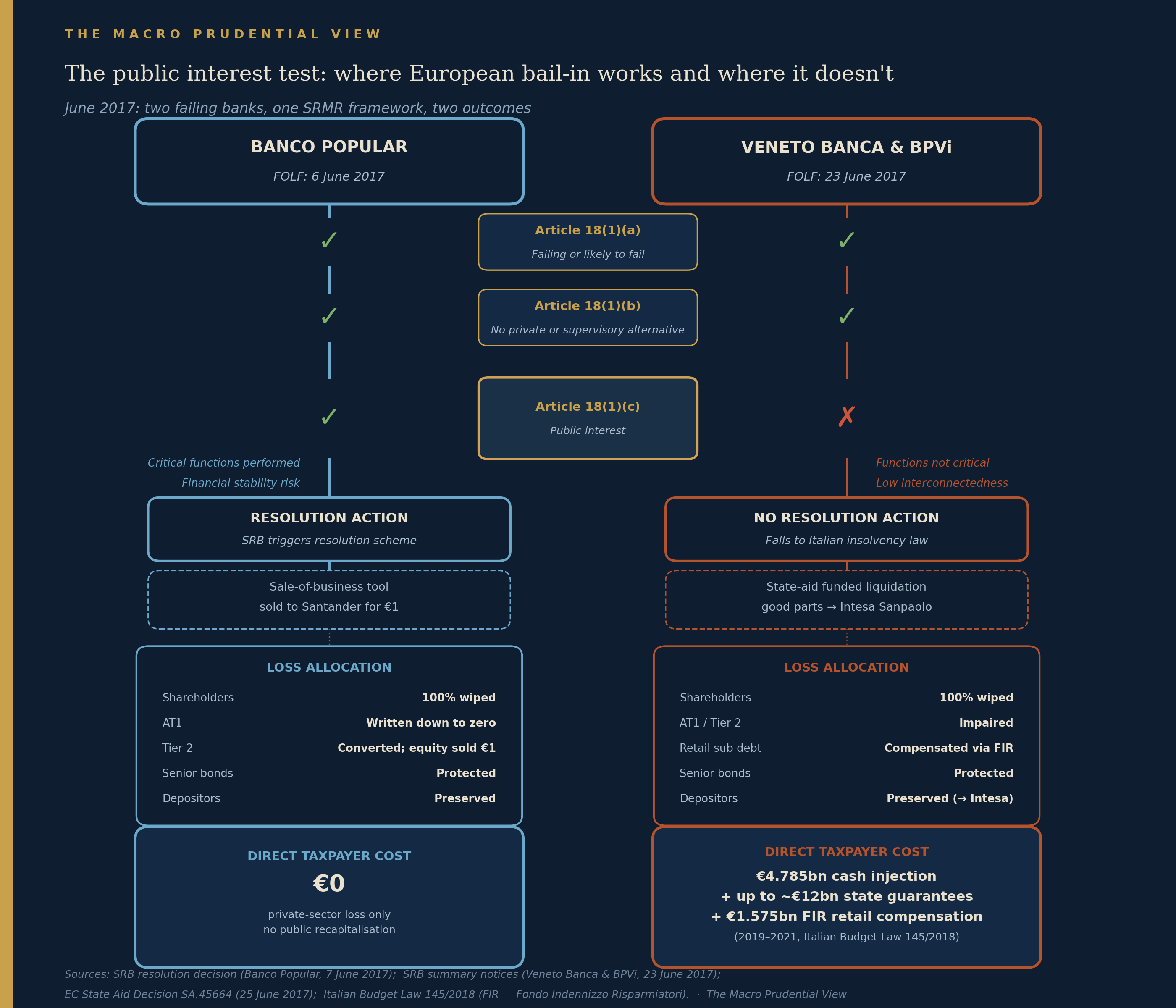

Two events in 2017 provide the cleanest natural experiment we have on bail-in. Both involved failing banks meeting Article 18(1)(a) and (b) of the SRMR — failing or likely to fail, with no private alternative. Both required the SRB to decide whether to invoke resolution under (1)(c)’s public interest test. The two outcomes diverged completely.

Banco Popular was declared failing or likely to fail by the ECB on 6 June 2017, after a deposit run and an ELA collateral shortfall that left the bank unable to reopen on 7 June. The SRB triggered resolution within hours, applied the bail-in framework, and sold the bank to Santander for €1 on the morning of 7 June. The cap structure was applied as designed: shareholders 100% wiped, AT1 written down to zero, Tier 2 converted to equity which was then sold to Santander for €1, depositors preserved. Direct taxpayer cost: €0.

Veneto Banca and Banca Popolare di Vicenza were declared failing or likely to fail by the ECB on 23 June 2017, with the SRB issuing a same-day determination that resolution was not in the public interest under Article 18(1)(c). The reasoning given was that the banks’ functions were “not critical,” interconnectedness was “low,” and Italian insolvency proceedings would achieve resolution objectives to the same extent. The banks were placed into national liquidation. The European Commission approved Italian state aid for the resolution under Commission Decision SA.45664 within 48 hours.

The state aid package was substantial. The Commission decision authorised cash contributions to Intesa Sanpaolo of €4.785 billion (€3.5bn cash, €1.285bn restructuring lump sum), plus state guarantees of up to ~€12 billion on the funding gap and NPL transfer. Subsequent retail-bondholder compensation through the Fondo Indennizzo Risparmiatori, established by Italian Budget Law 145/2018, added another €1.575 billion over 2019–2021.

