Who Buys When the ECB Doesn't?

European sovereign debt markets are adjusting to life without the central bank. The buyers filling the gap are not equivalent substitutes.

On 5 March 2025, the German 10-year Bund yield rose by 30 basis points in a single trading session — the largest one-day move since the fall of the Berlin Wall. The immediate trigger was the coalition parties’ agreement to suspend the debt brake and establish a €500bn infrastructure and defence special fund. But the magnitude of the move revealed something more structural: a market in which the most reliable buyer has been systematically withdrawing for two years, and in which the new buyers are not equivalent replacements.

This article examines that structural shift through four data series. It is not, at its core, a story about German fiscal policy, although that is the most visible current catalyst. It is a story about who absorbs European sovereign debt when the ECB does not — and whether those buyers are stable enough to do so without periodic crises of the kind 5 March 2025 briefly resembled.

The timing is not accidental. The Group of Thirty released its working group report on nonbank financial intermediation in April 2026, co-chaired by Agustín Carstens and Klaas Knot, titled Nonbank Financial Intermediation and Financial Stability: A Perfect Storm in the Making? The report’s central concern — that NBFIs have taken on a growing share of sovereign financing precisely as their structural vulnerabilities are increasing — maps directly onto what European sovereign bond data now shows.

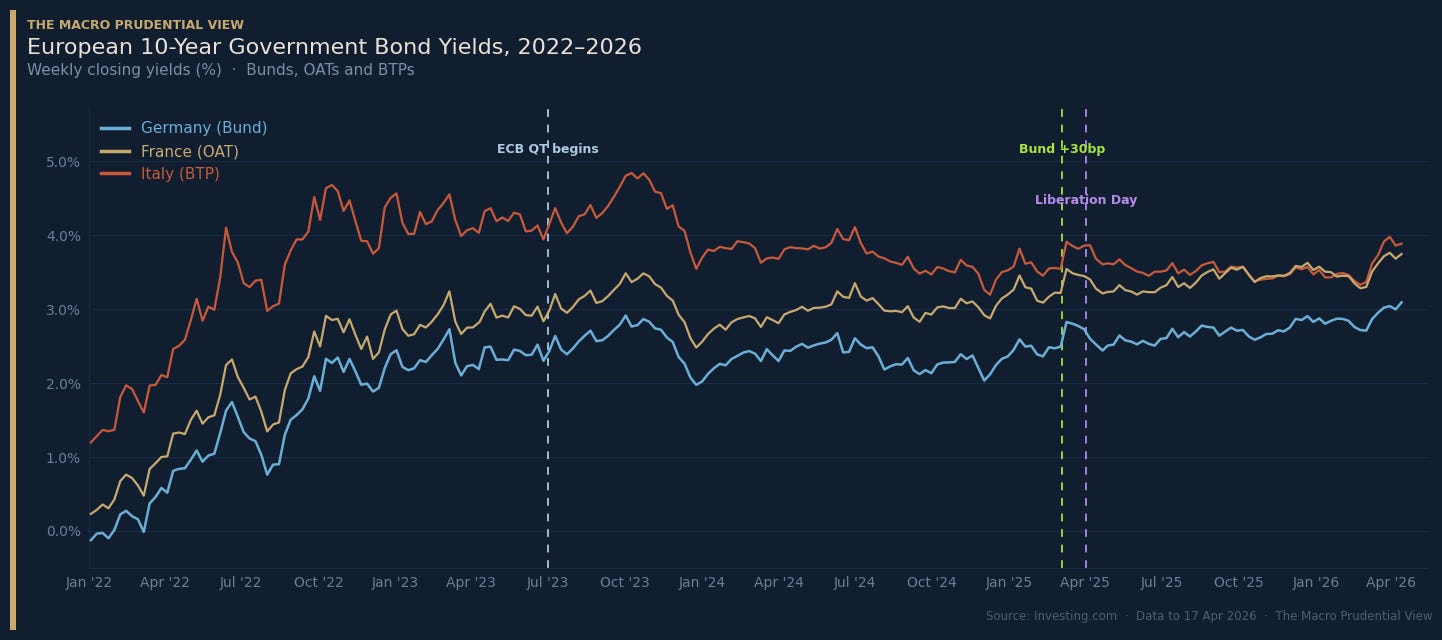

Yields and their volatility

The yield chart tells a familiar story at first glance: rates rose sharply from near-zero as the ECB tightened in 2022, then stabilised through 2023–2024, with the five major euro area sovereign curves trading in a broadly correlated band. Bund–BTP spreads, which peaked at around 250 basis points in mid-2022, compressed to roughly 115 basis points by early 2025 — itself a notable fact given ongoing pressure on Italian fiscal metrics.

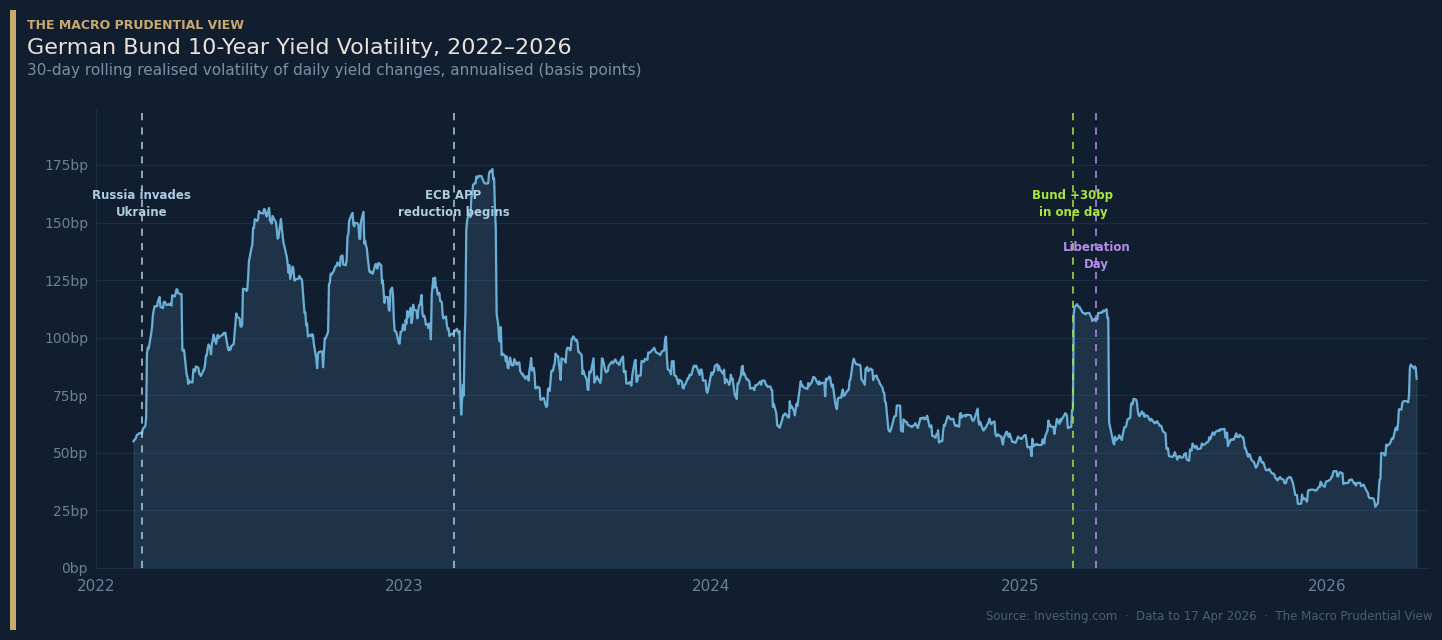

What is less visible in yield levels is volatility. The rolling realised volatility chart below makes it explicit.

