What Poland's Growth Was Made Of

The composition of Poland's growth kept it out of the 2009 recession. The same growth left a Swiss-franc book it still hasn't cleared.

Macroprudential policy has a working theory of what makes a financial system safe. Keep household leverage from outrunning income. Keep the external position from depending on financing that can reverse overnight. Hold down currency mismatches on unhedged balance sheets. Lean against the procyclical build-up of all three. The toolkit — countercyclical capital buffers, loan-to-value and debt-service limits, restrictions on foreign-currency lending — is a set of instruments for producing a balance sheet that can take a shock without amplifying it.

Poland arrived at the 2008–09 crisis with much of that balance sheet already in place, and largely before it had the tools. The modern Polish framework — the systemic risk board, the activated buffers, the borrower-based measures — came mostly after 2011, after the events that made Poland look resilient. The resilience came first. My argument is that it came in significant part from the composition of Polish growth: not the headline rate of expansion but what the expansion ran on and how it was financed. By the time the crisis arrived, Poland already had several of the balance-sheet characteristics that macroprudential policy later seeks to preserve.

It did not have all of them. The same growth that kept aggregate leverage moderate sat on top of a Swiss-franc mortgage stock larger, in absolute terms, than Hungary’s. That is not a footnote to the argument; it is the argument’s other half. Poland’s growth composition was strong on two counts and weak on a third, and the count it failed on produced a concentrated vulnerability that the favourable aggregate picture could not see and that fifteen years of resolution has still not cleared. Aggregate resilience and concentrated fragility on the same balance sheet — that recurring pattern is the through-line of this piece. It appears before the crisis in the foreign-currency mortgage book, and it appears today in a deeply negative credit gap sitting over a flagged housing-market risk. The aggregate flatters; the concentration bites; the distance between them is where the macroprudential questions live.

A word on what this is. It is a structured comparison across a handful of European economies through one shock, not an identification strategy. The things I am separating — leverage, external financing, currency mismatch, real-economy structure, the exchange-rate regime — co-moved in the countries that had them, and I make no claim to have isolated any one. To keep the central term from swallowing everything, I use growth composition narrowly, in three parts: the leverage intensity of the expansion, the currency in which that leverage is denominated, and the liability structure of the external financing behind it. Two things sit deliberately outside that definition. A country’s structural endowment — domestic-market size, trade openness, sectoral concentration — is largely inherited rather than chosen, and it turns out to matter as much. The exchange-rate regime is a monetary choice that transmits the balance sheet into outcomes rather than forming part of it. Keeping these three layers apart is what stops “composition” from becoming a synonym for “everything that went right,” and it is what lets the argument concede, later, that composition was not always the decisive layer.

One thing this definition leaves out is worth naming rather than smuggling past. The sectoral destination of credit — whether the borrowing built tradable-sector capacity or financed property and consumption — is a genuine determinant of long-run resilience, and two economies identical on my three counts could differ sharply on it. I scope it out here on purpose: the evidence in this piece is about the financial structure of the expansion and the balance sheet it left behind, not about where the credit was ultimately deployed, and that allocation question deserves its own treatment rather than a fourth column bolted onto this one.