The reading I take from these two events — and others may read them differently — is that the bail-in framework works when it works, and the question is when it works. The Article 18(1)(c) public-interest test is the discretionary margin. In the Italian case, the public-interest test was applied in a way that allowed a national-law liquidation with state aid, effectively bypassing the SRB’s bail-in regime and shifting losses back to the sovereign balance sheet. The framework is the same in both cases; the application diverged on a single discretionary judgment.

This matters for incentives because what bondholders price is expected loss-absorption, not legal loss-absorption. If the expectation is that medium-sized banks in politically-sensitive jurisdictions can secure exemptions, the disciplining effect of the framework on bondholder behaviour is correspondingly diluted. This is not a critique of the framework or of the people applying it. It is an observation that the framework is structured to permit discretion at exactly the point where the structural-reform alternatives — which we will come to shortly — are structured to remove it. The CMDI (Crisis Management and Deposit Insurance) proposal of April 2023 is, in effect, an admission that the framework as it stands does not systematically work for mid-sized banks, and an attempt to plug the gap by expanding DGS use and resolution scope.

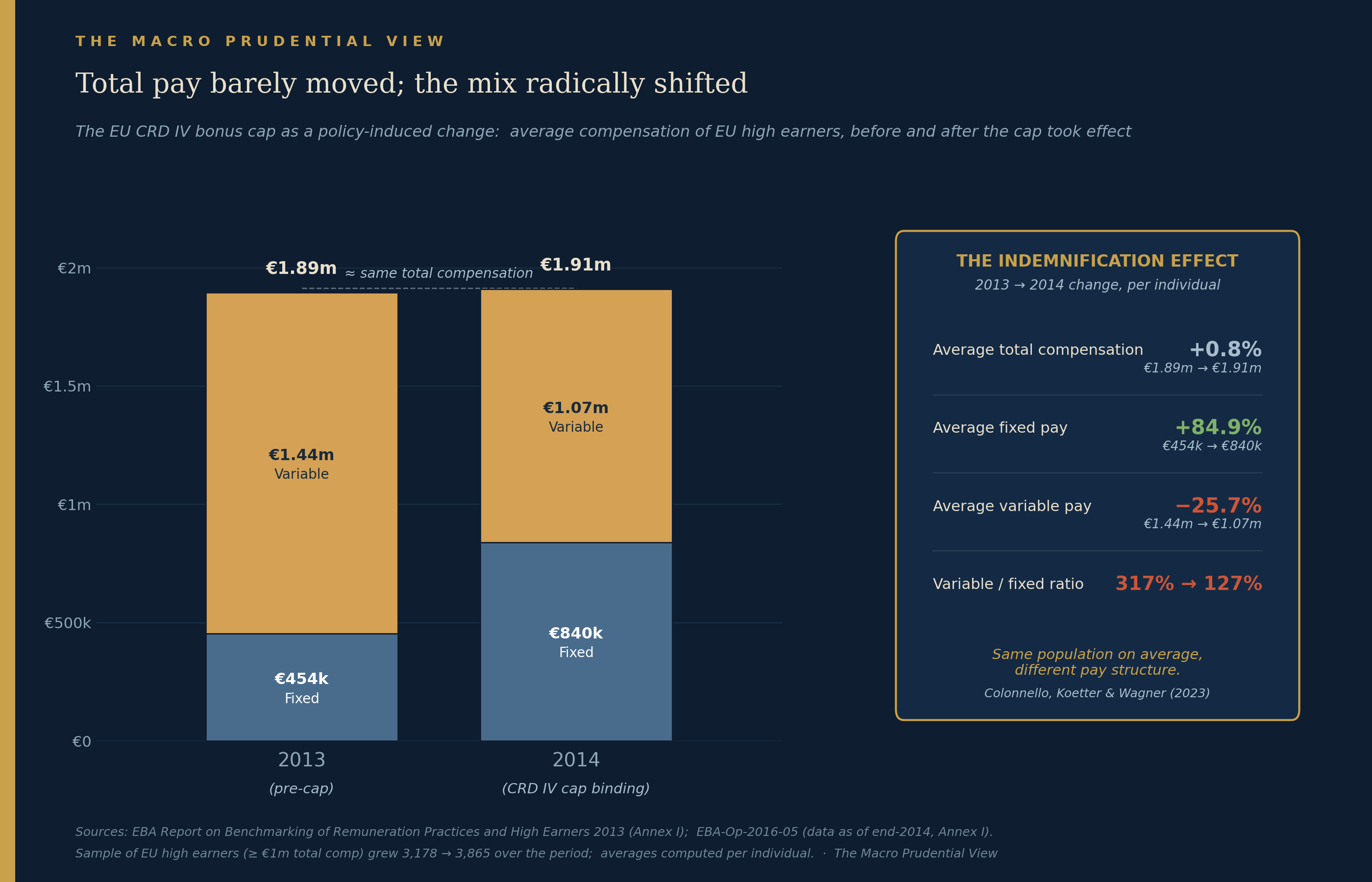

The bonus cap provides a different kind of natural experiment. EBA’s annual benchmarking of high-earner remuneration in EU banks reports the data needed for a clean comparison: 2013 (the last year before the cap, since CRD IV took effect for performance year 2014) and 2014 (the first year of binding cap).