The 2022 spike is expected — the ECB moved faster than at any point in its history, and markets were repricing duration risk across the entire curve simultaneously. What is more interesting is what happened in 2025. The March spike briefly exceeded the 2022 peak in short-term volatility terms, and it occurred in a regime that had looked, by the surface metrics of 2024, relatively calm.

The April episode — triggered by US tariff announcements that sparked a global risk-off rotation, initially driving capital toward core European sovereigns even as it unsettled peripheral spreads — produced a secondary spike. J.P Morgan & ESMA data (via ESRB report) showed that during the episode, European high-yield bond ETFs saw outflows of 6.4% of NAV in a single week, while sovereign bond funds saw simultaneous inflows — the flight-to-safety dynamic within the NBFI sector made visible, illustrating exactly the leveraged, fast-unwinding demand the G30 report warns about.

Two features of this overall pattern deserve attention. First, the 2025 spikes are idiosyncratic rather than systemic in origin — one driven by domestic fiscal news, one by US trade policy — suggesting the market has become sensitive to individual triggers in a way it was not when the ECB was a reliable marginal buyer.

Second, neither episode produced lasting dislocation. The ECB did not intervene. Markets self-corrected. This is the outcome policymakers point to as evidence that the absorption transition is proceeding smoothly. It may be the right conclusion — or it may reflect conditions that have not yet been genuinely tested.