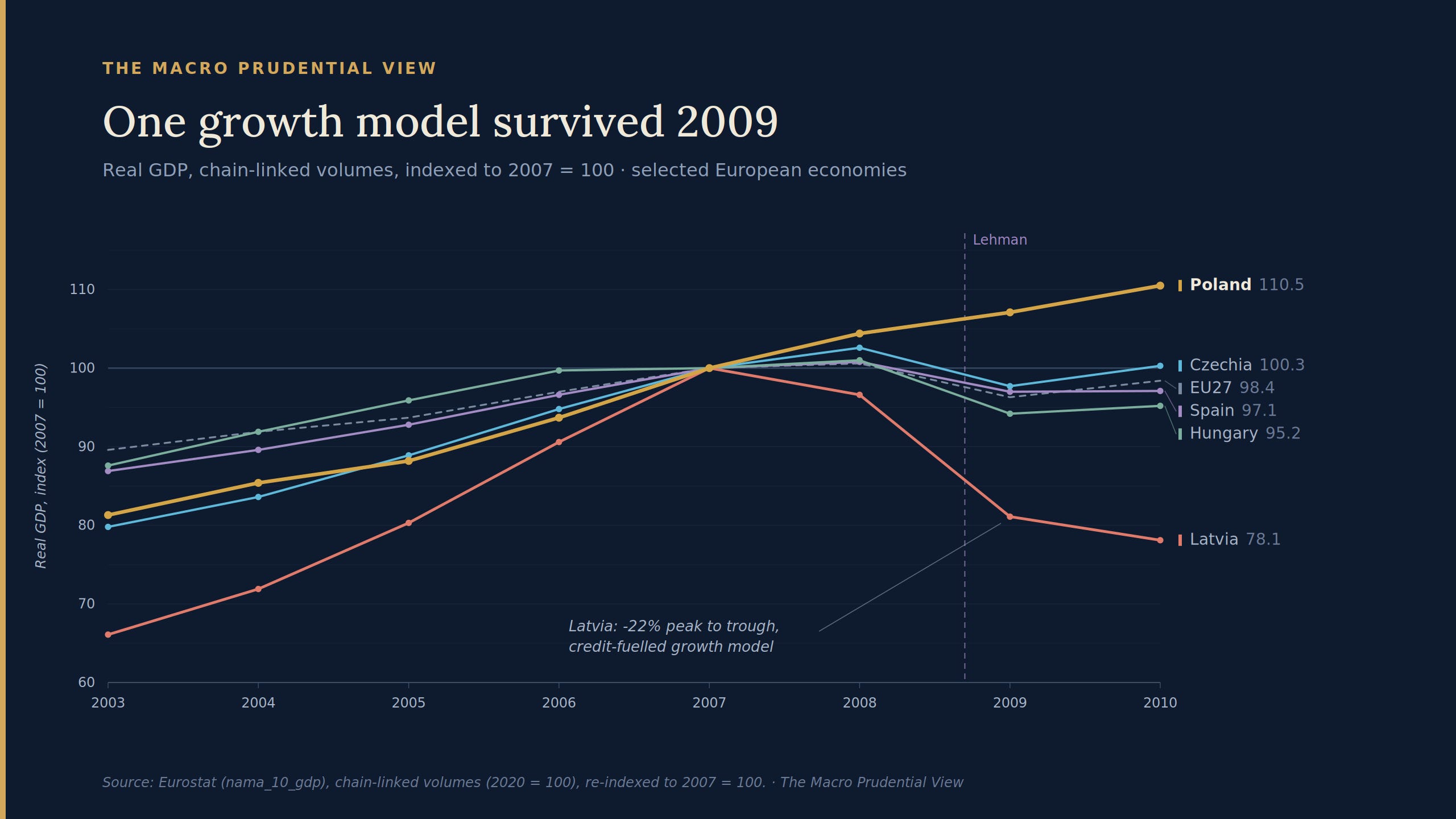

The puzzle

Poland was the only EU economy to avoid a recession in 2009. The point worth pressing is comparative, because Poland was not the only fast-growing economy in the region beforehand. Latvia, Hungary and the rest of the CEE bloc were converging on Western European incomes at speed; Spain was doing the same inside the euro area. They were all growing. The chart shows the growth resolving into a spectrum of outcomes rather than a clean binary, from Poland’s continued expansion through Czechia’s and Hungary’s moderate dips to Latvia’s collapse.

Headline GDP conceals the difference because it counts output regardless of what produced it. An economy expanding on a property and consumption boom financed by reversible foreign capital and one expanding on productivity and employment post similar numbers and carry different risks. The macroprudential question is whether the difference is legible before the shock rather than only in the wreckage.

One country should make the argument nervous from the start, so I will name it now. Czechia had a floating currency and low household leverage — much of what I am about to credit Poland with — and still contracted close to 5% in 2009. Hold that case. It is the test the argument has to pass, and I return to it once the mechanism is visible, because Czechia does not break the thesis so much as fix its limits.

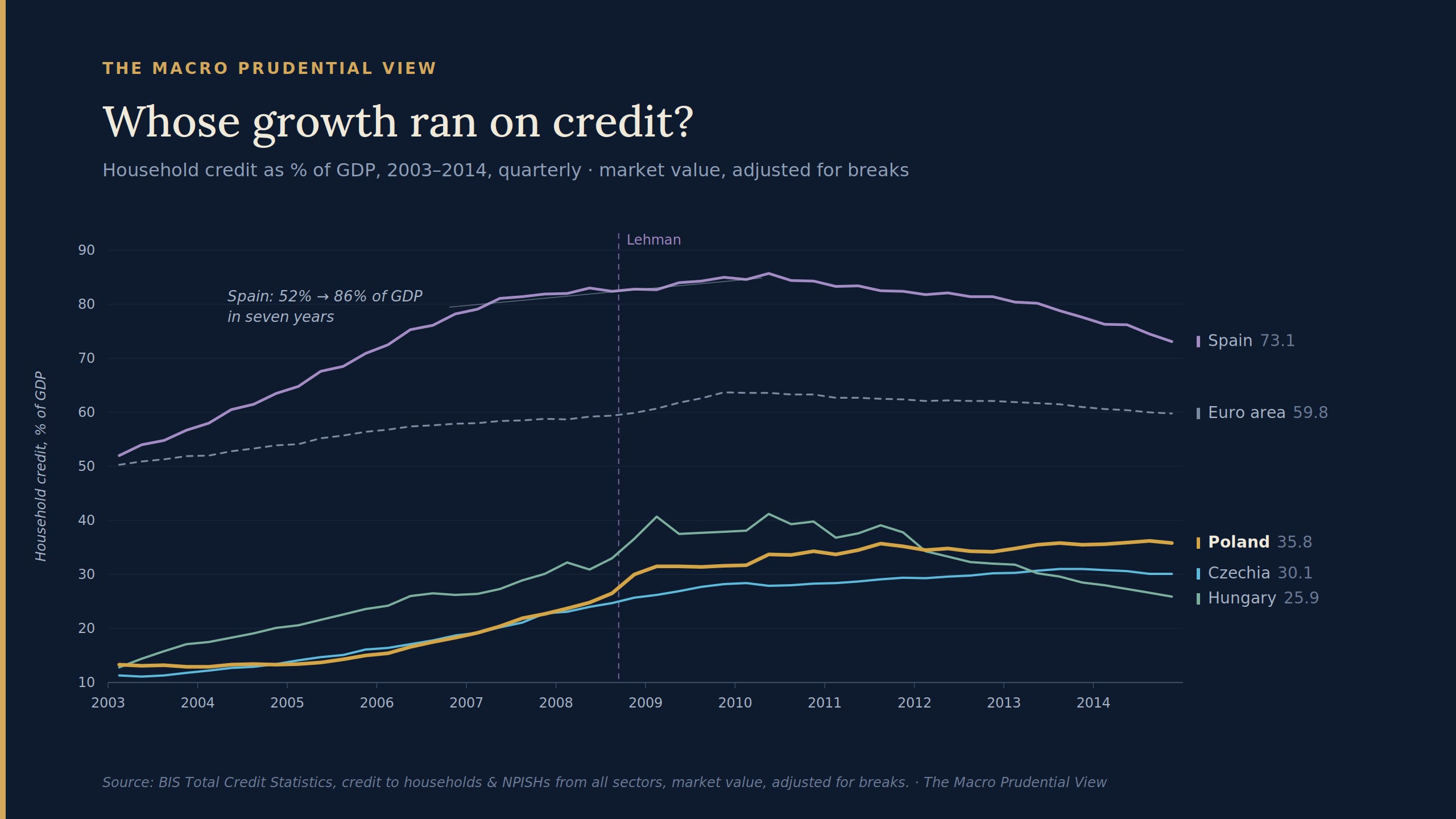

Aggregate leverage

By 2010 Polish household credit stood near 36% of GDP, Czechia’s at 30%, Hungary’s at 25%. Spain’s was 73% and had peaked near 86%. These are not points on the same distribution. Spain and the euro-area periphery had undergone a financial deepening of a different order, much of it into residential property; the CEE economies were building leverage from a lower base and more slowly. Polish credit grew, but in proportion to an economy itself expanding fast — leverage added to a denominator that was genuinely enlarging.