The headline numbers are unambiguous. The average total compensation of EU high earners (≥ €1 million total compensation) was essentially unchanged: €1.89m in 2013, €1.91m in 2014. The composition flipped: average fixed pay rose from €454k to €840k (+85%), while average variable pay fell from €1.44m to €1.07m (−26%). The variable/fixed ratio collapsed from 317% to 127% — exactly as the cap mechanically required. The sample of EU high earners grew from 3,178 to 3,865 over the period as reporting harmonised, so the per-individual averages are the right metric for isolating the composition effect from sample growth.

Colonnello, Koetter and Wagner formalised the empirical pattern in their 2023 Journal of Accounting and Economics paper, using difference-in-differences identification on a larger panel of European banks. They documented what the literature calls the indemnification effect: banks responded to the variable-pay constraint by raising base salaries to maintain total compensation, with the level of total pay roughly preserved across the cap transition.

The economic interpretation matters. The cap was designed on the theory that variable pay drives risk-taking, and reducing variable pay relative to fixed pay should reduce risk incentives. The mechanical response of banks was to raise base salaries to maintain total compensation. This is exactly what the Bebchuk-Spamann framework would predict: if executive talent is competitively priced in a labour market, a constraint on one component of compensation will be offset by adjustments in others.

There is a second, less-discussed consequence worth flagging. By converting variable pay (which is cuttable in stress) into fixed pay (which is structurally rigid), the cap raised the operating leverage of EU banks’ compensation cost base. In a systemic downturn, variable pay can be reduced quickly to preserve capital; fixed salaries cannot. The cap, on this reading, did not just fail to discipline risk-taking — it made bank cost structures less flexible in exactly the scenario the regulator most cares about.

The UK provides the other end of the experiment. In October 2023, the PRA and FCA jointly removed the bonus cap entirely (PS9/23), citing exactly the arbitrage argument: the cap had pushed compensation toward fixed pay without reducing total compensation, and fixed pay is less responsive to performance — meaning the cap may have actually weakened the link between pay and risk discipline. Whether the UK was right to abandon the rule, or whether the abandonment trades one set of incentives for another, is a separate question worth its own essay. But the trajectory is striking: the UK first implemented the rule (as part of CRD IV transposition), saw a decade of evidence that the implementation did not achieve its goals, and abandoned it.

The same indemnification logic appears in today’s PIK structures, refracted into different vocabulary. The cap on cash distributions imposed by the RIC tax framework pushed BDCs to maintain headline distribution rates while their underlying cash receipts deteriorated. The constraint on one margin produced an adjustment on another: PIK accruals expanded, the dividend was funded by other means, and the headline numbers held. The system finds the path of least resistance — not because anyone is corrupt, but because every participant has private incentives pointing toward that path. The bonus cap and PIK are two manifestations of the same dynamic: rules that operate on one margin while the binding incentive operates on another.

Both cases illustrate the deeper pattern the rest of this essay develops. When regulation constrains one margin of the incentive structure, markets adjust on another — often in ways the original rule never anticipated. The question is whether the macroprudential framework can be designed to anticipate the adjustment, and whether the political-economy conditions exist to do so.

Goodhart’s boundary problem

The classical statement is Goodhart’s law: “Any observed statistical regularity will tend to collapse once pressure is placed upon it for control purposes.” Goodhart published this in the context of monetary aggregates in the 1970s, but the form is general. Any quantity that becomes a regulatory target ceases to be a reliable indicator of the underlying phenomenon, because the regulated population reorganises its activities to optimise against the target.

The macroprudential framework runs into a specific version of this problem. The framework is built on a regulatory perimeter — entities classified as banks, alternative investment funds, money-market funds, central counterparties — and within each perimeter operates with quantity-based instruments. The problem is that financial activity does not stay inside the perimeter when the regulatory cost of being inside it rises. The activity migrates outward, to non-bank vehicles, to off-balance-sheet arrangements, to jurisdictions and contractual structures where the regulator has less reach.