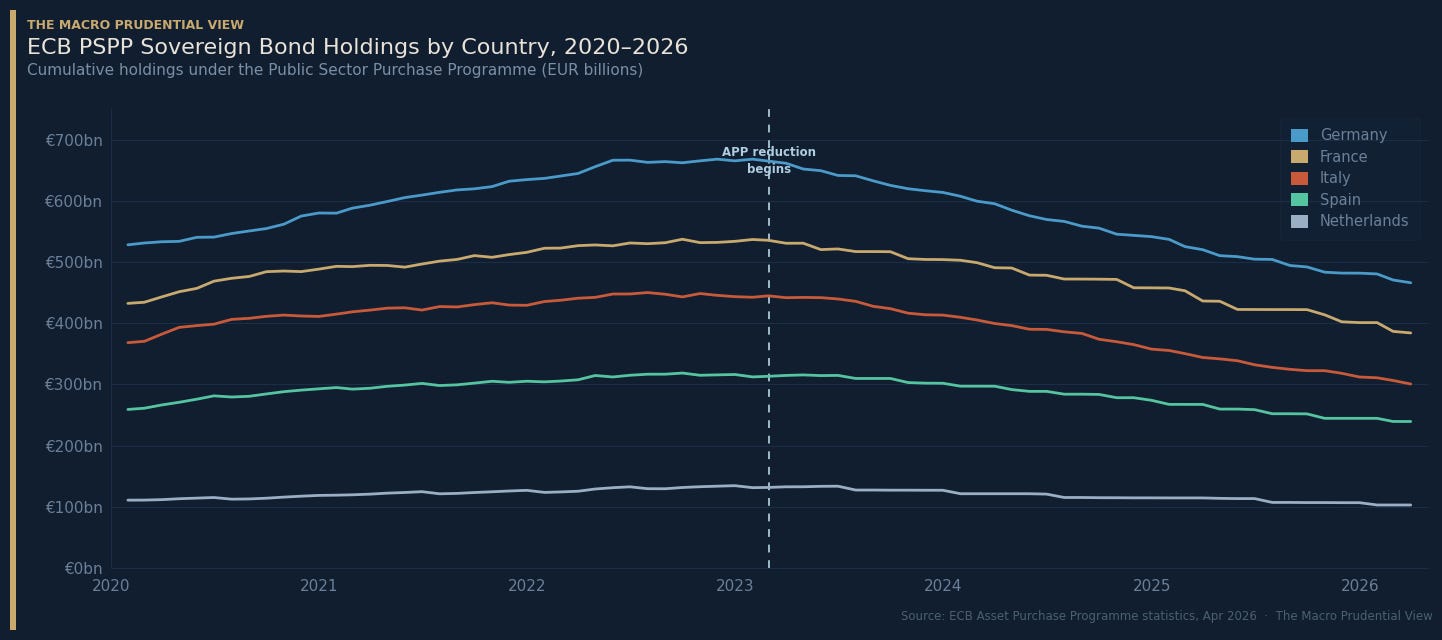

The supply gap

The ECB’s withdrawal from European sovereign bond markets is neither subtle nor ambiguous in the data. Under the PSPP, the ECB built cumulative holdings of roughly €670bn in German sovereign debt, €540bn in French, €450bn in Italian and €320bn in Spanish bonds at their respective peaks. Since active portfolio reduction began in March 2023, those holdings have fallen by €202bn, €153bn, €149bn and €79bn respectively — a combined withdrawal of roughly €600bn across the five largest euro area economies in under three years.

The pace matters as much as the magnitude. The ECB is no longer reinvesting the principal payments from maturing securities under the PSPP; it is allowing its portfolio to run off at a measured and predictable pace — a portfolio that became, during the QE years, one of the largest single holders of European sovereign debt. The buyers on the other side of this withdrawal are heterogeneous — domestic banks, foreign official sector, asset managers, pension funds, insurance corporations, and an increasingly significant segment of hedge funds operating through the repo market. The ESRB’s NBFI Risk Monitor documents hedge funds’ average net borrowing in EU sovereign repo at €115bn in Q4 2024. That is not a trivial position. The pattern is not unique to the euro area. The Bank of England's Deputy Governor for Financial Stability noted on 17 April 2026 that net gilt repo positioning among hedge funds reached its highest level since data collection began in 2017 by early 2026, with borrowing concentrated among a relatively small number of firms pursuing similar strategies — a concentration risk that maps directly onto the European data.

What is striking about this transition is its coincidence with rising supply. Germany’s debt brake suspension and the €500bn special fund represent a structural shift in sovereign issuance that will persist for the better part of a decade. France, Italy and Spain face their own fiscal pressures. The G30 report notes that sovereign debt in advanced economies has expanded roughly 60% faster than credit to the private sector over the past fifteen years, and that NBFIs must increasingly serve as the marginal buyer as central banks withdraw. The European data confirms this is happening not as a projection but as a present reality.