This is a leverage measure, not a decomposition of growth into productive and unproductive parts, and it should not be asked to carry more than it can. It does not establish that Polish growth was productivity-led and Spanish growth was not. It establishes something narrower: entering the crisis, Polish and Czech household balance sheets carried far less debt relative to income than Spanish ones, and were correspondingly less exposed to debt-deflation and to a rise in debt-service costs. That is the balance-sheet outcome a borrower-based macroprudential regime exists to produce, and Poland had it without yet having the regime. On the first of composition’s three counts — leverage intensity — Poland scored well.

The Hungarian line does something the others do not. It jumps, from around 37% in 2009 to 41% by mid-2010, then slides. That movement is not new lending; it is the forint depreciating and revaluing a stock of foreign-currency mortgages upward in domestic-currency terms. Ordinary credit does not behave like that. The line is carrying a currency mismatch, which is the cue to look at the mismatch directly — because Poland was carrying a larger one, and that is the count on which it did not score well.

The mismatch underneath

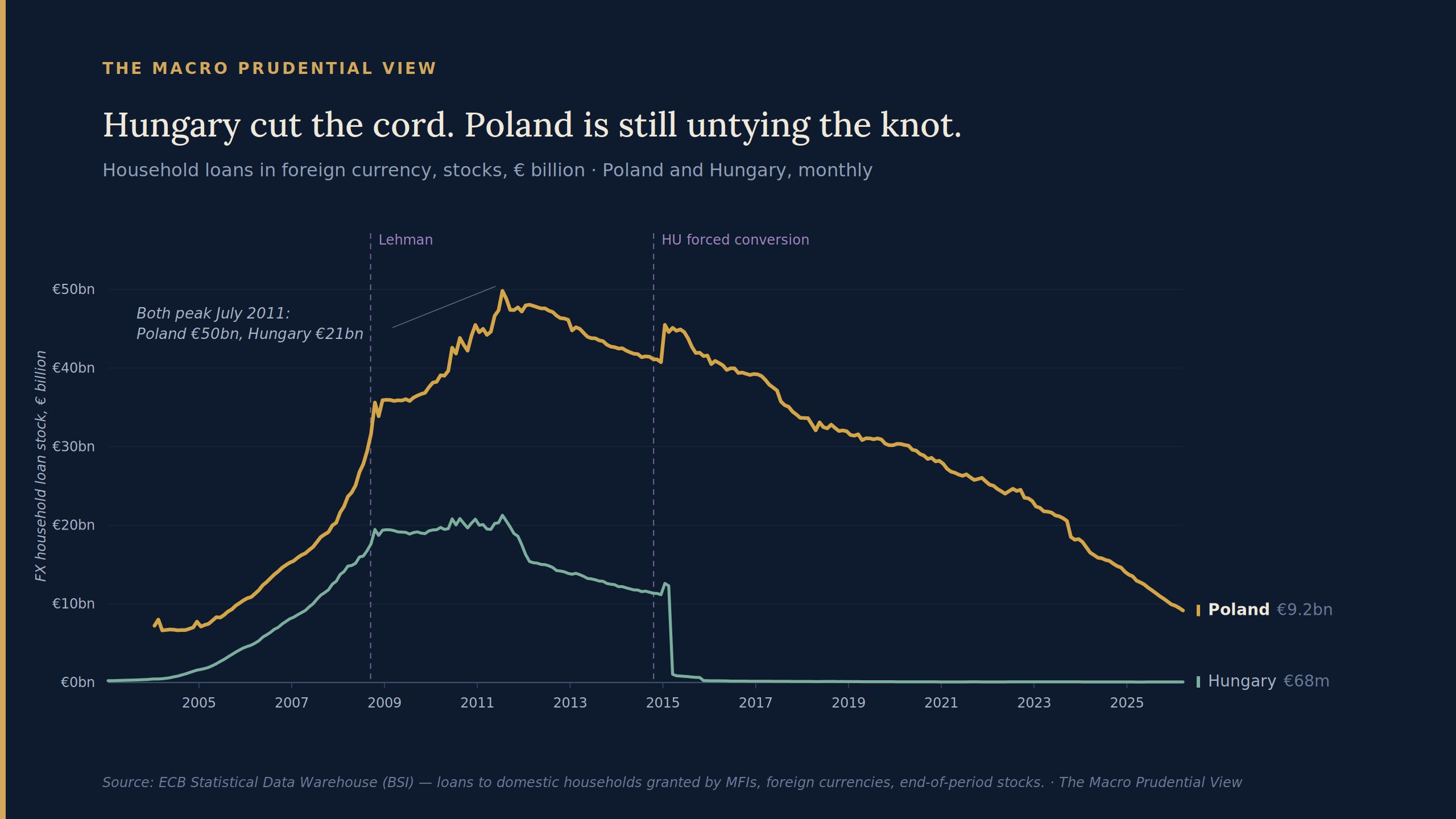

Poland’s household FX loans — overwhelmingly Swiss-franc mortgages — peaked near €50bn in July 2011, larger in absolute terms than Hungary’s €21bn, the exposure usually cited as the cautionary CEE case. This is the second count of composition, currency denomination, and Poland scored badly on it. The point needs stating carefully, because it is easy to overstate in either direction. The mismatch did not mean Poland’s aggregate leverage was secretly high: the €50bn book was around 13% of GDP, roughly a third of a household-credit ratio that was itself low, and stripping it out would leave Polish leverage lower still, not higher. Cheap Swiss-franc credit expanded mortgage access; it did not disguise a domestic-currency binge that would otherwise show. Low leverage and a concentrated currency mismatch genuinely coexisted. But a leverage ratio that is low and a third unhedged foreign currency is worth less as reassurance than the ratio alone suggests, which is exactly why currency denomination belongs inside the definition of composition and not outside it. Poland’s composition was mixed: strong on volume, weak on denomination.