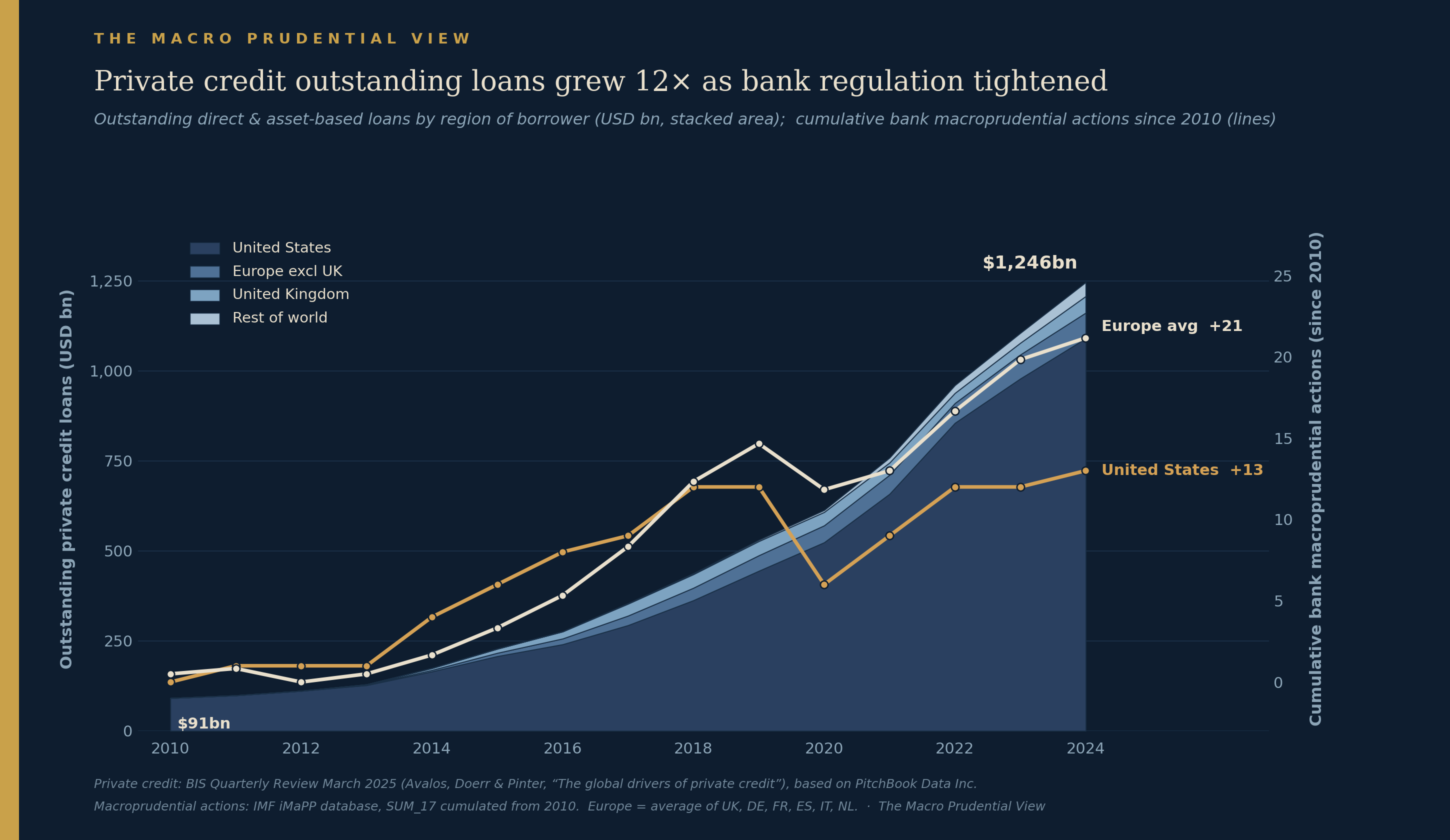

The empirical record on this is striking. iMaPP data — the IMF’s database of macroprudential actions covering 2010–2024 — show that European jurisdictions cumulatively implemented around 21 tightening actions per country on average, with the United States implementing around 13. Across the same period, the global private credit asset class grew roughly twelvefold, from $91 billion outstanding in 2010 to $1.246 trillion by 2024 (BIS data). The growth was not uniform — much of it concentrated in the latter half of the period — but the trajectory is unmistakable.

The pattern is not coincidence. As the quantity tools tightened on regulated balance sheets, the same credit risk migrated to the least-regulated edge — exactly as Goodhart’s boundary would predict. I want to be careful about what this correlation does and does not show. The chart does not establish that macroprudential tightening caused the migration to private credit. The growth of private credit is over-determined: yield-seeking institutional investors after a decade of low rates, the post-2008 retreat of banks from leveraged lending, the rise of private equity as the dominant ownership form in mid-market US business, regulatory arbitrage at the bank-fund interface. All of these mattered. The point is that the macroprudential framework was tightening throughout the period and did not, by its design, constrain the migration.

This is Goodhart’s boundary problem in the macroprudential context. The framework can tighten capital, tighten liquidity, tighten leverage limits for banks and for AIFs within its perimeter. It cannot, by direct instrument, prevent activity from migrating to entity types and contractual structures outside the perimeter. Each tightening creates marginal pressure for migration; the cumulative effect, over fifteen years, is a substantial transfer of credit-creation activity to vehicles where the prudential supervisor has less visibility.

The natural response — and the one that has been pursued throughout the period — is to expand the perimeter. AIFMD II in 2024 extended leverage limits and reporting requirements to a broader population of alternative funds. The FSB’s NBFI work programme since 2022 has tried to identify systemic activities across non-bank intermediaries and bring them within prudential reach. The ECB’s Macroprudential Strategy 2024 review specifically called out NBFI as a strategic priority.

Each expansion buys some visibility. But the expansion has a logical limit: every entity type the regulator brings inside the perimeter incentivises the next iteration of innovation outside it. The PIK arrangement in a BDC subscription line is a contemporary illustration. AIFMD II expanded the perimeter; the contractual structure that combines BDC distribution policy with sponsor IRR protection with GP carry economics sits at the contractual margin that no expansion of the entity perimeter directly reaches.

The deeper question is whether expanding the perimeter is the right response, or whether the regulatory architecture needs a different theory of where to act — one that operates on contract design rather than entity type. The next section takes on the three approaches that have been proposed and the frictions each runs into.