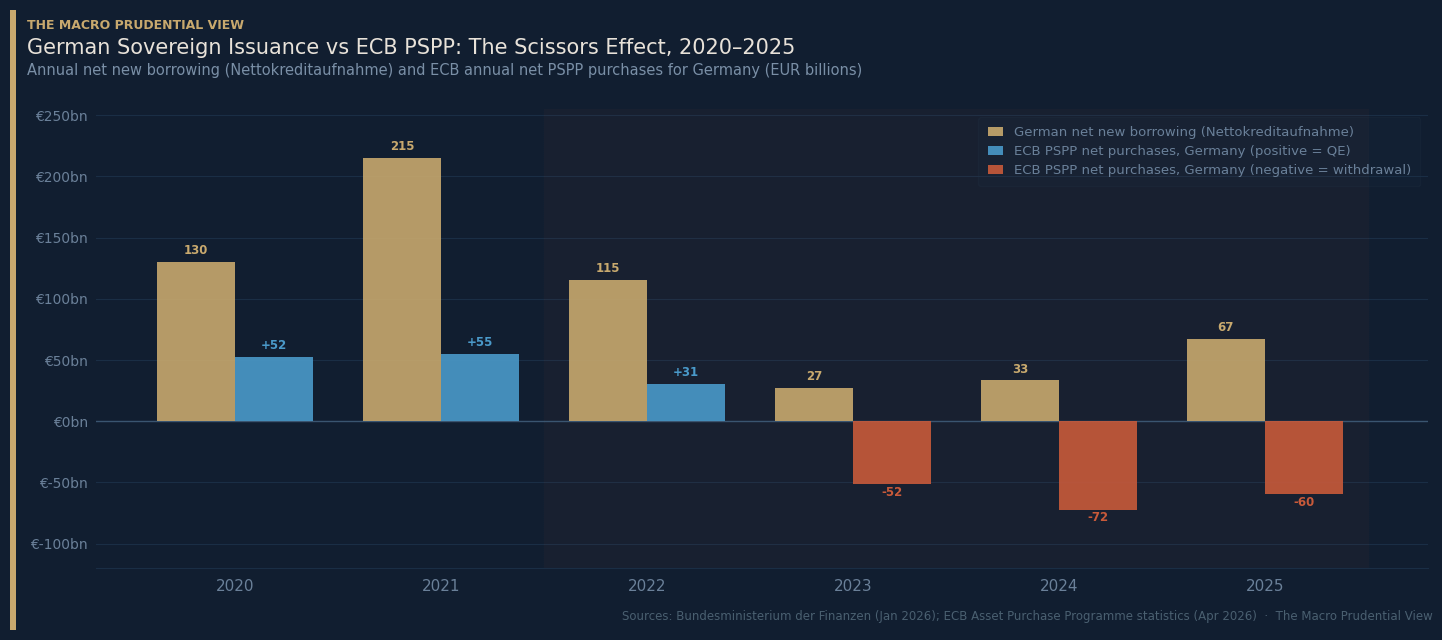

The scissors effect

The fourth chart makes the supply-demand shift most concrete. In 2020 and 2021, the ECB absorbed roughly €52–55bn annually in German sovereign debt — covering between 25% and 40% of Germany’s net new borrowing in those years. The pandemic fiscal response was, in this sense, substantially ECB-financed. From 2023, the relationship inverted. The ECB withdrew €51.7bn net in 2023, a year in which Germany itself only net-borrowed €27.2bn. In 2024, ECB withdrawal (€72.2bn) was more than twice Germany’s net issuance (€33.3bn).

This is the scissors effect: simultaneously rising supply and withdrawing central bank support, meeting at a point where the residual buyer must absorb both the new issuance and the ongoing redemptions from the ECB’s portfolio. With German net borrowing rising again in 2025 (€67bn) and the special fund adding further issuance pressure from 2026, the structural demand for non-ECB buyers of German paper is growing in both directions at once.

The BlackRock Investment Institute, writing on 13 April 2026, concluded that increased German bond issuance “is already largely reflected in the current level of 10-year yields.” That may well be correct. But markets have a habit of interpreting the absence of stress as proof of resilience — precisely the behavioural bias the G30 report cautions against.

Who the new buyers are, and why it matters

The G30 report’s taxonomy of NBFI forms is useful here. The buyers filling the ECB’s role in European sovereign markets are not homogenous. Some — pension funds, insurance corporations, sovereign wealth funds — are genuinely long-horizon, buy-and-hold investors whose presence in the sovereign market is structurally stabilising. The FSB’s latest global monitoring report confirms that these investors have increased their sovereign debt holdings meaningfully, though gradually.

Others are not. The ESRB’s data on hedge fund sovereign repo exposure, and the G30’s documentation of near-zero repo haircuts for the largest hedge-fund borrowers — in some cases 50 basis points or lower — implying leverage ratios that can reach 200 times or more — point to a significant component of sovereign market demand that is highly leveraged, short-duration funded, and prone to rapid unwinding. The basis trade, in which hedge funds hold sovereign bonds financed through repo while taking offsetting derivatives positions, has become a meaningful source of demand in European sovereign markets. The April 2025 episode illustrated what the European equivalent could look like at larger scale under less benign conditions.

Critically, this is not a risk contained within the NBFI sector. The G30 report’s “transformation form” argument makes clear that while credit risk has migrated from banks to NBFIs, much of the associated liquidity risk remains concentrated in the banking system. When a leveraged basis trade unwinds, the prime brokerage banks are directly in the line of fire — which is why the G30 treats this not as a shadow banking problem but as a core financial system problem.