Where did the denomination failure come from? Partly from the growth model, but not as cleanly as a tidy story would want. A fast-converging economy runs structurally higher inflation and therefore higher policy rates than the core, and the gap between złoty and Swiss-franc rates was wide and persistent; that differential created the pricing incentive for households to borrow in francs. The convergence process that shaped Poland’s macro balance also helped create the incentive for the mismatch. But the incentive was not the scale. Czechia and Romania were converging floaters with rate differentials of their own and did not build Poland-scale franc books; the differential was necessary, not sufficient. What turned an incentive into €50bn was supervisory tolerance of unhedged foreign-currency lending to households and the competition among foreign-owned banks to write it. The growth model lit the incentive; supervision and bank competition let it run. That distinction matters, because it locates the failure precisely where a tool could have acted — a cap or ban on foreign-currency lending to unhedged borrowers — and Poland’s tools were absent or weak through the build-up.

How the two stocks were resolved is a separate question from how they were built, and it runs along a different axis again: not growth composition but the capacity and willingness to act. Hungary extinguished its FX mortgage book almost completely through a forced conversion in 2014–15, converting borrowers to forint by statute, pushing the currency risk onto the banks, the exposure gone in roughly a quarter. Poland did not. Its stock has come down slowly, through amortisation and, since around 2020, through individual litigation, with Polish courts and the Court of Justice of the EU annulling Swiss-franc contracts on consumer-protection grounds. By mid-2022 the ESRB recorded almost 30% of CHF contracts in litigation; about €9bn remained outstanding in early 2026, with provisioning against the litigation a continuing drag on bank profitability.

On the narrow metric macroprudential authorities weigh most heavily — the speed with which a systemic mismatch leaves bank balance sheets — Hungary did better, doing in a quarter what Poland has not finished in fifteen years. Whether it did better overall is genuinely unsettled. Forced conversion carried a cost that does not appear as a balance-sheet line: a state that rewrites financial contracts by statute may raise the premium it later pays for bank and sovereign funding, with second-round effects on credit supply, though how large that cost was, and whether it exceeded the drag of Poland’s fifteen-year litigation overhang, is not something the evidence here settles. What the comparison does show is cleaner than a verdict. Hungary had the worse growth model and the greater resolution capacity, and used it; Poland had the better model and let the mismatch sit. Resolution capacity and growth composition are different things, and a country can be strong in one and weak in the other.

With both halves on the table — composition strong on leverage, weak on denomination, and resolution a separate axis entirely — the rest of the piece concerns the third count, external financing, and why Poland’s aggregate position held when the shock came.