Three approaches, three frictions

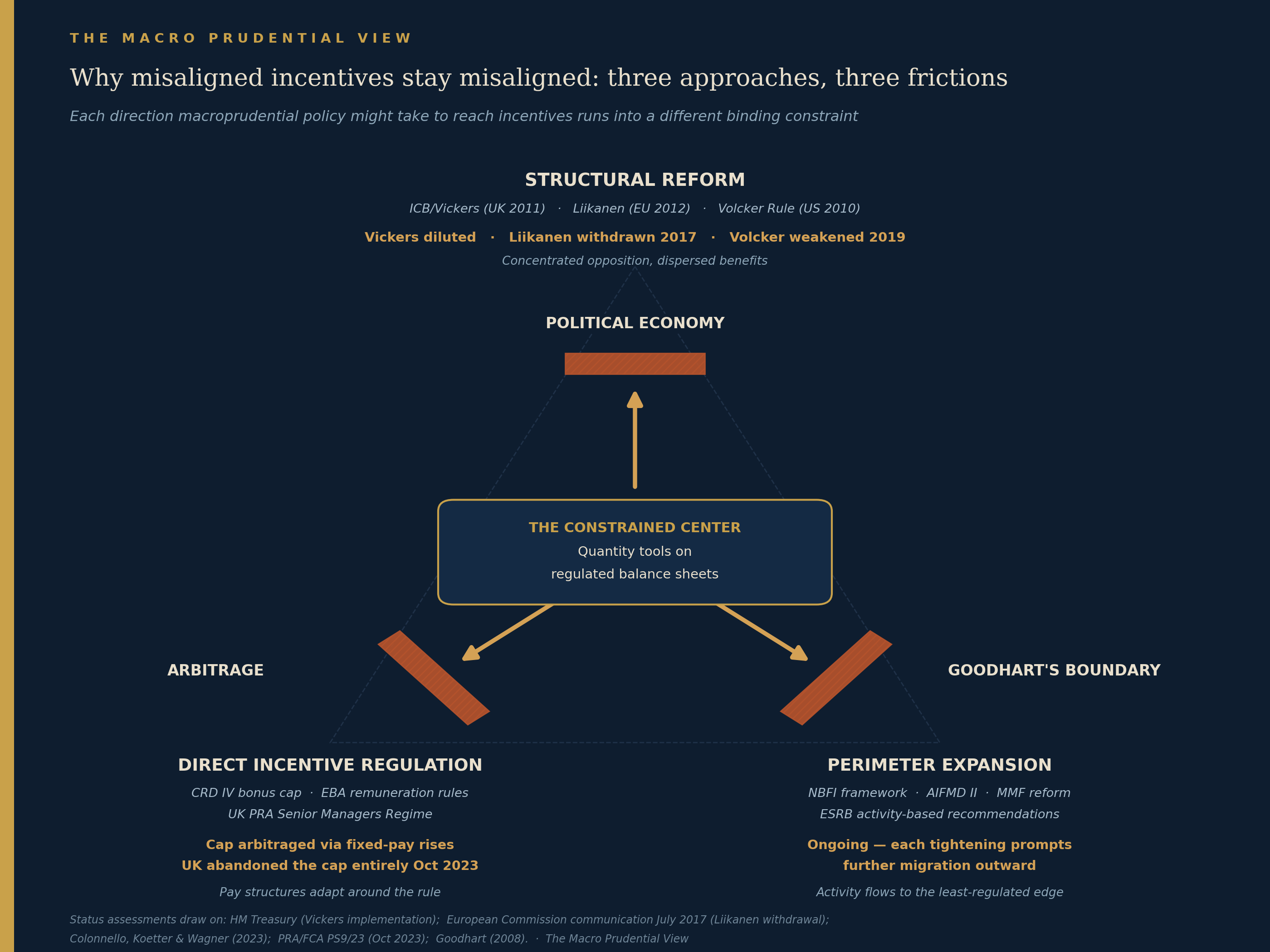

If the macroprudential toolkit, as currently designed, cannot directly reach the incentive structures that drive the kind of equilibrium described earlier, what are the alternatives? There are essentially three, and each runs into a different binding constraint.

The first approach is structural reform: removing the activities or organisational forms that generate the problematic incentives in the first place. The intellectual genealogy runs through Glass-Steagall, Vickers (the UK’s Independent Commission on Banking, 2011), Liikanen (the EU’s High-Level Expert Group, 2012), and the Volcker Rule (the US’s 2010 Dodd-Frank provision). The proposals differed in detail but shared a common logic: ring-fence retail banking from investment banking, or prohibit certain trading activities entirely, or break up entities deemed too complex to supervise. By altering the structure rather than the parameters, structural reform aims to remove the underlying option-like payoff that drives the Bebchuk-Spamann mechanism.

The friction is political economy. The benefits of structural reform are dispersed (general financial stability, fewer crises) while the costs are concentrated on specific institutions and their employees. Mancur Olson’s collective-action logic predicts exactly which side wins in this configuration. The UK’s ICB recommendations were implemented but in diluted form: the ring-fence applies only to the very largest banks and the operational separation has been progressively softened. Liikanen was formally withdrawn by the European Commission in 2017. Volcker survived but was substantially weakened in 2020. The structural-reform path has not failed for intellectual reasons. It has failed for political-economy reasons that were predictable in advance.

The second approach is direct incentive regulation: rules that target compensation structure, contract design, or specific forms of risk-taking directly. CRD IV’s bonus cap is the cleanest example. The UK PRA’s Senior Managers Regime, which makes senior managers personally accountable for prudential failures, is another. EBA’s remuneration guidelines, which constrain deferral periods, malus, and clawback, fall in this category. So do underwriting standards expressed in supervisory letters, which try to constrain how loans can be structured.