The FSB documents that NBFIs increased their share of advanced economy sovereign bond holdings by approximately 7.9 percentage points between 2021 and 2024. What this means in practice is that the marginal price-setter in European sovereign markets has changed — from a central bank with an unlimited balance sheet, no leverage constraint, and no redemption risk, to a collection of entities with varying degrees of leverage, short-term funding, and sensitivity to global risk appetite.

This does not make European sovereign markets unstable. Most of the time, the new buyer composition functions adequately. The 2025 episodes suggest that under episodic stress, the transition from central bank to NBFI as marginal buyer is visible in volatility even when it does not produce lasting dislocation.

The honest uncertainty is whether episodes that resolve without intervention are evidence of resilience, or of good fortune.

The regulatory gap

One dimension of this transition that the G30 report addresses directly, and that the European data makes urgent, is the absence of a central bank liquidity facility for NBFIs in the euro area. The Bank of England adopted its Contingent Non-Bank Financial Institution Repo Facility in 2025 — a pre-designed, contingent mechanism through which the BoE can provide repo liquidity directly to insurance corporations and pension funds under defined stress conditions, at penalty rates and with strict eligibility criteria. The facility is not standing; it activates on defined triggers. But its existence means the BoE has a documented, ex-ante response to NBFI liquidity stress in gilt markets.

The ECB has no equivalent. EUREP — the ECB’s repo facility for non-euro area central banks — is not designed for this purpose. The ECB’s operational toolkit for managing sovereign market dysfunction runs through bank intermediation and, ultimately, asset purchase programmes.

The G30 report is explicit: relying on broad asset-purchase programmes as the default backstop for NBFI stress creates moral hazard and blurs monetary-policy communication. No equivalent targeted, pre-committed tool currently exists in the euro area. This is not an argument for the ECB to backstop hedge funds. The G30’s framework carefully distinguishes between providing contingent liquidity to systemically important NBFI activities — pension funds, insurance corporations, large asset managers — under strict conditions, and open-ended support for leveraged trading strategies. The former has a legitimate financial stability rationale. The latter does not. The challenge is that designing a facility which credibly separates the two, in advance, is genuinely difficult — as the BoE’s CNRF design process illustrated. The difficulty of the design problem is, in the G30’s assessment, not a sufficient reason to avoid attempting it.

What to watch

The immediate catalyst for this article — the March 2025 Bund spike and its connection to German fiscal expansion — will fade as a market focus. German issuance will be absorbed, spreads will stabilise, and the volatility charts will normalise. That is almost certainly the right base case.

What will not normalise is the structural composition of who holds European sovereign debt. The ECB’s portfolio will continue to decline. German, French and Italian issuance will continue to rise. The NBFI share of the marginal buyer will grow further. And the institutional infrastructure for managing stress in that buyer base — data quality, supervisory frameworks, liquidity facilities, crisis simulation — remains incomplete by the most detailed practitioner assessment yet published on the subject.

The G30 report asks whether a perfect storm is in the making. The honest answer, consistent with the report itself, is that the conditions for one are assembling — and that the absence of a storm so far is not the same as the absence of risk.

Paweł Fiedor — The Macro Prudential View

Charts compiled from ECB Asset Purchase Programme statistics (April 2026), Bundesministerium der Finanzen (January 2026), ESRB NBFI Risk Monitor, and Investing.com. Full G30 report: Nonbank Financial Intermediation and Financial Stability: A Perfect Storm in the Making? BlackRock Investment Institute commentary (13 April 2026) linked in text.

The absence of a storm so far is doing a lot of work as proof of resilience, this is the most important sentence in the piece.

Really enjoyed this. The most interesting part for me is the way you shift the focus toward the question of who actually absorbs sovereign debt now that the ECB is stepping back.

I also liked the ending point. Just because recent episodes resolved without intervention does not necessarily prove resilience, as it might simply mean the system has not been tested under worse conditions yet. Very nice article.