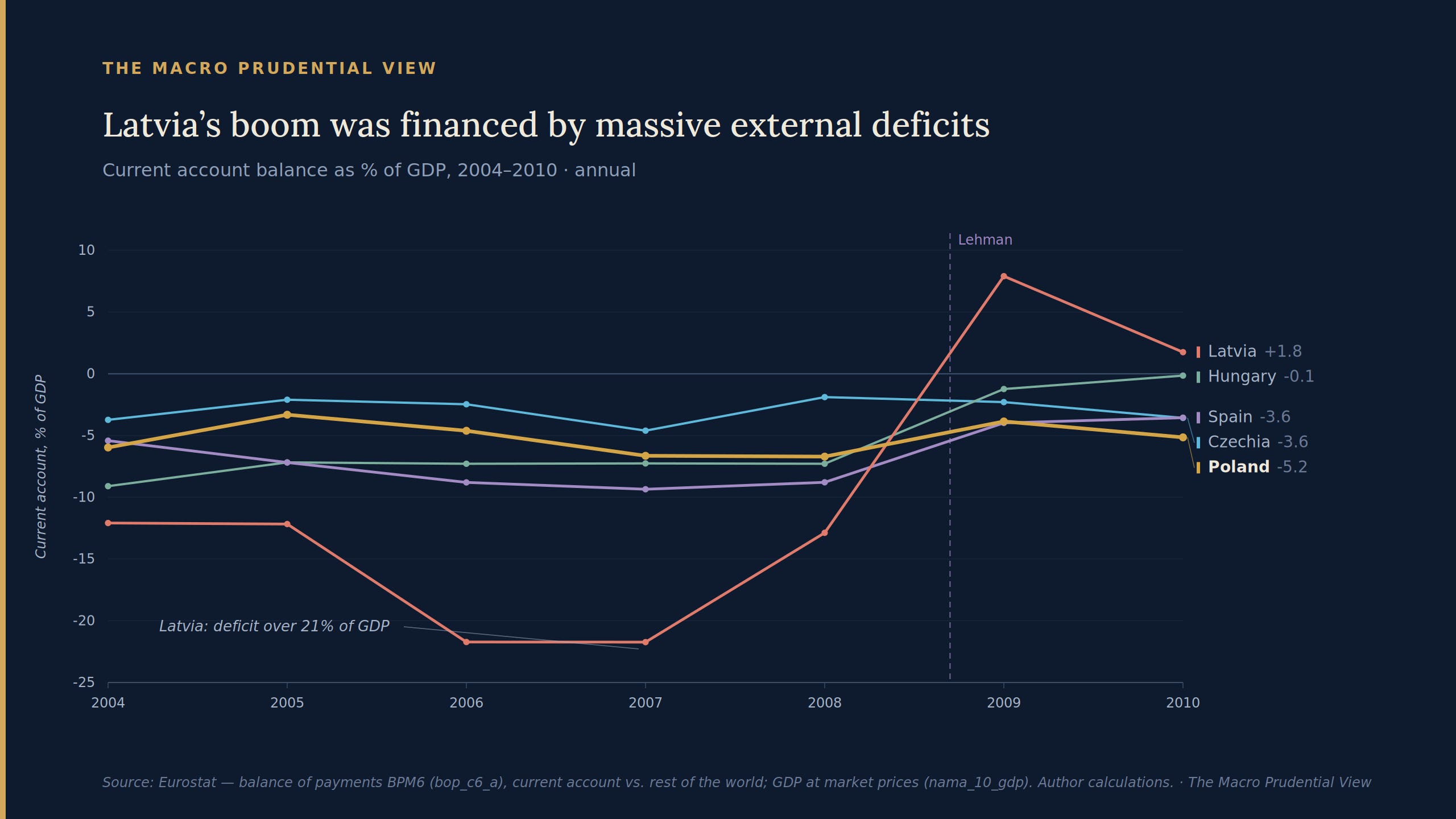

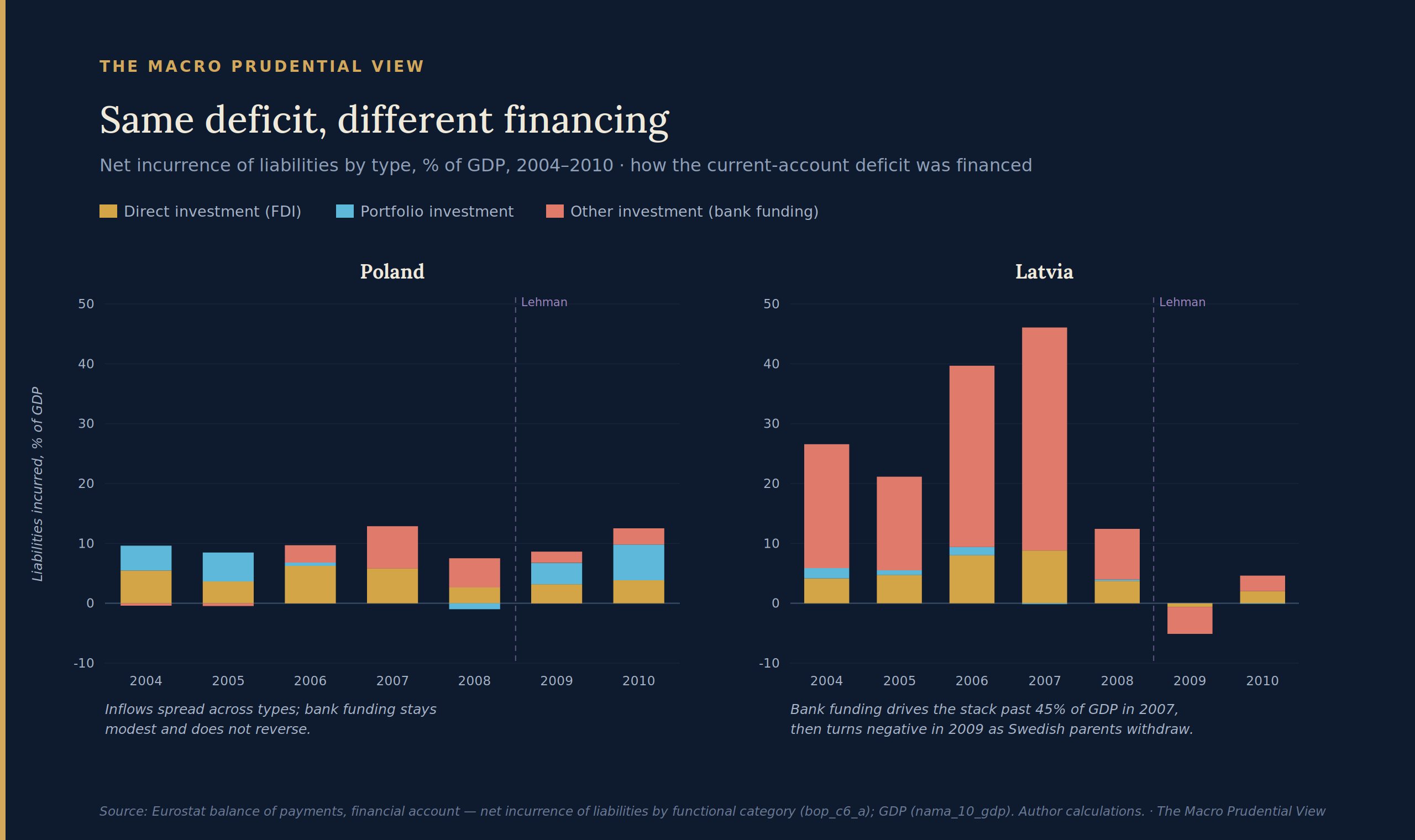

What financed the deficit

Latvia ran current account deficits above 21% of GDP in 2006 and 2007; when the financing stopped in late 2008 the deficit swung to surplus within a year, but only because imports collapsed and output fell by a fifth. Spain, inside the euro and so without the same risk of abrupt currency-driven flight, ran deficits near 9% and adjusted slowly through years of internal grind. Poland’s deficits stayed in the mid-single digits — not dramatically smaller than Hungary’s, and at points not far from Spain’s. The size of the deficit is not what set Poland apart. What differed was the liability side: how the deficit was financed, and how reversible that financing was.

The contrast is the point, and it is one of scale and reversibility rather than of one pure financing type against another. Latvia financed its deficit overwhelmingly through short-term cross-border bank funding, the bulk of it from Swedish parents — Swedbank and SEB — lending into their Baltic subsidiaries and onward into real estate. That funding ran past 37% of GDP at its 2007 peak, and it reverses on a trigger: in 2009 it went sharply negative as the parents pulled back. The Riksbank’s own retrospective identifies the Baltic crisis as a combination of fixed exchange rates, foreign-currency debt and heavy parent-company funding of bank subsidiaries; the ECB describes those banks coming under acute pressure when intragroup liquidity seized. Poland’s bank-funding component never approached that scale — it peaked around 7% of GDP — and it did not reverse in 2009. Poland’s inflows were spread across direct investment, portfolio investment and bank funding rather than concentrated in the one category that runs.

Three honest qualifications keep this from overreaching, and none of them dissolves the contrast. First, the categories are not airtight: portfolio investment is not a stable flow, and over the period it was at times Poland’s largest single inflow, so the claim is not that Poland leaned on sticky FDI but that it leaned far less on the specific reversible funding — short-term parent-bank lines — that turned the Baltic deficit into a sudden stop. Second, a meaningful share of Poland’s FDI went into the banking sector itself, foreign parents capitalising their Polish subsidiaries to fund exactly the retail-lending expansion, including the Swiss-franc mortgages, that produced the mismatch above; the liability structure governs rollover and sudden-stop risk, and on that it protected Poland, but it does nothing about the asset-side currency mismatch the same capital helped fund. Third, Poland’s own mix shifted under stress, with the bank-funding component rising in 2006–08, visible in the chart. The defensible claim is bounded and is enough: Poland’s external financing was structurally less reliant on the funding that can be cut in a quarter, which is why it avoided the sudden stop that crushed Latvia — and that is a different protection from the one the FX book needed and did not get.