The friction is arbitrage. Pay structures adapt around the rule. The bonus cap pushed compensation toward fixed pay without reducing total compensation. The Senior Managers Regime has changed reporting lines without obviously changing behaviour. Underwriting guidelines on covenant-lite loans were largely ignored because they were not formally binding. Where rules are binding, the regulated population adapts; where they are not binding, the rules do not have force. The UK’s decision to abandon the bonus cap in October 2023 is the most direct admission of this dynamic.

The third approach is perimeter expansion: bringing new entities and activities under the prudential framework as they emerge. AIFMD, MMF reform, the FSB’s NBFI agenda, ESRB activity-based recommendations all sit here. The logic is to chase the activity wherever it goes, rather than to constrain what activity can do.

The friction is Goodhart’s boundary problem — the issue covered in the previous section. Each tightening creates marginal pressure for migration outward. The perimeter expands; the next iteration of innovation appears at the new margin. The expansion is necessary — without it, activity migrates faster than the framework adapts — but it is not sufficient, because the dynamic does not converge to an equilibrium where the framework catches all systemic activity.

Each of these approaches has had its serious advocates. Each is genuinely useful at the margin. None has been able to address the core problem at scale, because each runs into a different binding constraint. The structural-reform proposals are diluted by political economy. The direct-incentive rules are arbitraged. The perimeter expansion is chased by Goodhart’s logic.

(A separate debate, which I am consciously not engaging with here, concerns whether the European architecture can be made more credible by completing Banking Union — common deposit insurance, full single rulebook, removal of national exemptions on resolution. That conversation is important, but it is about credibility within the existing framework, not about the framework’s reach. This essay is about the latter.)

What this leaves is a macroprudential framework that has done what it was designed to do — capitalised banks, made them more liquid, made them less concentrated — but that has not addressed and probably cannot address the kind of equilibrium I described at the beginning. The PIK creep, on this reading, is not the result of regulatory failure in the conventional sense. It is the natural expression of a framework that operates on quantities while the binding incentives operate on contracts.

What might move the needle

Against this backdrop of institutional frictions, what, if anything, can macroprudential authorities do to move the equilibrium? I am going to be modest about claims here. I do not think there is a single instrument that resolves the problem this essay has been describing. What I do think is that the framing of the policy debate has, over fifteen years, settled into asking the wrong questions — and that reframing the questions is, in itself, useful.

Three angles deserve more attention than they have received.

The first is transparency and data infrastructure. The FSB’s May 2026 report on private credit is candid about the data gaps. The most actionable response is not to wait for harmonised disclosure regimes, which are slow to negotiate and easy to dilute. It is to make existing reporting infrastructure work harder. AIFMD reporting templates could be extended to require loan-level disclosure on PIK accruals, covenant amendments, and valuation methodologies. Bank reporting on subscription lines and NAV-backed facilities could be made granular enough that supervisors can see the underlying exposure rather than just the credit-line commitment. The MMF reform agenda showed that targeted disclosure requirements, well-designed, can have substantial effects on behaviour. The same logic should apply to private credit.

The second is the contractual margin. The cleanest insight from the bank-comp literature — that compensation should track the cap structure as a whole rather than just equity — is implementable. The “inside debt” literature, including Edmans and Liu (2011, Review of Finance) and the operationalisations proposed in Bebchuk-Spamann themselves, argues for compensating bank executives partly in subordinated debt or other loss-absorbing instruments (extensions of the deferral and malus logic already in CRD V, rather than departures from it). Various deferred-pay vehicles linked to bank-wide loss-absorption performance, rather than equity returns, are another path to the same end. The structural problem with the current framework is that it constrains the level of variable pay without constraining its composition. Constraining composition — requiring a portion to be linked to subordinated claims or loss-absorbing instruments — addresses the option-like payoff directly. For private credit, the analogue is GP carry structures that share in NAV declines as well as gains. Whether this is achievable through fund-prospectus disclosure requirements or through LP fiduciary standards is a separate question, but the structural fix is identifiable.

The third is credibility on the resolution framework. The Banco Popular/Veneto comparison is not an argument for abolishing the public-interest test. It is an argument for narrowing the discretion that the test permits, or for separating the politically-sensitive judgment from the technical resolution decision. The CMDI proposal moves in this direction by expanding the scope of resolution and clarifying the DGS-funded path for mid-sized banks. Whether the final version of CMDI, when negotiated, will narrow the discretion enough to change bondholder behaviour is an open question. But the direction of travel — narrowing rather than expanding the room for case-by-case judgment — is the right one if the framework is to have ex-ante disciplining effect.

I am not putting these forward as a programme. I am putting them forward as the angles that follow from the analysis. Each of them runs into one or more of the frictions described above. Transparency proposals face the same political-economy resistance that structural reform faces, but at lower intensity. Contractual-margin reforms face industry pushback comparable to compensation regulation in general, but with the advantage that the literature supporting them is robust. Resolution-framework credibility faces sovereign-political resistance, but the CMDI process suggests there is at least appetite for incremental progress.

What none of these does is dispose of the underlying problem. The configuration I described in the PIK case is, in my reading, a permanent feature of financial systems with private capital allocation, competitive funding markets, and a generalised expectation of public support in extremis. The point is not to dissolve it. The point is to slow its growth and to make its manifestations more visible to supervisors before they crystallise.

What we have established

This essay has tried to make a single argument with several supporting claims.

The argument is that macroprudential policy, as currently designed, operates on quantities — capital, liquidity, leverage, exposure — while the equilibria that drive financial fragility operate on incentives. The post-2008 reform agenda has made banks better capitalised, more liquid, and less concentrated, and that is a real and substantial achievement. But it has not addressed the contractual and structural margins where the next equilibrium is being built, and the design of the toolkit does not permit it to do so directly.