What absorbed the shock

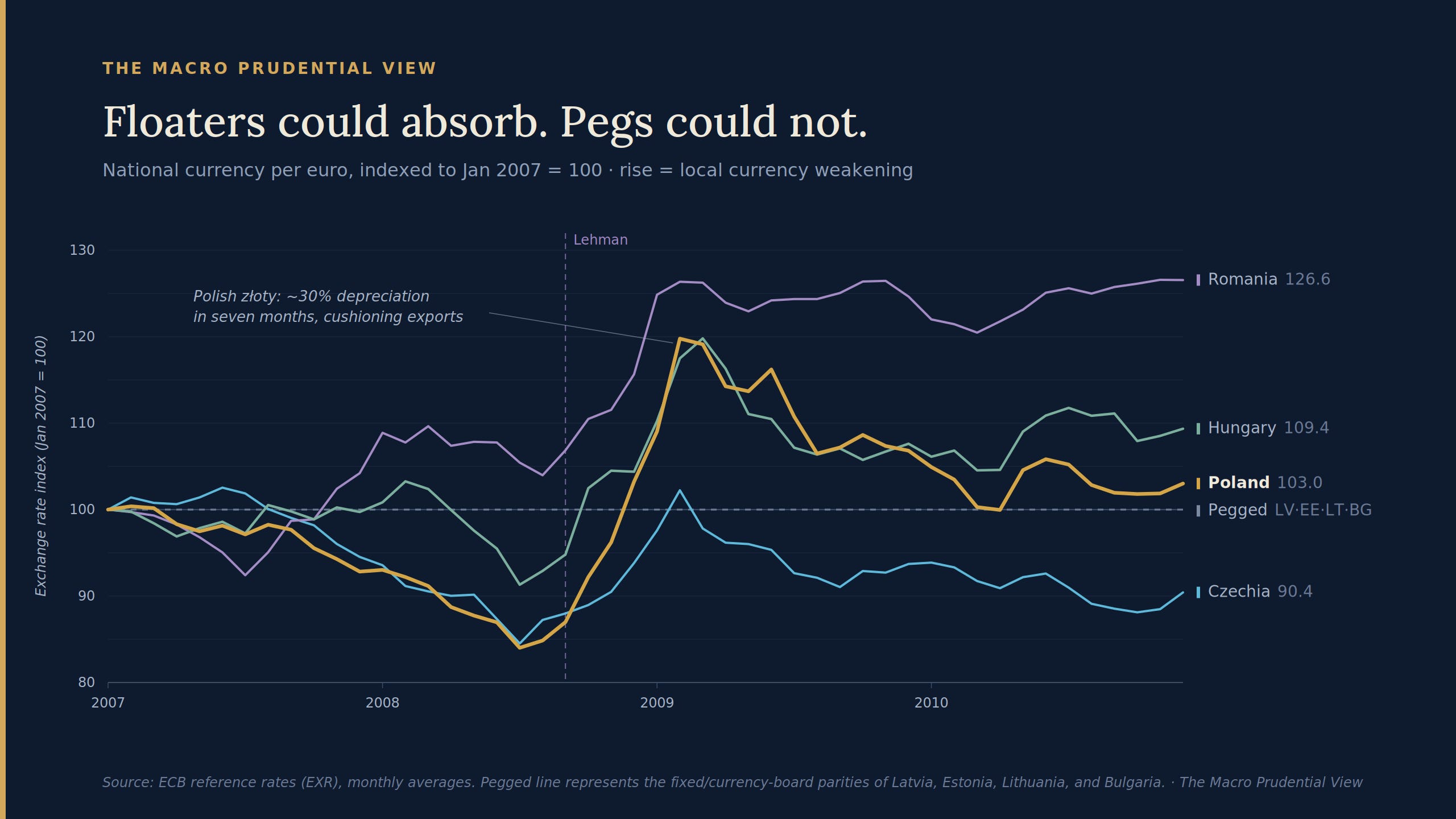

The exchange-rate regime is a monetary choice, not a feature of how Poland grew, and the two should not be merged. The złoty’s roughly 30% depreciation between mid-2008 and early 2009 said nothing about Polish growth composition; it reflected a decision to float. What the float did was transmit the balance sheet Poland brought to the crisis into the output it recorded through it. For an economy with a large tradable sector and a household balance sheet not catastrophically short foreign currency, depreciation works as a shock absorber: exports cheapen as domestic demand weakens, and the balance-sheet damage from the weaker currency stays contained.

That second condition is why the easy version — floaters absorb, pegs cannot — needs qualifying, and the qualification runs straight back through the FX chart. Depreciation absorbs a shock only where private balance sheets are not fatally short foreign currency. Hungary floated, and for Hungarian households with forint incomes and Swiss-franc mortgages the depreciation deepened the damage rather than cushioning it; the same currency move that helped Polish exporters tightened the screw on Hungarian and many Polish FX borrowers. The pegged Baltics sat at the other pole, unable to depreciate at all, and took the entire external adjustment through internal devaluation — falling wages, prices and employment, the channel that manufactures non-performing loans and the reason Latvian output fell by a fifth. The float did not create Poland’s resilience. It transmitted a balance sheet that was resilient at the aggregate level, and only to the extent that it was.

Czechia, and the part composition leaves out

Now the case held back. Czechia had a float and low household leverage — good marks on composition as I have defined it — and still contracted close to 5% in 2009. On composition alone the thesis would not survive it.

It survives because resilience required more than good composition, and Czechia is where the structural endowment I set aside earlier does its work. Czechia’s recession came through trade: a small, extremely open economy wired into German manufacturing supply chains, hit hard when those chains contracted in late 2008. A floating koruna helped at the margin but could not offset a collapse in foreign demand for the goods Czechia made. Poland’s larger domestic market and lower trade openness gave the złoty’s depreciation more to work with — more domestic demand to defend and proportionally less exposure to the single channel that carried the shock into Czechia.

I separated endowment from composition at the outset precisely so this would not read as the thesis stretching to absorb its counterexample. Domestic-market size and trade structure are not features of how a country chose to grow; they are largely inherited, and in Czechia’s case the inheritance was decisive. But the right conclusion is not that endowment beats composition and the article should pack up. It is that composition and endowment are distinct failure modes, and in this episode they produced damage of different depth. The countries undone by composition took the deep hits: Latvia, financed by funding that vanished, lost more than a fifth of output; Spain, carrying household leverage near 86% of GDP, lost most of a decade. The country undone by endowment took a shallower, recoverable one: Czechia contracted around 5% and was back above its pre-crisis level by 2010. I would not build a general law out of three outcomes from a single crisis. What this configuration shows is narrower and still useful: when the shock hit, the largest collapses sat with the financing and leverage failures, while a trade-endowment shock produced a normal recession Czechia walked out of. Composition was not the only thing that determined whether a shock was survived, but here it was the layer that travelled with the outcomes a supervisor most wants to avoid.

What I am not ruling out

Poland’s resilience is overdetermined, and honesty requires conceding that some of the omitted factors may be first-order rather than additive. EU structural funds were not merely a helpful inflow; they were a non-reversible source of external financing during precisely the window when private capital retreated, and a stabiliser of that kind weakens how far the Polish case generalises to converging economies without an EU anchor. Foreign-bank ownership, common across the region, interacted with Polish supervision and home-host arrangements differently than in the Baltics, in ways that are about supervisory practice as much as funding structure. Pre-crisis house-price excess was milder than in Spain or the Baltics. Fiscal space let the automatic stabilisers run. The absence of US securitisation exposure spared Poland the first-round hit. A large domestic market — which I have filed under endowment — may simply be one of the principal reasons Poland could absorb the external shock at all.

The claim is therefore not that growth composition was the cause, nor that it can be isolated from the bundle it travelled with. It is that composition is a coherent and observable organising lens for part of that bundle, that it sits upstream of the specific vulnerabilities macroprudential authorities track, and that it was legible in the balance sheet before the shock — which is more than can be said for “Poland was lucky,” a description of the outcome rather than the structure that produced it.

Where Poland stands now

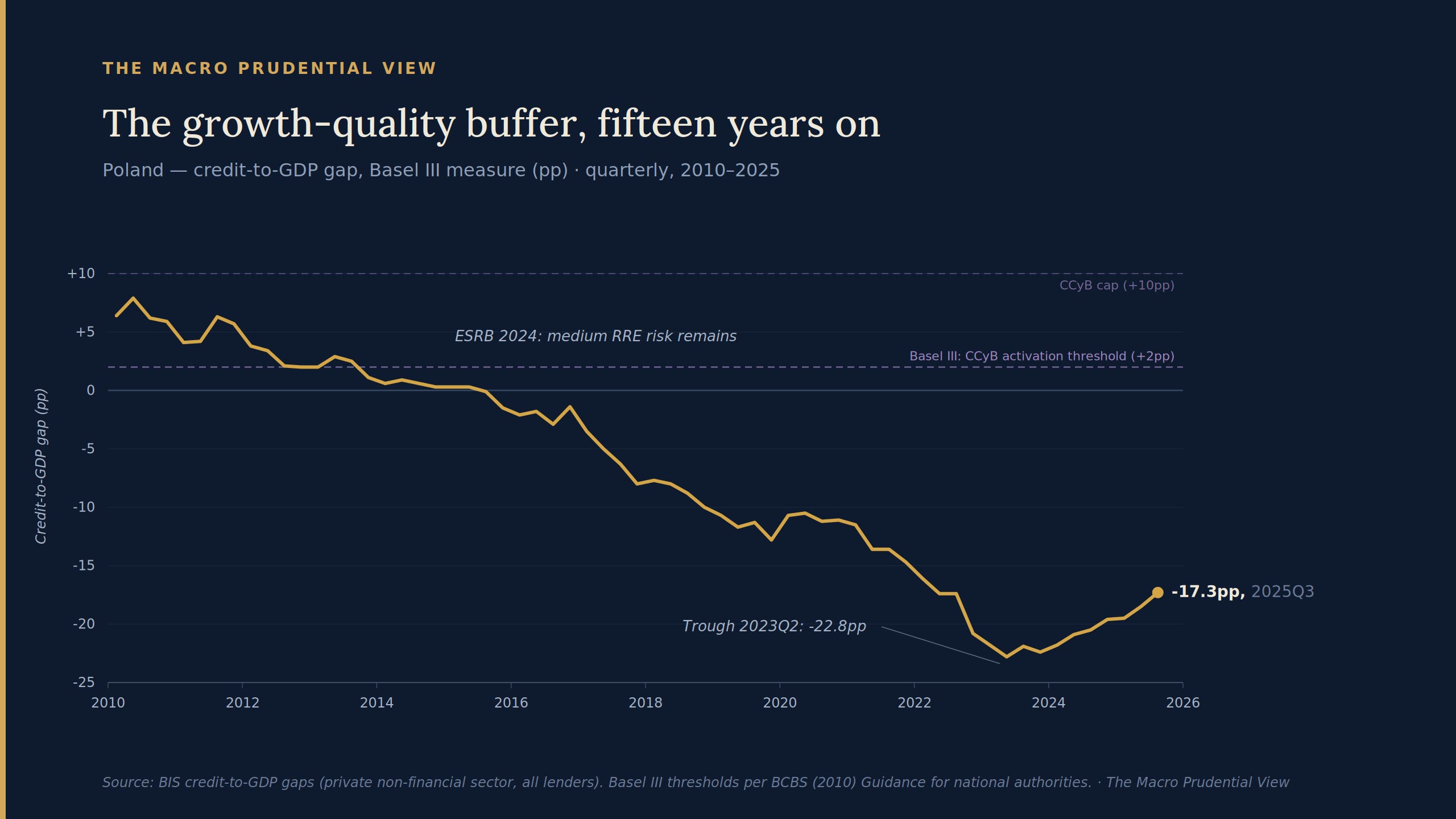

The credit-to-GDP gap is the indicator the Basel framework uses to signal whether a countercyclical buffer should be switched on; above +2 percentage points is the conventional activation level. Poland’s gap has been below that for over a decade and now sits around −17pp, having reached −23pp in 2023. Read literally, there is no credit boom in Poland and the economy is accumulating macroprudential space rather than spending it, which is why Poland’s authorities have kept the buffer rate inactive for most of the period.