The supporting claims are five.

First, the PIK creep in private credit is not an isolated phenomenon. It is the contemporary expression of a pattern that runs back through cov-lite leveraged loans, through mortgage securitisation, through the S&L crisis: contractual or structural innovation that converts cash-flow stress into balance-sheet items that do not require immediate recognition.

Second, the equilibrium holds because every participant in the capital structure has private incentives pointing the same way. This is not corruption or incompetence. It is the natural product of the contractual and fiduciary structures within which the participants operate.

Third, the post-2008 capital framework, while a genuine success at what it was designed to do, has not addressed the structural asymmetry that Bebchuk and Spamann identified — the option-like payoff that bank executives hold on a thinly-capitalised cap structure. Capital regulation changes the size of the buffer between management’s incentive and the taxpayer, but does not change the asymmetry itself.

Fourth, the European post-crisis architecture has gone further than the US on incentive-side regulation, and the natural experiments — Banco Popular versus Veneto, the bonus-cap implementation between 2013 and 2014 — are genuinely informative about what direct incentive regulation can and cannot do. The bail-in framework works when the political conditions for invoking it exist; the bonus cap was arbitraged through fixed-pay adjustments that left total compensation roughly unchanged.

Fifth, each of the three approaches to addressing incentives directly — structural reform, direct incentive regulation, perimeter expansion — runs into a different binding constraint. Structural reform is diluted by political economy. Direct incentive regulation is arbitraged. Perimeter expansion is chased by Goodhart’s boundary problem. None of these is a fatal objection; all of them are reasons why progress has been incremental.