The literal reading is the one to resist. A deeply negative gap is a descriptive residual — credit has grown more slowly than output — and a residual has several possible causes. Polish credit has been suppressed on the supply side as much as moderated on the demand side: a bank asset tax since 2016 that penalises lending relative to holding government securities, and capital tied up against the CHF litigation described earlier. Nominal output outrunning credit is consistent with a safe, well-balanced economy; it is equally consistent with a banking sector taxed and litigated into caution. The BIS gap is also known to be unstable in real time, sensitive to the trend it is measured against. I read it as a description of where credit sits relative to output, not as a verdict that Poland is safe.

The sectoral picture is where the verdict lives, and it returns to the through-line. The ESRB’s most recent residential real estate assessment still classifies Poland as medium stock risk, citing accelerating house prices, elevated debt-service ratios on new lending, a high share of variable-rate loans and the unresolved Swiss-franc legacy. A deeply negative aggregate gap sitting over a flagged housing vulnerability is the same configuration as the pre-crisis balance sheet: aggregate moderation on top of a concentration the aggregate cannot see. Fifteen years ago the concentration was a foreign-currency mortgage book; today it is the housing market and what remains of that same book. The instruments differ in resolution, and the coarser one flatters.

What this implies

For most of the period that matters here Poland barely had a macroprudential framework in the modern sense; the institutions and tools arrived largely after 2011, after the events that made Poland look resilient. The resilience came first, from the structure of the economy rather than from prudential policy applied to it.

That has an implication for the people who run these frameworks, and it is sharper than “monitor the growth model,” which is not an operational instruction. The lesson is about which tools sit where in the framework. Poland’s Swiss-franc book built up while aggregate credit stayed moderate, which means the credit-to-GDP gap — the cyclical indicator that anchors the countercyclical buffer — would never have flagged it: a concentrated currency mismatch is not a volume boom, and the gap is built to see volume booms. The borrower-based measures that catch this class of risk — caps on debt-service ratios, limits or bans on unhedged foreign-currency lending — are not cyclical switches a supervisor flips when a dashboard turns red. They are structural underwriting standards, and the Polish case is an argument for treating them that way: in place as a permanent baseline rather than held in reserve for a cyclical signal that, by construction, will not arrive in time for a risk that is not also a boom. Composition metrics earn their place a step below that: not as automatic triggers, but as the early evidence that justifies heightened scrutiny and informs how tightly the structural measures are calibrated. The currency denomination of household leverage, the share of external financing in reversible bank funding, the concentration of the real economy on single external channels: all were legible in Poland’s and Latvia’s data well before 2008, and all speak to risks the cyclical anchor cannot register. The contestable claim is not that supervisors should add three indicators to a dashboard; many already track them. It is that the framework should not depend on the cyclical gap to call for the structural tools, because for this class of risk the gap is the wrong instrument and will stay silent while the exposure builds.

The boundary on all of this is the FX book itself. Good composition on two of three counts did not stop Poland accumulating a Swiss-franc stock larger than Hungary’s; the growth model lit the incentive and supervision let it run; and neither composition nor surveillance resolved it, which is why the stock and the housing risk beside it are still on the ESRB’s list. Reading the terrain earlier is worth doing. It is not a substitute for holding the borrower-based instruments that catch what the terrain leaves exposed, nor for the supervisory willingness to use them — the count on which Hungary, with the worse model, outperformed.

Poland’s 2009 outcome was the right one, and the structure that produced it was partly legible in advance. The unresolved Swiss-franc book is the wrong one, on the same charts, fifteen years on. A resilient aggregate is worth having. It is not, on its own, the same thing as a safe one.

Paweł Fiedor — The Macro Prudential View

The views expressed are the author’s own and do not necessarily reflect those of any institution with which the author is or has been affiliated.

Sources: Eurostat, national accounts — GDP and main components, chain-linked volumes (nama_10_gdp) — https://ec.europa.eu/eurostat; Eurostat, balance of payments by country, current account and financial account (bop_c6_a), and GDP at market prices (nama_10_gdp), author calculations; BIS, Total Credit Statistics — credit to households and NPISHs, % of GDP, adjusted for breaks — https://www.bis.org/statistics/totcredit.htm; BIS, credit-to-GDP gaps (private non-financial sector) — https://www.bis.org/statistics/c_gaps.htm; Basel Committee on Banking Supervision, Guidance for national authorities operating the countercyclical capital buffer (December 2010) — https://www.bis.org/publ/bcbs187.htm; ECB, Statistical Data Warehouse — euro reference exchange rates (EXR) and MFI balance sheet items, loans to households in foreign currency (BSI) — https://data.ecb.europa.eu; Z. Zimny, Inward FDI-Related Challenges to Poland's Further Economic Progress (2015) — https://www.davidpublisher.com/Public/uploads/Contribute/56d3febf33bd9.pdf; Sveriges Riksbank, Financial crisis preparedness in the Nordic-Baltic region, Economic Commentary (2025) — https://www.riksbank.se; ECB Banking Supervision, Financial integration in the Baltics: lessons in resilience and transformation (4 October 2024) — https://www.bankingsupervision.europa.eu/press/speeches/date/2024/html/ssm.sp241004~9588c58d39.en.html; Peterson Institute for International Economics, Baltic Protests and Financial Meltdowns — https://www.piie.com/commentary/op-eds/baltic-protests-and-financial-meltdowns; European Systemic Risk Board, Follow-up report on vulnerabilities in the residential real estate sectors of the EEA countries (February 2024) — https://www.esrb.europa.eu/pub/pdf/reports/esrb.report.vulnerabilitiesresidentialrealestatesectors202402~df77b00f9a.en.pdf; European Systemic Risk Board, national macroprudential measures database — https://www.esrb.europa.eu/national_policy/; M. Piątkowski, Europe's Growth Champion: Insights from the Economic Rise of Poland (Oxford University Press, 2018). Chart data as cited in each figure.