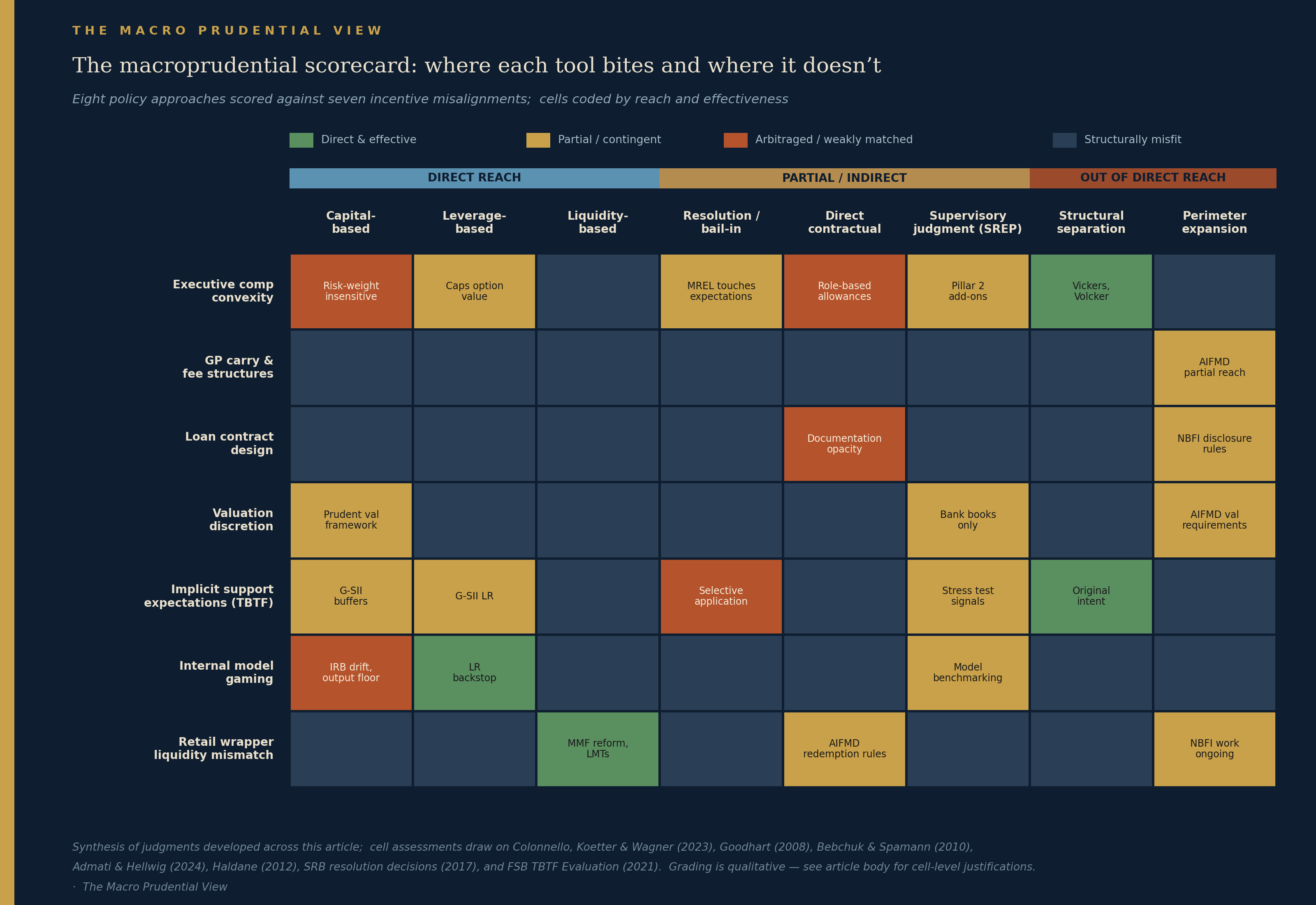

The macroprudential scorecard in the chart above is the synthesis of this argument. Most cells in the matrix are grey — pairings of policy tools with incentive types where the tool does not, by its design, reach the incentive. The dominance of grey is the visual restatement of the argument: most policy tools do not apply to most incentive structures. The handful of green cells indicate genuine matches, mostly in the leverage-ratio backstop against model gaming and the liquidity-tool response to retail wrapper mismatches. The yellow cells are partial matches, often through AIFMD’s reach into fund-side activities. The red cells — risk-weight insensitivity to compensation convexity, the role-based-allowances arbitrage of the bonus cap, selective application of the public-interest test, the documentation opacity of PIK and covenant-lite — are the explicit cases of arbitrage where the rule was tried and the market adjusted around it.

Which brings us back to where we started. PIK in first-lien private credit is the latest expression of this incentive pattern. It is not a fraud, it is not a bubble, and it is not the product of regulatory failure in the narrow sense. It is the natural equilibrium of a system in which every participant — borrower, sponsor, GP, LP, BDC, bank — has private incentives pointing the same way, and in which the macroprudential framework, as currently designed, cannot reach the contractual margin where the equilibrium forms. Whether the next downturn crystallises the underlying credit problem in private credit, in some adjacent corner of the financial system, or — most likely — in a form that nobody is currently watching, the structural argument is the same. The fault line is at the contractual margin. The toolkit operates on the balance sheet.

That is the wrong margin. And the structural reason it is the wrong margin is not that the macroprudential framework has failed. It is that the framework was never designed to act there in the first place.

Paweł Fiedor - The Macro Prudential View

Views expressed are personal and do not represent the institutions with which the author is affiliated.

Sources and references

Chart 1 (PIK creep timeline) compiled from author’s aggregation of SEC EDGAR 10-K and 10-Q filings for the top fifteen exchange-traded BDCs, four-quarter rolling basis. Ares Capital Corporation first-lien PIK share computed from ARCC Schedule of Investments (measured by fair value). Chart 5 (bail-in case comparison) drawn from SRB Decision SRB/EES/2017/08 on Banco Popular Español S.A. (7 June 2017); SRB Decision SRB/EES/2017/11 and SRB/EES/2017/12 on Veneto Banca S.p.A. and Banca Popolare di Vicenza S.p.A. (23 June 2017); European Commission State Aid Decision SA.45664 (25 June 2017); and Italian Budget Law 145/2018 establishing the Fondo Indennizzo Risparmiatori. Chart 6 (bonus cap natural experiment) computed from EBA Report on Benchmarking of Remuneration Practices and Data on High Earners 2013 (Annex I) and EBA-Op-2016-05, Report on Benchmarking of Remuneration Practices at EU Level and Data on High Earners (data as of end-2014) (Annex I), averages per individual. Chart 7 (private credit growth vs macroprudential tightening) uses private credit outstandings from Avalos, Doerr and Pinter, The global drivers of private credit (BIS Quarterly Review, March 2025) and cumulative macroprudential actions from the IMF integrated Macroprudential Policy (iMaPP) Database.

Cited reports and primary documents: FSB, Vulnerabilities Associated with Private Credit (May 2026); iCapital, Painting a PIKture: The Benefits and Risks of PIK in Private Credit (2025); SRB, Minimum Requirement for Own Funds and Eligible Liabilities (MREL) Dashboard, Q4 2024; European Commission, Proposal for a Regulation amending the BRRD and SRMR — Crisis Management and Deposit Insurance framework (18 April 2023); PRA, PS9/23: Remuneration: Ratio between fixed and variable components of total remuneration (’bonus cap’) (October 2023); ECB Banking Supervision, ECB Macroprudential Bulletin (various issues).

Cited academic literature: Admati and Hellwig, The Bankers’ New Clothes: What’s Wrong with Banking and What to Do about It (Princeton University Press, expanded 2024 edition); Bebchuk and Spamann, “Regulating Bankers’ Pay”, Georgetown Law Journal 98 (2010); Bebchuk, Cohen and Spamann, “The Wages of Failure: Executive Compensation at Bear Stearns and Lehman 2000-2008”, Yale Journal on Regulation 27 (2010); Cerasi, Deininger, Gambacorta and Oliviero, “How post-crisis regulation has affected bank CEO compensation” (BIS Working Paper 630, 2017); Cheng, Hong and Scheinkman, “Yesterday’s Heroes: Compensation and Risk at Financial Firms”, Journal of Finance 70 (2015); Colonnello, Koetter and Wagner, “Compensation regulation in banking: Executive director behavior and bank performance after the EU bonus cap”, Journal of Accounting and Economics 76 (2023); Edmans and Liu, “Inside Debt”, Review of Finance 15 (2011); Galati and Moessner, “Macroprudential Policy — A Literature Review” (BIS Working Paper 337, 2011); Goodhart, “Problems of Monetary Management: The U.K. Experience”, Papers in Monetary Economics (Reserve Bank of Australia, 1975); Haldane, “The Dog and the Frisbee” (speech at the Federal Reserve Bank of Kansas City Jackson Hole Symposium, August 2012); Tarullo, “Departing Thoughts” (speech at the Woodrow Wilson School, Princeton University, 4 April 2017).